Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Data and Examples from Greene (2003)DescriptionThis manual page collects a list of examples from the book. Some solutions might not be exact and the list is certainly not complete. If you have suggestions for improvement (preferably in the form of code), please contact the package maintainer. ReferencesGreene, W.H. (2003). Econometric Analysis, 5th edition. Upper Saddle River, NJ: Prentice Hall. URL http://pages.stern.nyu.edu/~wgreene/Text/tables/tablelist5.htm. See Also

Examples

#####################################

## US consumption data (1970-1979) ##

#####################################

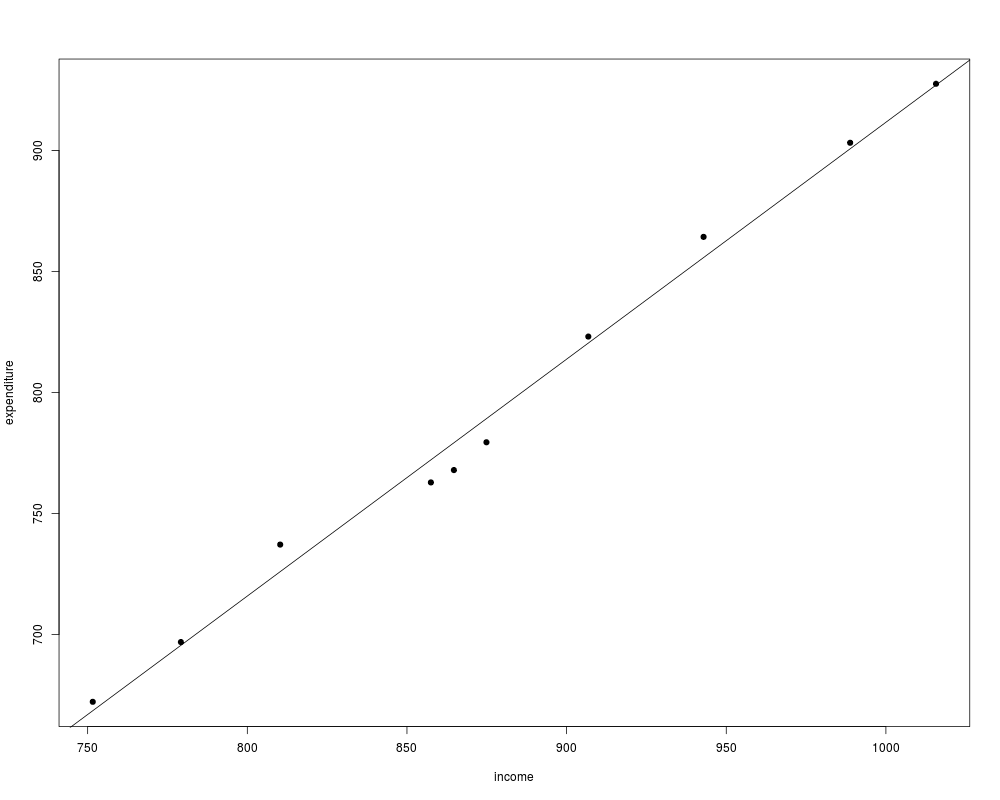

## Example 1.1

data("USConsump1979", package = "AER")

plot(expenditure ~ income, data = as.data.frame(USConsump1979), pch = 19)

fm <- lm(expenditure ~ income, data = as.data.frame(USConsump1979))

summary(fm)

abline(fm)

#####################################

## US consumption data (1940-1950) ##

#####################################

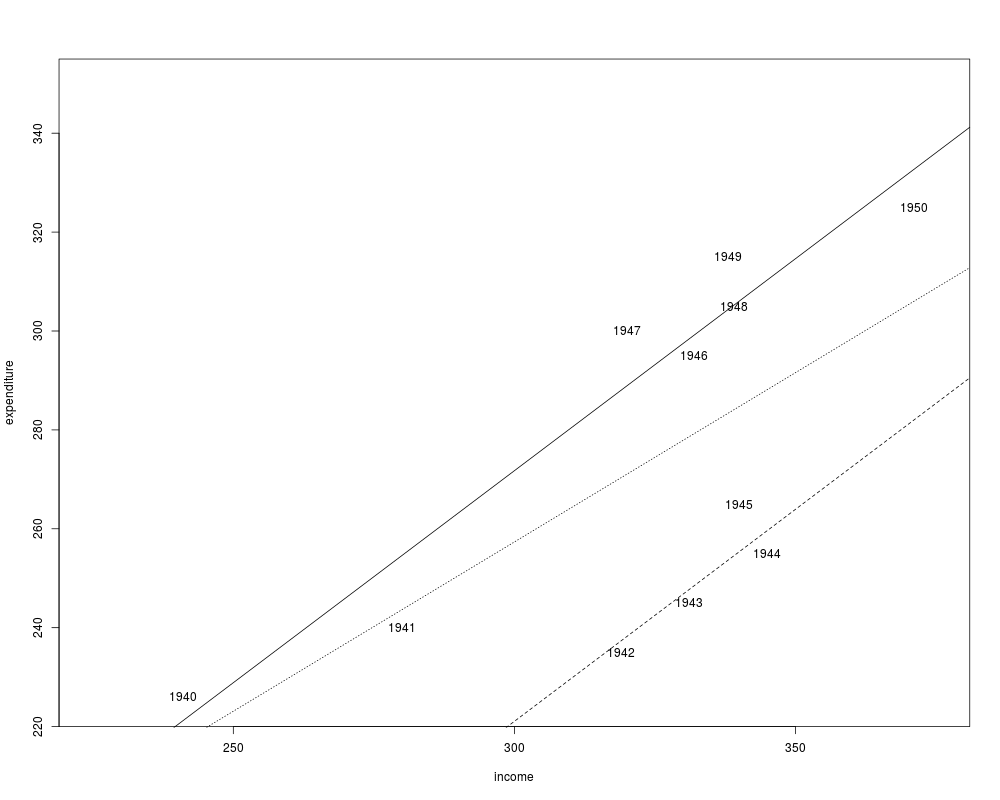

## data

data("USConsump1950", package = "AER")

usc <- as.data.frame(USConsump1950)

usc$war <- factor(usc$war, labels = c("no", "yes"))

## Example 2.1

plot(expenditure ~ income, data = usc, type = "n", xlim = c(225, 375), ylim = c(225, 350))

with(usc, text(income, expenditure, time(USConsump1950)))

## single model

fm <- lm(expenditure ~ income, data = usc)

summary(fm)

## different intercepts for war yes/no

fm2 <- lm(expenditure ~ income + war, data = usc)

summary(fm2)

## compare

anova(fm, fm2)

## visualize

abline(fm, lty = 3)

abline(coef(fm2)[1:2])

abline(sum(coef(fm2)[c(1, 3)]), coef(fm2)[2], lty = 2)

## Example 3.2

summary(fm)$r.squared

summary(lm(expenditure ~ income, data = usc, subset = war == "no"))$r.squared

summary(fm2)$r.squared

########################

## US investment data ##

########################

data("USInvest", package = "AER")

## Chapter 3 in Greene (2003)

## transform (and round) data to match Table 3.1

us <- as.data.frame(USInvest)

us$invest <- round(0.1 * us$invest/us$price, digits = 3)

us$gnp <- round(0.1 * us$gnp/us$price, digits = 3)

us$inflation <- c(4.4, round(100 * diff(us$price)/us$price[-15], digits = 2))

us$trend <- 1:15

us <- us[, c(2, 6, 1, 4, 5)]

## p. 22-24

coef(lm(invest ~ trend + gnp, data = us))

coef(lm(invest ~ gnp, data = us))

## Example 3.1, Table 3.2

cor(us)[1,-1]

pcor <- solve(cor(us))

dcor <- 1/sqrt(diag(pcor))

pcor <- (-pcor * (dcor %o% dcor))[1,-1]

## Table 3.4

fm <- lm(invest ~ trend + gnp + interest + inflation, data = us)

fm1 <- lm(invest ~ 1, data = us)

anova(fm1, fm)

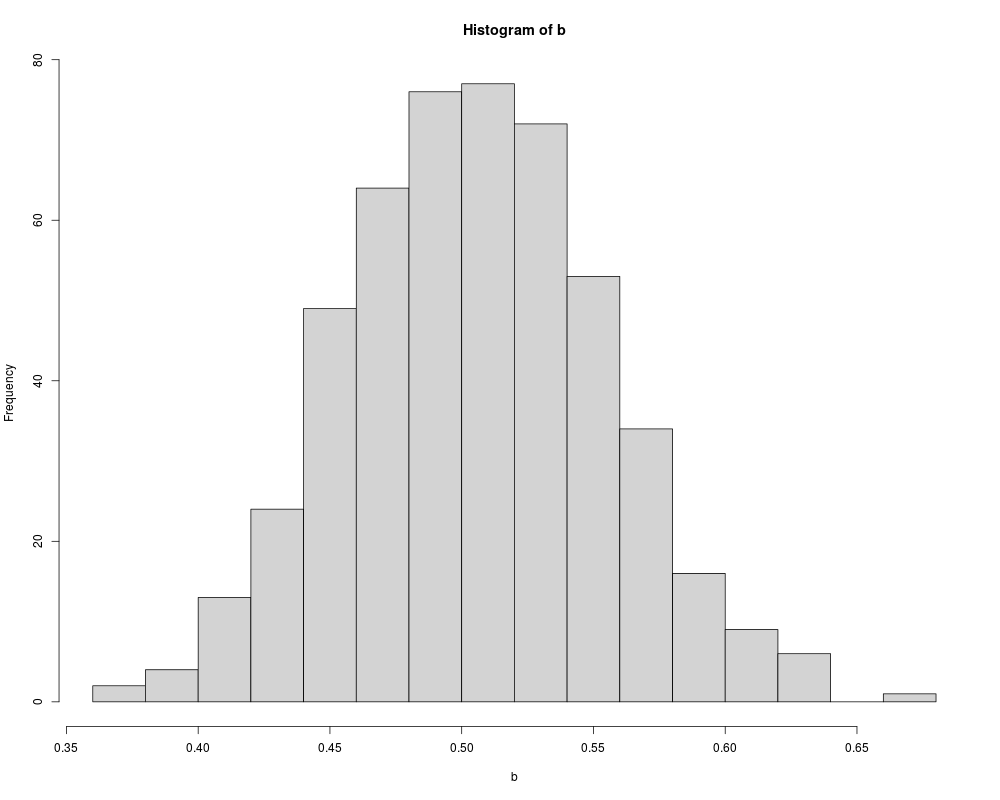

## Example 4.1

set.seed(123)

w <- rnorm(10000)

x <- rnorm(10000)

eps <- 0.5 * w

y <- 0.5 + 0.5 * x + eps

b <- rep(0, 500)

for(i in 1:500) {

ix <- sample(1:10000, 100)

b[i] <- lm.fit(cbind(1, x[ix]), y[ix])$coef[2]

}

hist(b, breaks = 20, col = "lightgray")

