Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

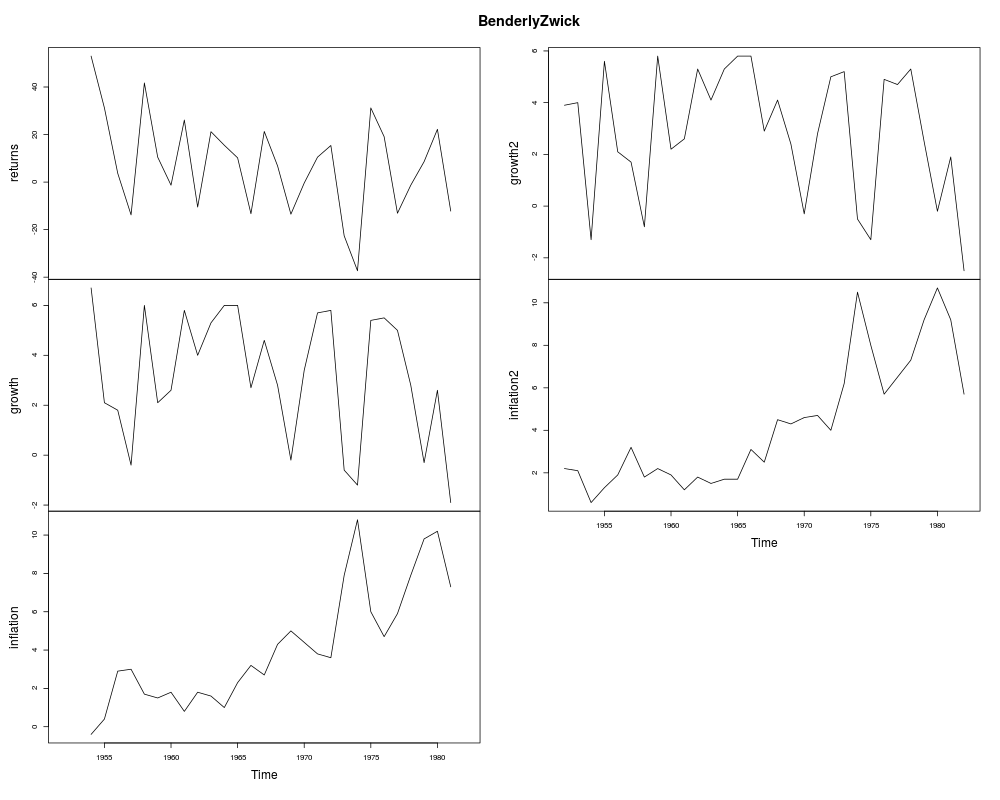

Benderly and Zwick Data: Inflation, Growth and Stock ReturnsDescriptionTime series data, 1952–1982. Usagedata("BenderlyZwick")

FormatAn annual multiple time series from 1952 to 1982 with 5 variables.

SourceThe first three columns of the data are from Table 1 in Benderly and Zwick (1985). The remaining columns are taken from the online complements of Baltagi (2002). The first column is identical in both sources, the other two variables differ in their numeric values and additionally the growth series seems to be lagged differently. Baltagi (2002) states Lott and Ray (1992) as the source for his version of the data set. ReferencesBaltagi, B.H. (2002). Econometrics, 3rd ed. Berlin, Springer. Benderly, J., and Zwick, B. (1985). Inflation, Real Balances, Output and Real Stock Returns. American Economic Review, 75, 1115–1123. Lott, W.F., and Ray, S.C. (1992). Applied Econometrics: Problems with Data Sets. New York: The Dryden Press. Zaman, A., Rousseeuw, P.J., and Orhan, M. (2001). Econometric Applications of High-Breakdown Robust Regression Techniques. Economics Letters, 71, 1–8. See Also

Examples

data("BenderlyZwick")

plot(BenderlyZwick)

## Benderly and Zwick (1985), p. 1116

library("dynlm")

bz_ols <- dynlm(returns ~ growth + inflation,

data = BenderlyZwick/100, start = 1956, end = 1981)

summary(bz_ols)

## Zaman, Rousseeuw and Orhan (2001)

## use larger period, without scaling

bz_ols2 <- dynlm(returns ~ growth + inflation,

data = BenderlyZwick, start = 1954, end = 1981)

summary(bz_ols2)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(AER)

Loading required package: car

Loading required package: lmtest

Loading required package: zoo

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numeric

Loading required package: sandwich

Loading required package: survival

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/AER/BenderlyZwick.Rd_%03d_medium.png", width=480, height=480)

> ### Name: BenderlyZwick

> ### Title: Benderly and Zwick Data: Inflation, Growth and Stock Returns

> ### Aliases: BenderlyZwick

> ### Keywords: datasets

>

> ### ** Examples

>

> data("BenderlyZwick")

> plot(BenderlyZwick)

>

> ## Benderly and Zwick (1985), p. 1116

> library("dynlm")

> bz_ols <- dynlm(returns ~ growth + inflation,

+ data = BenderlyZwick/100, start = 1956, end = 1981)

> summary(bz_ols)

Time series regression with "ts" data:

Start = 1956, End = 1981

Call:

dynlm(formula = returns ~ growth + inflation, data = BenderlyZwick/100,

start = 1956, end = 1981)

Residuals:

Min 1Q Median 3Q Max

-0.279553 -0.073666 -0.004526 0.085589 0.224095

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.1238 0.0833 -1.486 0.150747

growth 5.2255 1.2702 4.114 0.000424 ***

inflation 0.1882 1.1053 0.170 0.866312

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1333 on 23 degrees of freedom

Multiple R-squared: 0.5119, Adjusted R-squared: 0.4695

F-statistic: 12.06 on 2 and 23 DF, p-value: 0.0002617

>

> ## Zaman, Rousseeuw and Orhan (2001)

> ## use larger period, without scaling

> bz_ols2 <- dynlm(returns ~ growth + inflation,

+ data = BenderlyZwick, start = 1954, end = 1981)

> summary(bz_ols2)

Time series regression with "ts" data:

Start = 1954, End = 1981

Call:

dynlm(formula = returns ~ growth + inflation, data = BenderlyZwick,

start = 1954, end = 1981)

Residuals:

Min 1Q Median 3Q Max

-27.235 -8.478 -0.848 6.322 25.171

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -3.586 8.581 -0.418 0.6796

growth 4.778 1.368 3.492 0.0018 **

inflation -1.046 1.145 -0.913 0.3698

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 15.02 on 25 degrees of freedom

Multiple R-squared: 0.4961, Adjusted R-squared: 0.4558

F-statistic: 12.31 on 2 and 25 DF, p-value: 0.0001902

>

>

>

>

>

> dev.off()

null device

1

>

|