###############################

## Longley's regression data ##

###############################

## package and data

data("Longley", package = "AER")

library("dynlm")

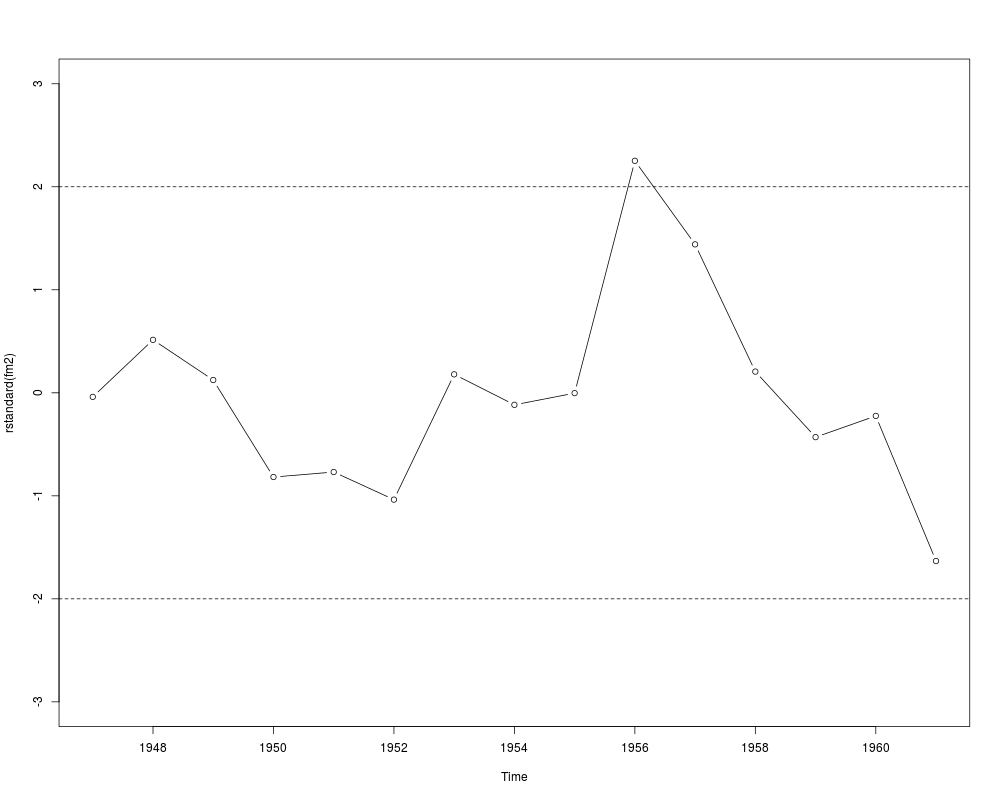

## Example 4.6

fm1 <- dynlm(employment ~ time(employment) + price + gnp + armedforces,

data = Longley)

fm2 <- update(fm1, end = 1961)

cbind(coef(fm2), coef(fm1))

## Figure 4.3

plot(rstandard(fm2), type = "b", ylim = c(-3, 3))

abline(h = c(-2, 2), lty = 2)

#########################################

## US gasoline market data (1960-1995) ##

#########################################

## data

data("USGasG", package = "AER")

## Greene (2003)

## Example 2.3

fm <- lm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

data = as.data.frame(USGasG))

summary(fm)

## Example 4.4

## estimates and standard errors (note different offset for intercept)

coef(fm)

sqrt(diag(vcov(fm)))

## confidence interval

confint(fm, parm = "log(income)")

## test linear hypothesis

linearHypothesis(fm, "log(income) = 1")

## Figure 7.5

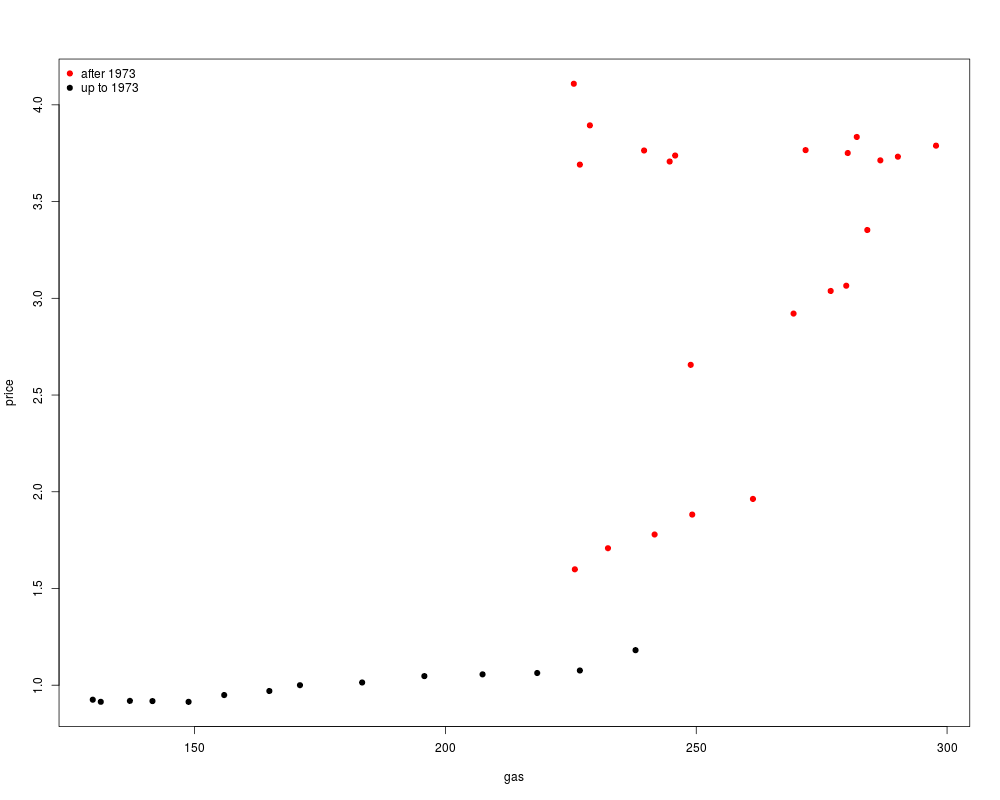

plot(price ~ gas, data = as.data.frame(USGasG), pch = 19,

col = (time(USGasG) > 1973) + 1)

legend("topleft", legend = c("after 1973", "up to 1973"), pch = 19, col = 2:1, bty = "n")

## Example 7.6

## re-used in Example 8.3

## linear time trend

ltrend <- 1:nrow(USGasG)

## shock factor

shock <- factor(time(USGasG) > 1973, levels = c(FALSE, TRUE), labels = c("before", "after"))

## 1960-1995

fm1 <- lm(log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

data = as.data.frame(USGasG))

summary(fm1)

## pooled

fm2 <- lm(

log(gas/population) ~ shock + log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

data = as.data.frame(USGasG))

summary(fm2)

## segmented

fm3 <- lm(

log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) + log(usedcar) + ltrend),

data = as.data.frame(USGasG))

summary(fm3)

## Chow test

anova(fm3, fm1)

library("strucchange")

sctest(log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

data = USGasG, point = c(1973, 1), type = "Chow")

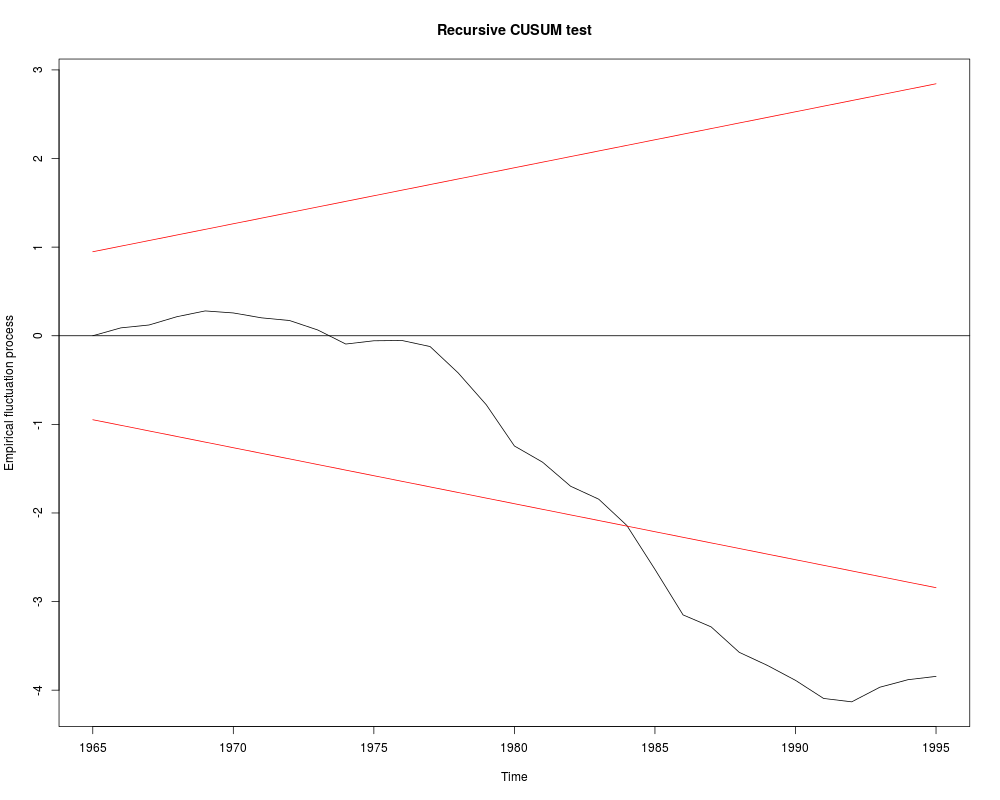

## Recursive CUSUM test

rcus <- efp(log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

data = USGasG, type = "Rec-CUSUM")

plot(rcus)

sctest(rcus)

## Note: Greene's remark that the break is in 1984 (where the process crosses its boundary)

## is wrong. The break appears to be no later than 1976.

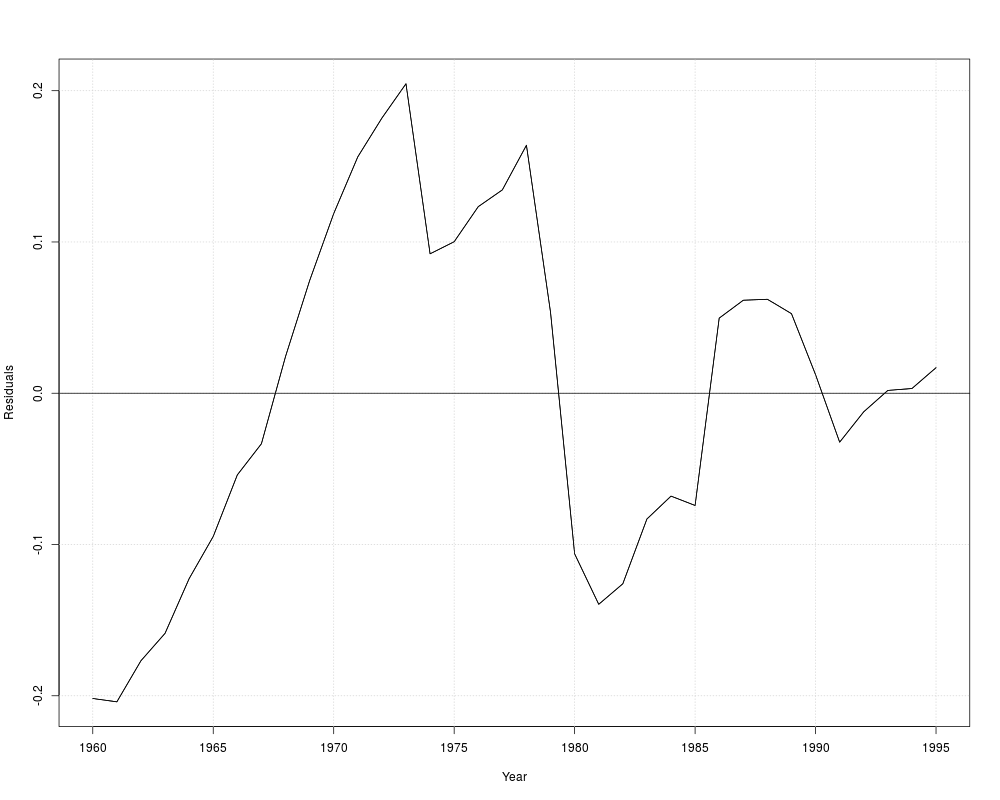

## Example 12.2

library("dynlm")

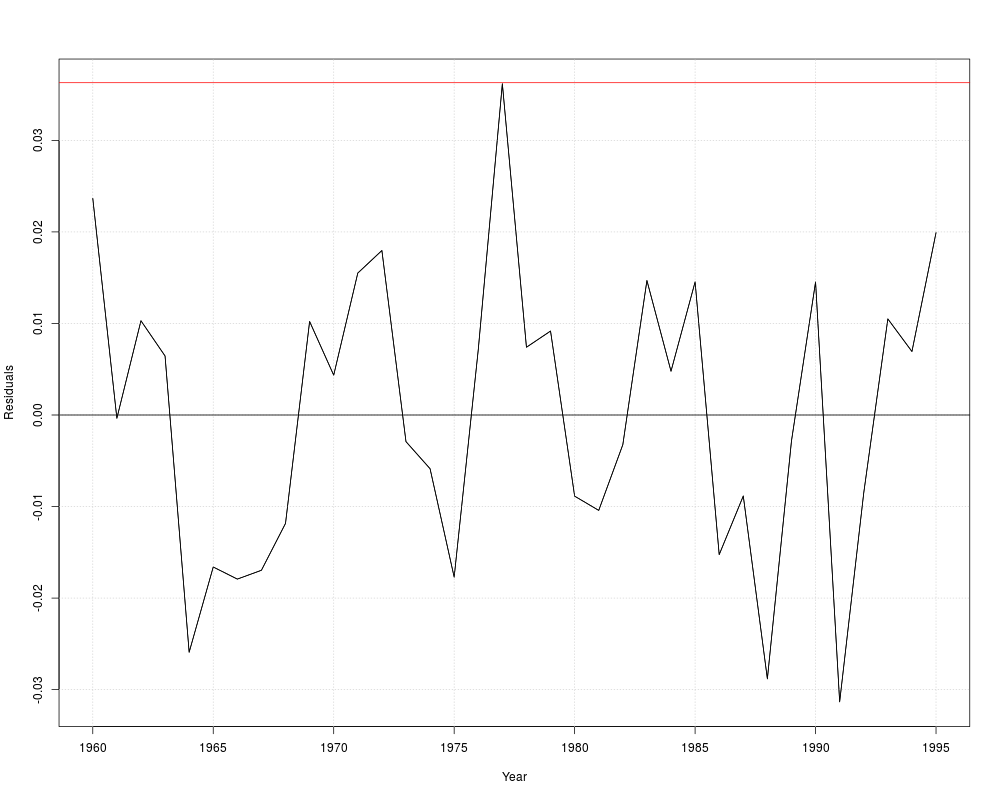

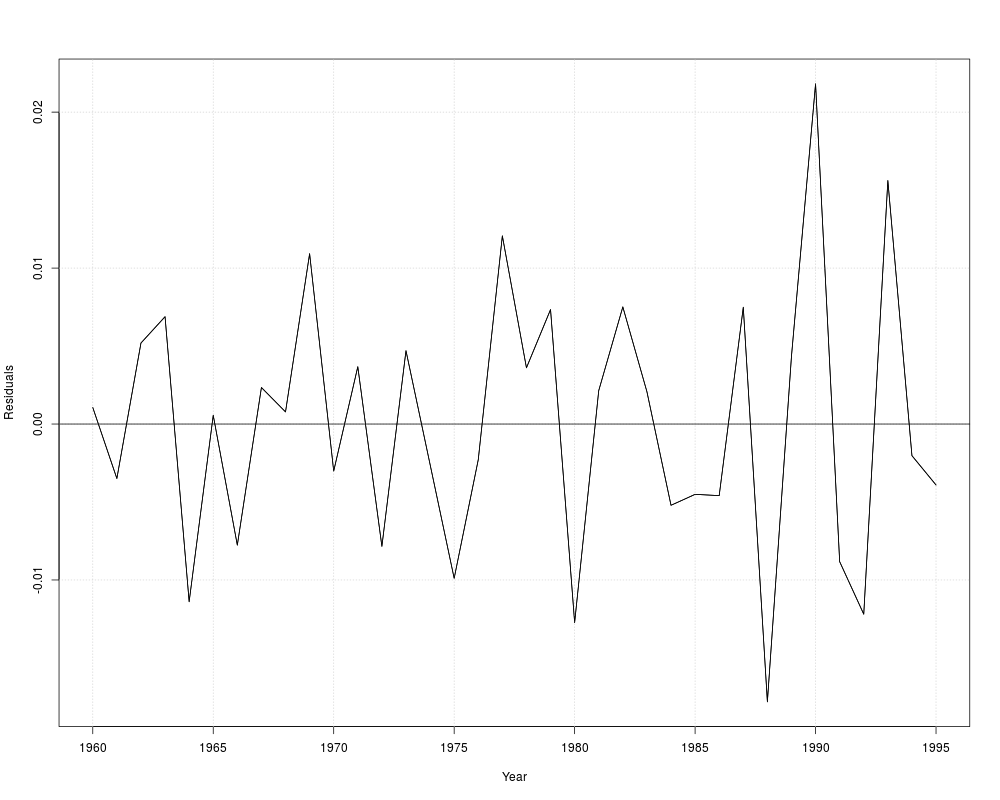

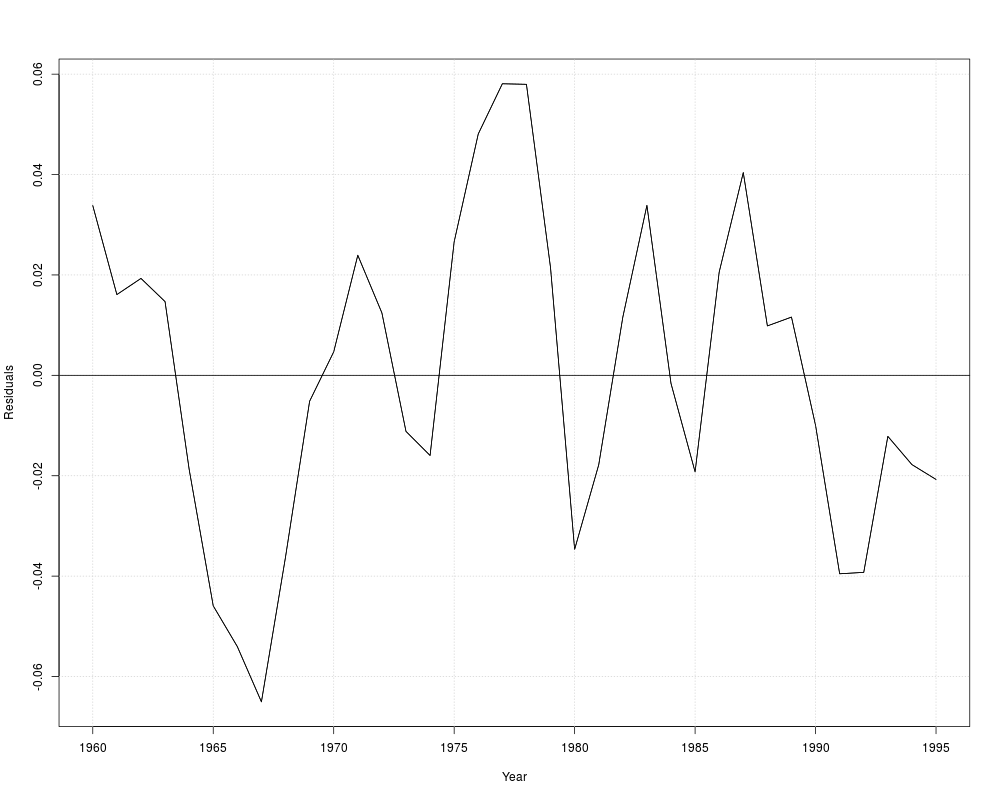

resplot <- function(obj, bound = TRUE) {

res <- residuals(obj)

sigma <- summary(obj)$sigma

plot(res, ylab = "Residuals", xlab = "Year")

grid()

abline(h = 0)

if(bound) abline(h = c(-2, 2) * sigma, col = "red")

lines(res)

}

resplot(dynlm(log(gas/population) ~ log(price), data = USGasG))

resplot(dynlm(log(gas/population) ~ log(price) + log(income), data = USGasG))

resplot(dynlm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar) +

log(transport) + log(nondurable) + log(durable) +log(service) + ltrend, data = USGasG))

## different shock variable than in 7.6

shock <- factor(time(USGasG) > 1974, levels = c(FALSE, TRUE), labels = c("before", "after"))

resplot(dynlm(log(gas/population) ~ shock/(log(price) + log(income) + log(newcar) + log(usedcar) +

log(transport) + log(nondurable) + log(durable) + log(service) + ltrend), data = USGasG))

## NOTE: something seems to be wrong with the sigma estimates in the `full' models

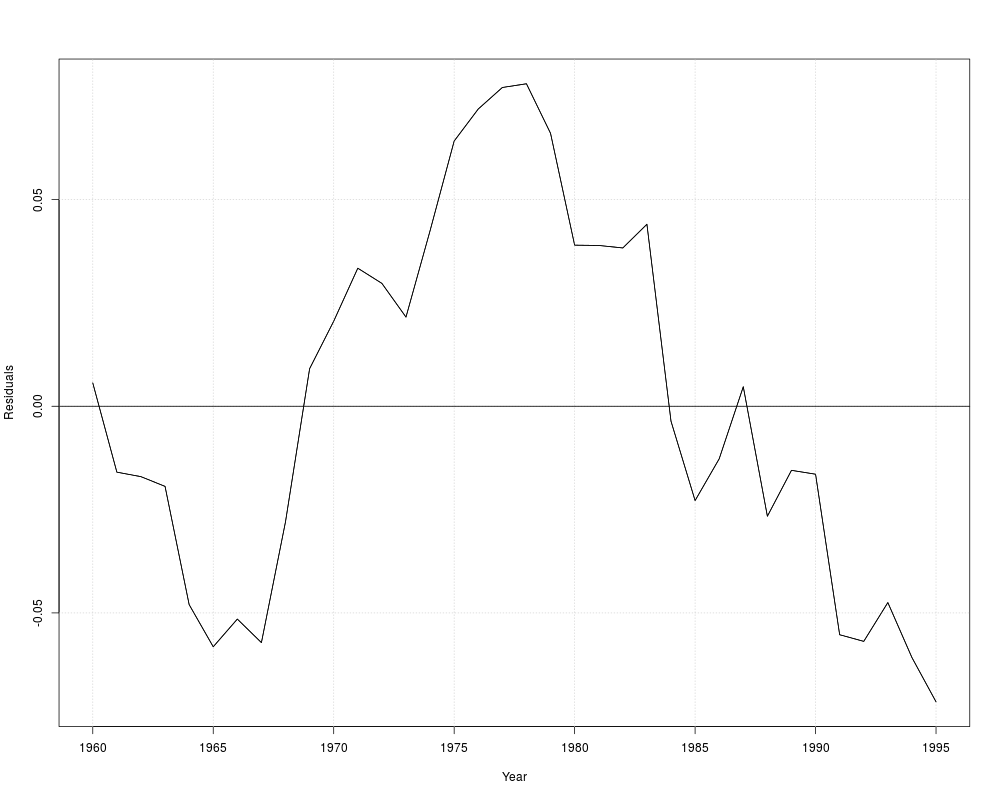

## Table 12.4, OLS

fm <- dynlm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

data = USGasG)

summary(fm)

resplot(fm, bound = FALSE)

dwtest(fm)

## ML

g <- as.data.frame(USGasG)

y <- log(g$gas/g$population)

X <- as.matrix(cbind(log(g$price), log(g$income), log(g$newcar), log(g$usedcar)))

arima(y, order = c(1, 0, 0), xreg = X)

#######################################

## US macroeconomic data (1950-2000) ##

#######################################

## data and trend

data("USMacroG", package = "AER")

ltrend <- 0:(nrow(USMacroG) - 1)

## Example 5.3

## OLS and IV regression

library("dynlm")

fm_ols <- dynlm(consumption ~ gdp, data = USMacroG)

fm_iv <- dynlm(consumption ~ gdp | L(consumption) + L(gdp), data = USMacroG)

## Hausman statistic

library("MASS")

b_diff <- coef(fm_iv) - coef(fm_ols)

v_diff <- summary(fm_iv)$cov.unscaled - summary(fm_ols)$cov.unscaled

(t(b_diff) %*% ginv(v_diff) %*% b_diff) / summary(fm_ols)$sigma^2

## Wu statistic

auxreg <- dynlm(gdp ~ L(consumption) + L(gdp), data = USMacroG)

coeftest(dynlm(consumption ~ gdp + fitted(auxreg), data = USMacroG))[3,3]

## agrees with Greene (but not with errata)

## Example 6.1

## Table 6.1

fm6.1 <- dynlm(log(invest) ~ tbill + inflation + log(gdp) + ltrend, data = USMacroG)

fm6.3 <- dynlm(log(invest) ~ I(tbill - inflation) + log(gdp) + ltrend, data = USMacroG)

summary(fm6.1)

summary(fm6.3)

deviance(fm6.1)

deviance(fm6.3)

vcov(fm6.1)[2,3]

## F test

linearHypothesis(fm6.1, "tbill + inflation = 0")

## alternatively

anova(fm6.1, fm6.3)

## t statistic

sqrt(anova(fm6.1, fm6.3)[2,5])

## Example 6.3

## Distributed lag model:

## log(Ct) = b0 + b1 * log(Yt) + b2 * log(C(t-1)) + u

us <- log(USMacroG[, c(2, 5)])

fm_distlag <- dynlm(log(consumption) ~ log(dpi) + L(log(consumption)),

data = USMacroG)

summary(fm_distlag)

## estimate and test long-run MPC

coef(fm_distlag)[2]/(1-coef(fm_distlag)[3])

linearHypothesis(fm_distlag, "log(dpi) + L(log(consumption)) = 1")

## correct, see errata

## Example 6.4

## predict investiment in 2001(1)

predict(fm6.1, interval = "prediction",

newdata = data.frame(tbill = 4.48, inflation = 5.262, gdp = 9316.8, ltrend = 204))

## Example 7.7

## no GMM available in "strucchange"

## using OLS instead yields

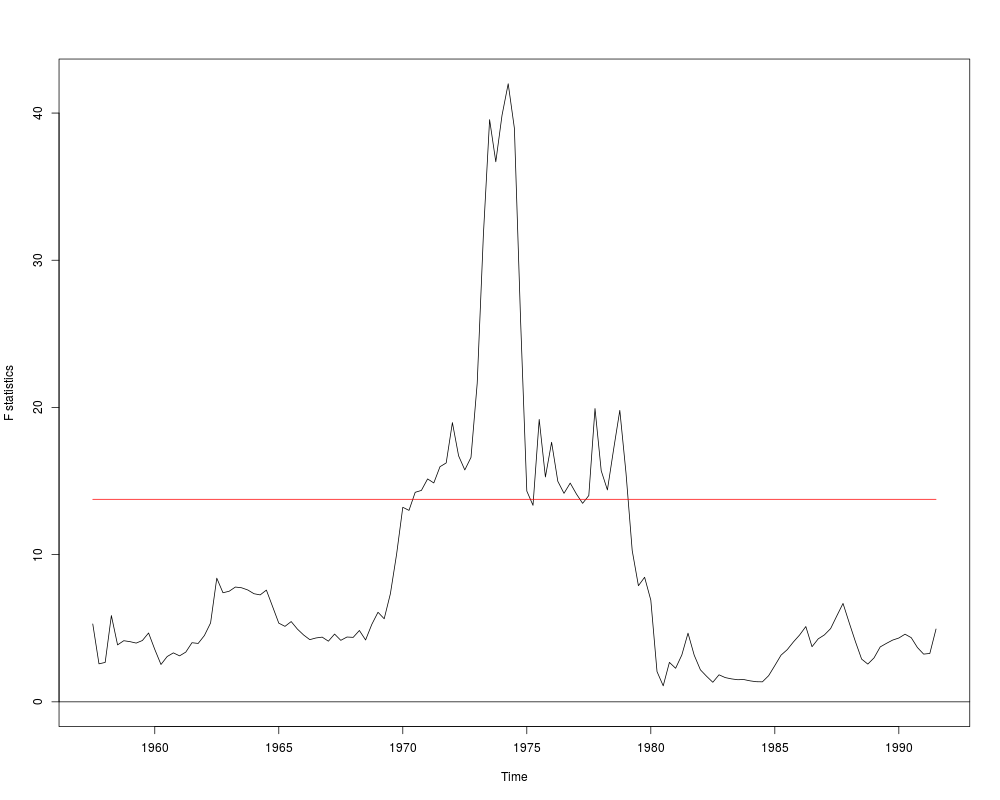

fs <- Fstats(log(m1/cpi) ~ log(gdp) + tbill, data = USMacroG,

vcov = NeweyWest, from = c(1957, 3), to = c(1991, 3))

plot(fs)

## which looks somewhat similar ...

## Example 8.2

## Ct = b0 + b1*Yt + b2*Y(t-1) + v

fm1 <- dynlm(consumption ~ dpi + L(dpi), data = USMacroG)

## Ct = a0 + a1*Yt + a2*C(t-1) + u

fm2 <- dynlm(consumption ~ dpi + L(consumption), data = USMacroG)

## Cox test in both directions:

coxtest(fm1, fm2)

## ... and do the same for jtest() and encomptest().

## Notice that in this particular case two of them are coincident.

jtest(fm1, fm2)

encomptest(fm1, fm2)

## encomptest could also be performed `by hand' via

fmE <- dynlm(consumption ~ dpi + L(dpi) + L(consumption), data = USMacroG)

waldtest(fm1, fmE, fm2)

## Table 9.1

fm_ols <- lm(consumption ~ dpi, data = as.data.frame(USMacroG))

fm_nls <- nls(consumption ~ alpha + beta * dpi^gamma,

start = list(alpha = coef(fm_ols)[1], beta = coef(fm_ols)[2], gamma = 1),

control = nls.control(maxiter = 100), data = as.data.frame(USMacroG))

summary(fm_ols)

summary(fm_nls)

deviance(fm_ols)

deviance(fm_nls)

vcov(fm_nls)

## Example 9.7

## F test

fm_nls2 <- nls(consumption ~ alpha + beta * dpi,

start = list(alpha = coef(fm_ols)[1], beta = coef(fm_ols)[2]),

control = nls.control(maxiter = 100), data = as.data.frame(USMacroG))

anova(fm_nls, fm_nls2)

## Wald test

linearHypothesis(fm_nls, "gamma = 1")

## Example 9.8, Table 9.2

usm <- USMacroG[, c("m1", "tbill", "gdp")]

fm_lin <- lm(m1 ~ tbill + gdp, data = usm)

fm_log <- lm(m1 ~ tbill + gdp, data = log(usm))

## PE auxiliary regressions

aux_lin <- lm(m1 ~ tbill + gdp + I(fitted(fm_log) - log(fitted(fm_lin))), data = usm)

aux_log <- lm(m1 ~ tbill + gdp + I(fitted(fm_lin) - exp(fitted(fm_log))), data = log(usm))

coeftest(aux_lin)[4,]

coeftest(aux_log)[4,]

## matches results from errata

## With lmtest >= 0.9-24:

## petest(fm_lin, fm_log)

## Example 12.1

fm_m1 <- dynlm(log(m1) ~ log(gdp) + log(cpi), data = USMacroG)

summary(fm_m1)

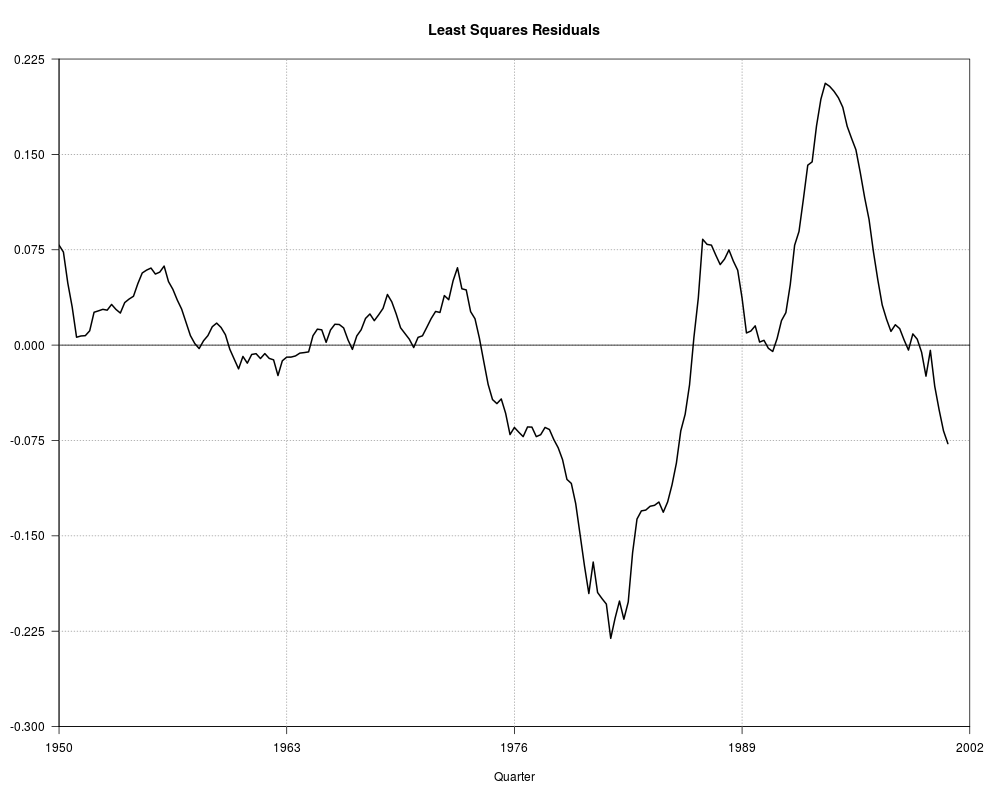

## Figure 12.1

par(las = 1)

plot(0, 0, type = "n", axes = FALSE,

xlim = c(1950, 2002), ylim = c(-0.3, 0.225),

xaxs = "i", yaxs = "i",

xlab = "Quarter", ylab = "", main = "Least Squares Residuals")

box()

axis(1, at = c(1950, 1963, 1976, 1989, 2002))

axis(2, seq(-0.3, 0.225, by = 0.075))

grid(4, 7, col = grey(0.6))

abline(0, 0)

lines(residuals(fm_m1), lwd = 2)

## Example 12.3

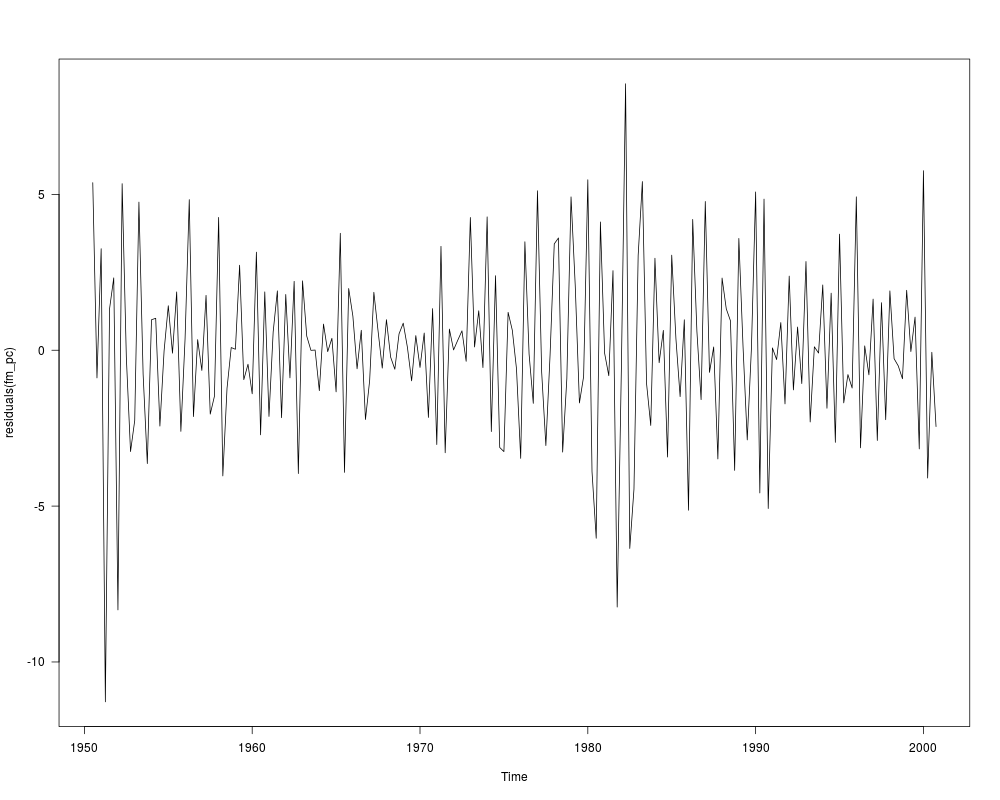

fm_pc <- dynlm(d(inflation) ~ unemp, data = USMacroG)

summary(fm_pc)

## Figure 12.3

plot(residuals(fm_pc))

## natural unemployment rate

coef(fm_pc)[1]/coef(fm_pc)[2]

## autocorrelation

res <- residuals(fm_pc)

summary(dynlm(res ~ L(res)))

## Example 12.4

coeftest(fm_m1)

coeftest(fm_m1, vcov = NeweyWest(fm_m1, lag = 5))

summary(fm_m1)$r.squared

dwtest(fm_m1)

as.vector(acf(residuals(fm_m1), plot = FALSE)$acf)[2]

## matches Tab. 12.1 errata and Greene 6e, apart from Newey-West SE

#################################################

## Cost function of electricity producers 1870 ##

#################################################

## Example 5.6: a generalized Cobb-Douglas cost function

data("Electricity1970", package = "AER")

fm <- lm(log(cost/fuel) ~ log(output) + I(log(output)^2/2) +

log(capital/fuel) + log(labor/fuel), data=Electricity1970[1:123,])

####################################################

## SIC 33: Production for primary metals industry ##

####################################################

## data

data("SIC33", package = "AER")

## Example 6.2

## Translog model

fm_tl <- lm(

output ~ labor + capital + I(0.5 * labor^2) + I(0.5 * capital^2) + I(labor * capital),

data = log(SIC33))

## Cobb-Douglas model

fm_cb <- lm(output ~ labor + capital, data = log(SIC33))

## Table 6.2 in Greene (2003)

deviance(fm_tl)

deviance(fm_cb)

summary(fm_tl)

summary(fm_cb)

vcov(fm_tl)

vcov(fm_cb)

## Cobb-Douglas vs. Translog model

anova(fm_cb, fm_tl)

## hypothesis of constant returns

linearHypothesis(fm_cb, "labor + capital = 1")

###############################

## Cost data for US airlines ##

###############################

## data

data("USAirlines", package = "AER")

## Example 7.2

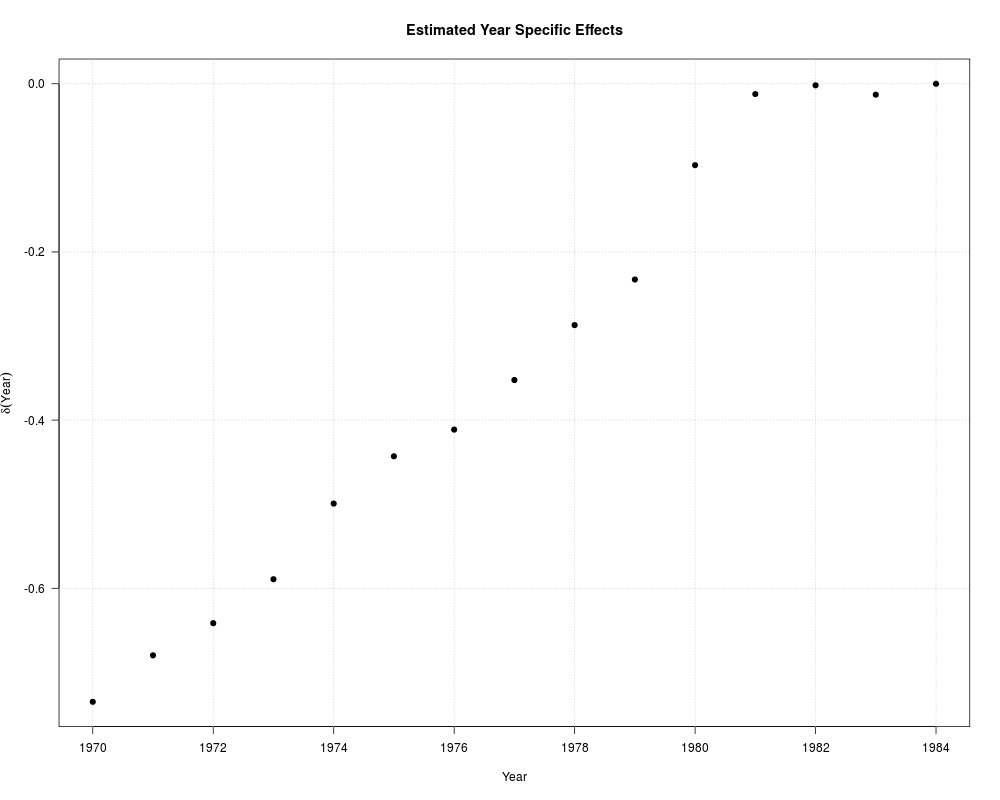

fm_full <- lm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load + year + firm,

data = USAirlines)

fm_time <- lm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load + year,

data = USAirlines)

fm_firm <- lm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load + firm,

data = USAirlines)

fm_no <- lm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load, data = USAirlines)

## full fitted model

coef(fm_full)[1:5]

plot(1970:1984, c(coef(fm_full)[6:19], 0), type = "n",

xlab = "Year", ylab = expression(delta(Year)),

main = "Estimated Year Specific Effects")

grid()

points(1970:1984, c(coef(fm_full)[6:19], 0), pch = 19)

## Table 7.2

anova(fm_full, fm_time)

anova(fm_full, fm_firm)

anova(fm_full, fm_no)

## alternatively, use plm()

library("plm")

usair <- plm.data(USAirlines, c("firm", "year"))

fm_full2 <- plm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load,

data = usair, model = "within", effect = "twoways")

fm_time2 <- plm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load,

data = usair, model = "within", effect = "time")

fm_firm2 <- plm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load,

data = usair, model = "within", effect = "individual")

fm_no2 <- plm(log(cost) ~ log(output) + I(log(output)^2) + log(price) + load,

data = usair, model = "pooling")

pFtest(fm_full2, fm_time2)

pFtest(fm_full2, fm_firm2)

pFtest(fm_full2, fm_no2)

## Example 13.1, Table 13.1

fm_no <- plm(log(cost) ~ log(output) + log(price) + load, data = usair, model = "pooling")

fm_gm <- plm(log(cost) ~ log(output) + log(price) + load, data = usair, model = "between")

fm_firm <- plm(log(cost) ~ log(output) + log(price) + load, data = usair, model = "within")

fm_time <- plm(log(cost) ~ log(output) + log(price) + load, data = usair, model = "within",

effect = "time")

fm_ft <- plm(log(cost) ~ log(output) + log(price) + load, data = usair, model = "within",

effect = "twoways")

summary(fm_no)

summary(fm_gm)

summary(fm_firm)

fixef(fm_firm)

summary(fm_time)

fixef(fm_time)

summary(fm_ft)

fixef(fm_ft, effect = "individual")

fixef(fm_ft, effect = "time")

## Table 13.2

fm_rfirm <- plm(log(cost) ~ log(output) + log(price) + load, data = usair, model = "random")

fm_rft <- plm(log(cost) ~ log(output) + log(price) + load, data = usair, model = "random",

effect = "twoways")

summary(fm_rfirm)

summary(fm_rft)

#################################################

## Cost function of electricity producers 1955 ##

#################################################

## Nerlove data

data("Electricity1955", package = "AER")

Electricity <- Electricity1955[1:145,]

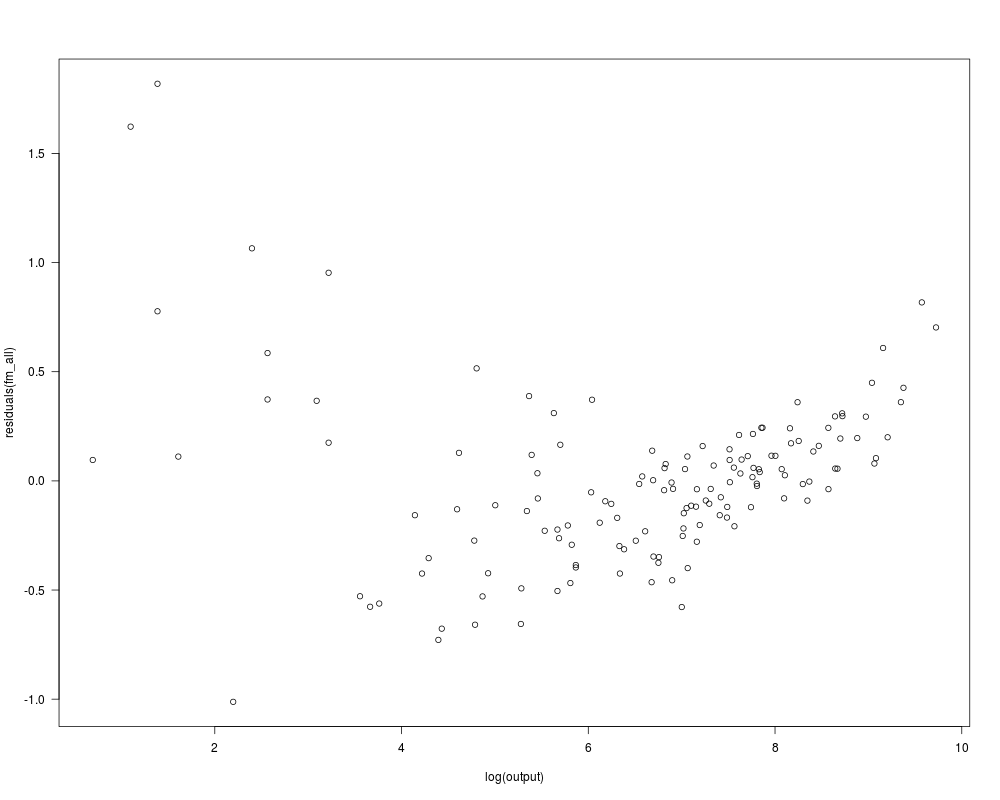

## Example 7.3

## Cobb-Douglas cost function

fm_all <- lm(log(cost/fuel) ~ log(output) + log(labor/fuel) + log(capital/fuel),

data = Electricity)

summary(fm_all)

## hypothesis of constant returns to scale

linearHypothesis(fm_all, "log(output) = 1")

## Figure 7.4

plot(residuals(fm_all) ~ log(output), data = Electricity)

## scaling seems to be different in Greene (2003) with logQ > 10?

## grouped functions

Electricity$group <- with(Electricity, cut(log(output), quantile(log(output), 0:5/5),

include.lowest = TRUE, labels = 1:5))

fm_group <- lm(

log(cost/fuel) ~ group/(log(output) + log(labor/fuel) + log(capital/fuel)) - 1,

data = Electricity)

## Table 7.3 (close, but not quite)

round(rbind(coef(fm_all)[-1], matrix(coef(fm_group), nrow = 5)[,-1]), digits = 3)

## Table 7.4

## log quadratic cost function

fm_all2 <- lm(

log(cost/fuel) ~ log(output) + I(log(output)^2) + log(labor/fuel) + log(capital/fuel),

data = Electricity)

summary(fm_all2)

##########################

## Technological change ##

##########################

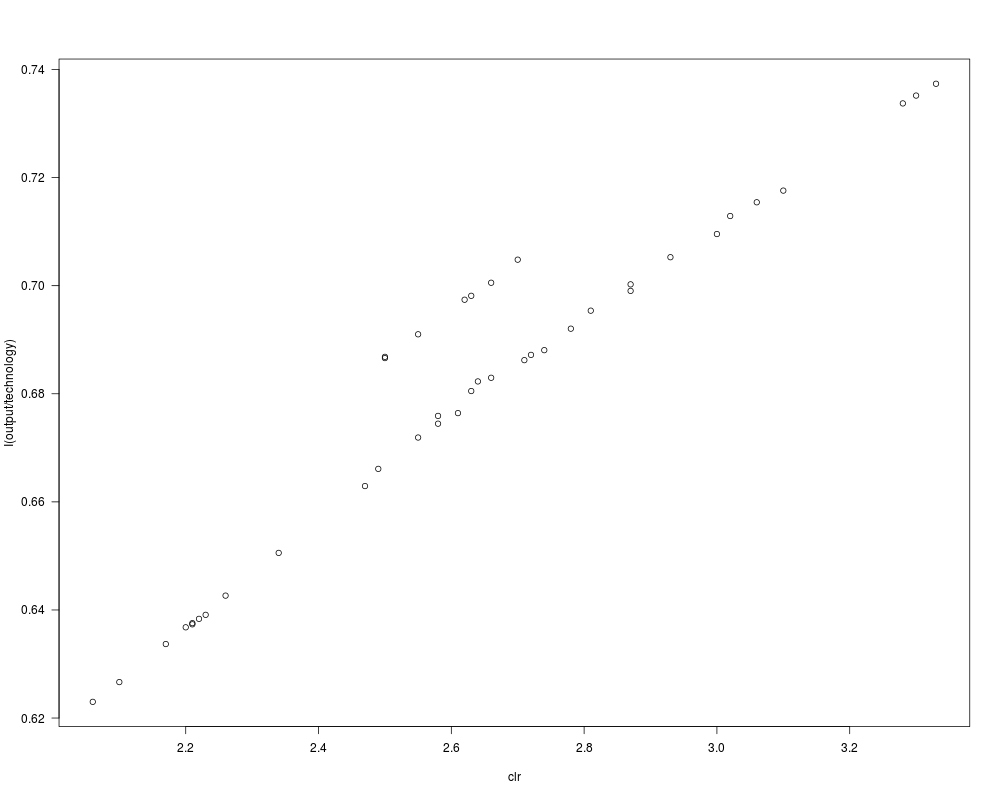

## Exercise 7.1

data("TechChange", package = "AER")

fm1 <- lm(I(output/technology) ~ log(clr), data = TechChange)

fm2 <- lm(I(output/technology) ~ I(1/clr), data = TechChange)

fm3 <- lm(log(output/technology) ~ log(clr), data = TechChange)

fm4 <- lm(log(output/technology) ~ I(1/clr), data = TechChange)

## Exercise 7.2 (a) and (c)

plot(I(output/technology) ~ clr, data = TechChange)

sctest(I(output/technology) ~ log(clr), data = TechChange,

type = "Chow", point = c(1942, 1))

##################################

## Expenditure and default data ##

##################################

## full data set (F21.4)

data("CreditCard", package = "AER")

## extract data set F9.1

ccard <- CreditCard[1:100,]

ccard$income <- round(ccard$income, digits = 2)

ccard$expenditure <- round(ccard$expenditure, digits = 2)

ccard$age <- round(ccard$age + .01)

## suspicious:

CreditCard$age[CreditCard$age < 1]

## the first of these is also in TableF9.1 with 36 instead of 0.5:

ccard$age[79] <- 36

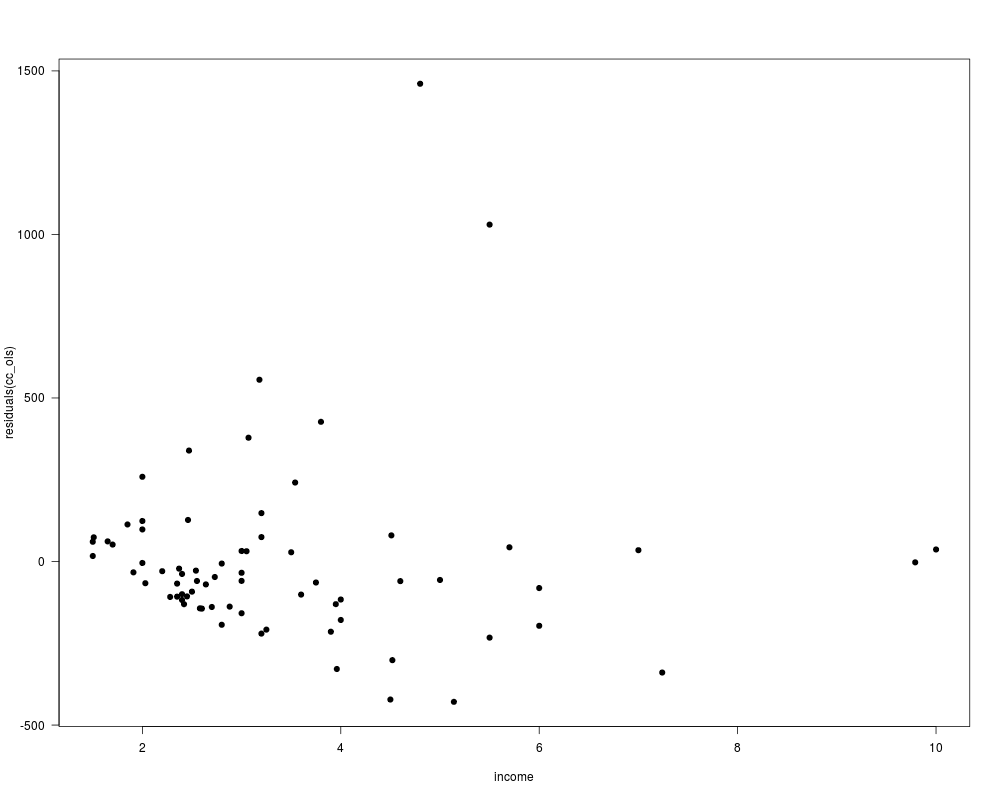

## Example 11.1

ccard <- ccard[order(ccard$income),]

ccard0 <- subset(ccard, expenditure > 0)

cc_ols <- lm(expenditure ~ age + owner + income + I(income^2), data = ccard0)

## Figure 11.1

plot(residuals(cc_ols) ~ income, data = ccard0, pch = 19)

## Table 11.1

mean(ccard$age)

prop.table(table(ccard$owner))

mean(ccard$income)

summary(cc_ols)

sqrt(diag(vcovHC(cc_ols, type = "HC0")))

sqrt(diag(vcovHC(cc_ols, type = "HC2")))

sqrt(diag(vcovHC(cc_ols, type = "HC1")))

bptest(cc_ols, ~ (age + income + I(income^2) + owner)^2 + I(age^2) + I(income^4),

data = ccard0)

gqtest(cc_ols)

bptest(cc_ols, ~ income + I(income^2), data = ccard0, studentize = FALSE)

bptest(cc_ols, ~ income + I(income^2), data = ccard0)

## Table 11.2, WLS and FGLS

cc_wls1 <- lm(expenditure ~ age + owner + income + I(income^2), weights = 1/income,

data = ccard0)

cc_wls2 <- lm(expenditure ~ age + owner + income + I(income^2), weights = 1/income^2,

data = ccard0)

auxreg1 <- lm(log(residuals(cc_ols)^2) ~ log(income), data = ccard0)

cc_fgls1 <- lm(expenditure ~ age + owner + income + I(income^2),

weights = 1/exp(fitted(auxreg1)), data = ccard0)

auxreg2 <- lm(log(residuals(cc_ols)^2) ~ income + I(income^2), data = ccard0)

cc_fgls2 <- lm(expenditure ~ age + owner + income + I(income^2),

weights = 1/exp(fitted(auxreg2)), data = ccard0)

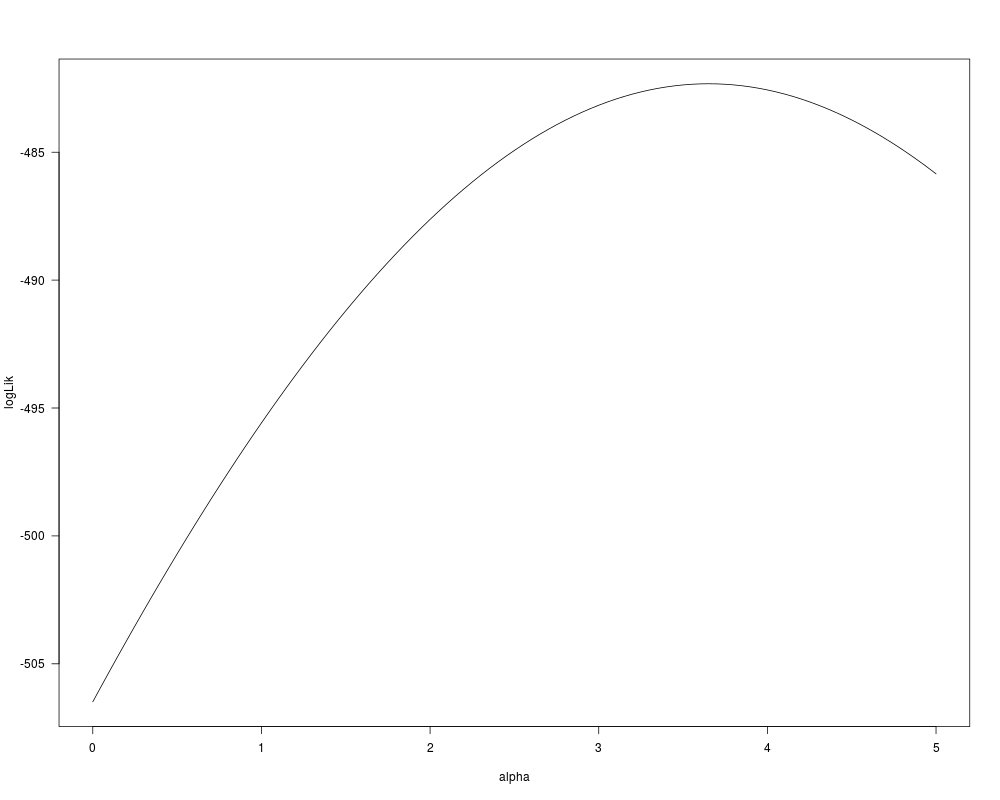

alphai <- coef(lm(log(residuals(cc_ols)^2) ~ log(income), data = ccard0))[2]

alpha <- 0

while(abs((alphai - alpha)/alpha) > 1e-7) {

alpha <- alphai

cc_fgls3 <- lm(expenditure ~ age + owner + income + I(income^2), weights = 1/income^alpha,

data = ccard0)

alphai <- coef(lm(log(residuals(cc_fgls3)^2) ~ log(income), data = ccard0))[2]

}

alpha ## 1.7623 for Greene

cc_fgls3 <- lm(expenditure ~ age + owner + income + I(income^2), weights = 1/income^alpha,

data = ccard0)

llik <- function(alpha)

-logLik(lm(expenditure ~ age + owner + income + I(income^2), weights = 1/income^alpha,

data = ccard0))

plot(0:100/20, -sapply(0:100/20, llik), type = "l", xlab = "alpha", ylab = "logLik")

alpha <- optimize(llik, interval = c(0, 5))$minimum

cc_fgls4 <- lm(expenditure ~ age + owner + income + I(income^2), weights = 1/income^alpha,

data = ccard0)

## Table 11.2

cc_fit <- list(cc_ols, cc_wls1, cc_wls2, cc_fgls2, cc_fgls1, cc_fgls3, cc_fgls4)

t(sapply(cc_fit, coef))

t(sapply(cc_fit, function(obj) sqrt(diag(vcov(obj)))))

## Table 21.21, Poisson and logit models

cc_pois <- glm(reports ~ age + income + expenditure, data = CreditCard, family = poisson)

summary(cc_pois)

logLik(cc_pois)

xhat <- colMeans(CreditCard[, c("age", "income", "expenditure")])

xhat <- as.data.frame(t(xhat))

lambda <- predict(cc_pois, newdata = xhat, type = "response")

ppois(0, lambda) * nrow(CreditCard)

cc_logit <- glm(factor(reports > 0) ~ age + income + owner,

data = CreditCard, family = binomial)

summary(cc_logit)

logLik(cc_logit)

## Table 21.21, "split population model"

library("pscl")

cc_zip <- zeroinfl(reports ~ age + income + expenditure | age + income + owner,

data = CreditCard)

summary(cc_zip)

sum(predict(cc_zip, type = "prob")[,1])

###################################

## DEM/GBP exchange rate returns ##

###################################

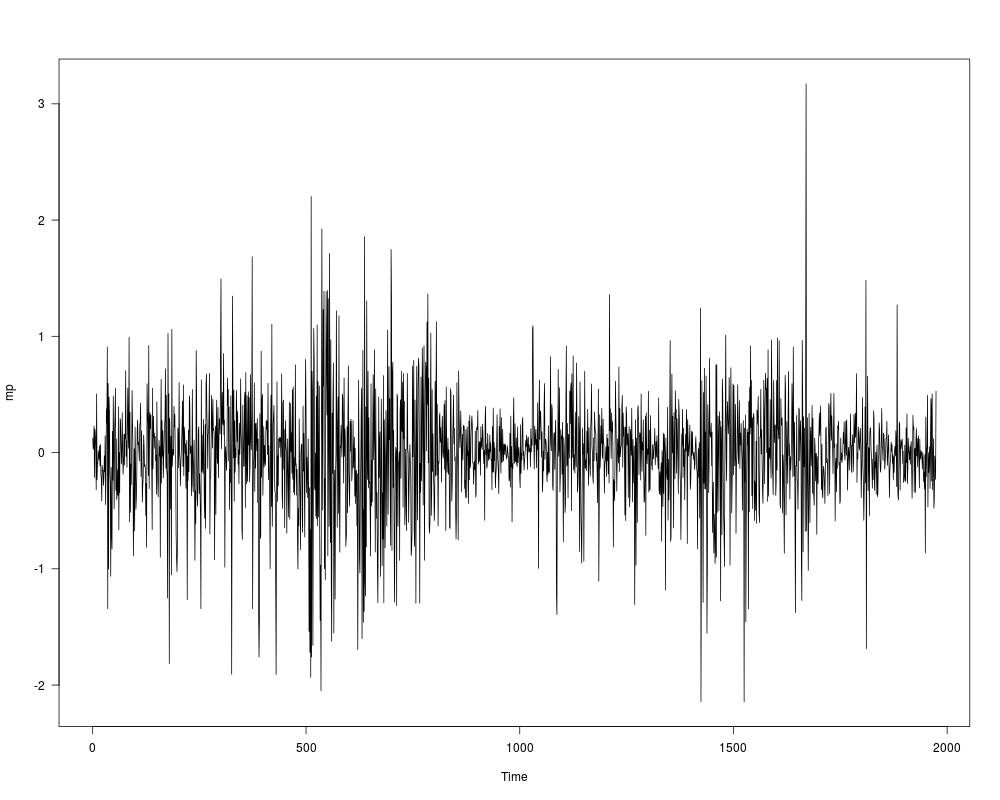

## data as given by Greene (2003)

data("MarkPound")

mp <- round(MarkPound, digits = 6)

## Figure 11.3 in Greene (2003)

plot(mp)

## Example 11.8 in Greene (2003), Table 11.5

library("tseries")

mp_garch <- garch(mp, grad = "numerical")

summary(mp_garch)

logLik(mp_garch)

## Greene (2003) also includes a constant and uses different

## standard errors (presumably computed from Hessian), here

## OPG standard errors are used. garchFit() in "fGarch"

## implements the approach used by Greene (2003).

## compare Errata to Greene (2003)

library("dynlm")

res <- residuals(dynlm(mp ~ 1))^2

mp_ols <- dynlm(res ~ L(res, 1:10))

summary(mp_ols)

logLik(mp_ols)

summary(mp_ols)$r.squared * length(residuals(mp_ols))

################################

## Grunfeld's investment data ##

################################

## subset of data with mistakes

data("Grunfeld", package = "AER")

ggr <- subset(Grunfeld, firm %in% c("General Motors", "US Steel",

"General Electric", "Chrysler", "Westinghouse"))

ggr[c(26, 38), 1] <- c(261.6, 645.2)

ggr[32, 3] <- 232.6

## Tab. 13.4

fm_pool <- lm(invest ~ value + capital, data = ggr)

summary(fm_pool)

logLik(fm_pool)

## White correction

sqrt(diag(vcovHC(fm_pool, type = "HC0")))

## heteroskedastic FGLS

auxreg1 <- lm(residuals(fm_pool)^2 ~ firm - 1, data = ggr)

fm_pfgls <- lm(invest ~ value + capital, data = ggr, weights = 1/fitted(auxreg1))

summary(fm_pfgls)

## ML, computed as iterated FGLS

sigmasi <- fitted(lm(residuals(fm_pfgls)^2 ~ firm - 1 , data = ggr))

sigmas <- 0

while(any(abs((sigmasi - sigmas)/sigmas) > 1e-7)) {

sigmas <- sigmasi

fm_pfgls_i <- lm(invest ~ value + capital, data = ggr, weights = 1/sigmas)

sigmasi <- fitted(lm(residuals(fm_pfgls_i)^2 ~ firm - 1 , data = ggr))

}

fm_pmlh <- lm(invest ~ value + capital, data = ggr, weights = 1/sigmas)

summary(fm_pmlh)

logLik(fm_pmlh)

## Tab. 13.5

auxreg2 <- lm(residuals(fm_pfgls)^2 ~ firm - 1, data = ggr)

auxreg3 <- lm(residuals(fm_pmlh)^2 ~ firm - 1, data = ggr)

rbind(

"OLS" = coef(auxreg1),

"Het. FGLS" = coef(auxreg2),

"Het. ML" = coef(auxreg3))

## Chapter 14: explicitly treat as panel data

library("plm")

pggr <- plm.data(ggr, c("firm", "year"))

## Tab. 14.1

library("systemfit")

fm_sur <- systemfit(invest ~ value + capital, data = pggr, method = "SUR",

methodResidCov = "noDfCor")

fm_psur <- systemfit(invest ~ value + capital, data = pggr, method = "SUR", pooled = TRUE,

methodResidCov = "noDfCor", residCovWeighted = TRUE)

## Tab 14.2

fm_ols <- systemfit(invest ~ value + capital, data = pggr, method = "OLS")

fm_pols <- systemfit(invest ~ value + capital, data = pggr, method = "OLS", pooled = TRUE)

## or "by hand"

fm_gm <- lm(invest ~ value + capital, data = ggr, subset = firm == "General Motors")

mean(residuals(fm_gm)^2) ## Greene uses MLE

## etc.

fm_pool <- lm(invest ~ value + capital, data = ggr)

## Tab. 14.3 (and Tab 13.4, cross-section ML)

## (not run due to long computation time)

## Not run:

fm_ml <- systemfit(invest ~ value + capital, data = pggr, method = "SUR",

methodResidCov = "noDfCor", maxiter = 1000, tol = 1e-10)

fm_pml <- systemfit(invest ~ value + capital, data = pggr, method = "SUR", pooled = TRUE,

methodResidCov = "noDfCor", residCovWeighted = TRUE, maxiter = 1000, tol = 1e-10)

## End(Not run)

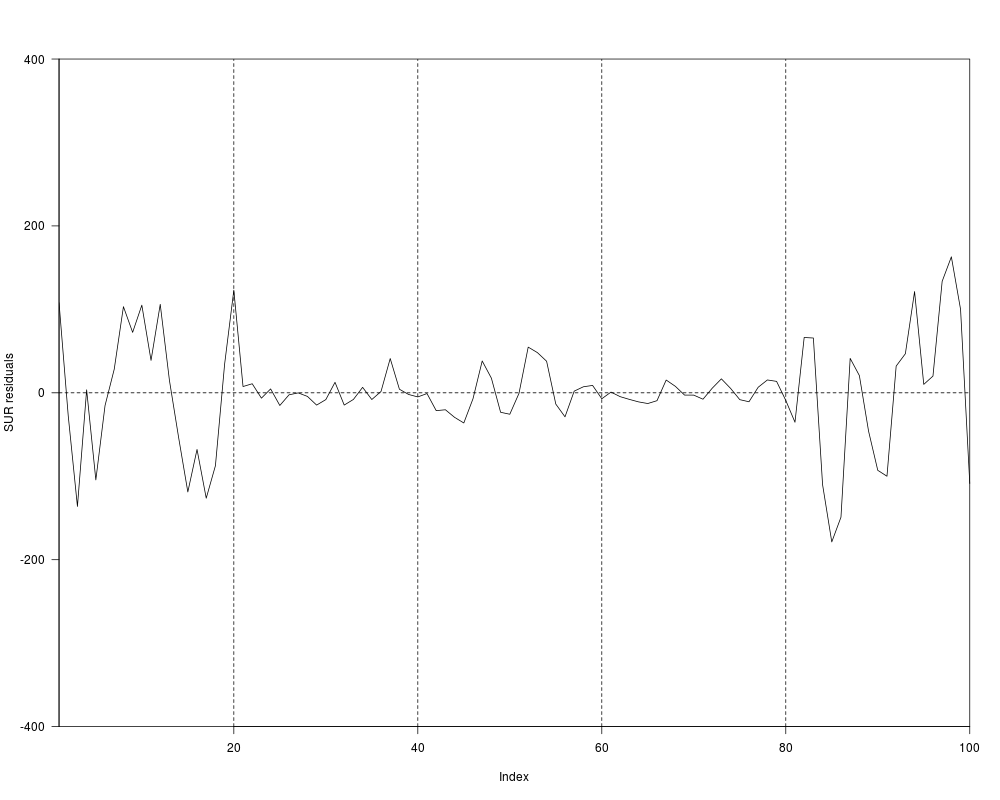

## Fig. 14.2

plot(unlist(residuals(fm_sur)[, c(3, 1, 2, 5, 4)]),

type = "l", ylab = "SUR residuals", ylim = c(-400, 400), xaxs = "i", yaxs = "i")

abline(v = c(20,40,60,80), h = 0, lty = 2)

###################

## Klein model I ##

###################

## data

data("KleinI", package = "AER")

## Tab. 15.3, OLS

library("dynlm")

fm_cons <- dynlm(consumption ~ cprofits + L(cprofits) + I(pwage + gwage), data = KleinI)

fm_inv <- dynlm(invest ~ cprofits + L(cprofits) + capital, data = KleinI)

fm_pwage <- dynlm(pwage ~ gnp + L(gnp) + I(time(gnp) - 1931), data = KleinI)

summary(fm_cons)

summary(fm_inv)

summary(fm_pwage)

## Notes:

## - capital refers to previous year's capital stock -> no lag needed!

## - trend used by Greene (p. 381, "time trend measured as years from 1931")

## Maddala uses years since 1919

## preparation of data frame for systemfit

KI <- ts.intersect(KleinI, lag(KleinI, k = -1), dframe = TRUE)

names(KI) <- c(colnames(KleinI), paste("L", colnames(KleinI), sep = ""))

KI$trend <- (1921:1941) - 1931

library("systemfit")

system <- list(

consumption = consumption ~ cprofits + Lcprofits + I(pwage + gwage),

invest = invest ~ cprofits + Lcprofits + capital,

pwage = pwage ~ gnp + Lgnp + trend)

## Tab. 15.3 OLS again

fm_ols <- systemfit(system, method = "OLS", data = KI)

summary(fm_ols)

## Tab. 15.3 2SLS, 3SLS, I3SLS

inst <- ~ Lcprofits + capital + Lgnp + gexpenditure + taxes + trend + gwage

fm_2sls <- systemfit(system, method = "2SLS", inst = inst,

methodResidCov = "noDfCor", data = KI)

fm_3sls <- systemfit(system, method = "3SLS", inst = inst,

methodResidCov = "noDfCor", data = KI)

fm_i3sls <- systemfit(system, method = "3SLS", inst = inst,

methodResidCov = "noDfCor", maxiter = 100, data = KI)

############################################

## Transportation equipment manufacturing ##

############################################

## data

data("Equipment", package = "AER")

## Example 17.5

## Cobb-Douglas

fm_cd <- lm(log(valueadded/firms) ~ log(capital/firms) + log(labor/firms),

data = Equipment)

## generalized Cobb-Douglas with Zellner-Revankar trafo

GCobbDouglas <- function(theta)

lm(I(log(valueadded/firms) + theta * valueadded/firms) ~ log(capital/firms) + log(labor/firms),

data = Equipment)

## yields classical Cobb-Douglas for theta = 0

fm_cd0 <- GCobbDouglas(0)

## ML estimation of generalized model

## choose starting values from classical model

par0 <- as.vector(c(coef(fm_cd0), 0, mean(residuals(fm_cd0)^2)))

## set up likelihood function

nlogL <- function(par) {

beta <- par[1:3]

theta <- par[4]

sigma2 <- par[5]

Y <- with(Equipment, valueadded/firms)

K <- with(Equipment, capital/firms)

L <- with(Equipment, labor/firms)

rhs <- beta[1] + beta[2] * log(K) + beta[3] * log(L)

lhs <- log(Y) + theta * Y

rval <- sum(log(1 + theta * Y) - log(Y) +

dnorm(lhs, mean = rhs, sd = sqrt(sigma2), log = TRUE))

return(-rval)

}

## optimization

opt <- optim(par0, nlogL, hessian = TRUE)

## Table 17.2

opt$par

sqrt(diag(solve(opt$hessian)))[1:4]

-opt$value

## re-fit ML model

fm_ml <- GCobbDouglas(opt$par[4])

deviance(fm_ml)

sqrt(diag(vcov(fm_ml)))

## fit NLS model

rss <- function(theta) deviance(GCobbDouglas(theta))

optim(0, rss)

opt2 <- optimize(rss, c(-1, 1))

fm_nls <- GCobbDouglas(opt2$minimum)

-nlogL(c(coef(fm_nls), opt2$minimum, mean(residuals(fm_nls)^2)))

############################

## Municipal expenditures ##

############################

## Table 18.2

data("Municipalities", package = "AER")

summary(Municipalities)

###########################

## Program effectiveness ##

###########################

## Table 21.1, col. "Probit"

data("ProgramEffectiveness", package = "AER")

fm_probit <- glm(grade ~ average + testscore + participation,

data = ProgramEffectiveness, family = binomial(link = "probit"))

summary(fm_probit)

####################################

## Labor force participation data ##

####################################

## data and transformations

data("PSID1976", package = "AER")

PSID1976$kids <- with(PSID1976, factor((youngkids + oldkids) > 0,

levels = c(FALSE, TRUE), labels = c("no", "yes")))

PSID1976$nwincome <- with(PSID1976, (fincome - hours * wage)/1000)

## Example 4.1, Table 4.2

## (reproduced in Example 7.1, Table 7.1)

gr_lm <- lm(log(hours * wage) ~ age + I(age^2) + education + kids,

data = PSID1976, subset = participation == "yes")

summary(gr_lm)

vcov(gr_lm)

## Example 4.5

summary(gr_lm)

## or equivalently

gr_lm1 <- lm(log(hours * wage) ~ 1, data = PSID1976, subset = participation == "yes")

anova(gr_lm1, gr_lm)

## Example 21.4, p. 681, and Tab. 21.3, p. 682

gr_probit1 <- glm(participation ~ age + I(age^2) + I(fincome/10000) + education + kids,

data = PSID1976, family = binomial(link = "probit") )

gr_probit2 <- glm(participation ~ age + I(age^2) + I(fincome/10000) + education,

data = PSID1976, family = binomial(link = "probit"))

gr_probit3 <- glm(participation ~ kids/(age + I(age^2) + I(fincome/10000) + education),

data = PSID1976, family = binomial(link = "probit"))

## LR test of all coefficients

lrtest(gr_probit1)

## Chow-type test

lrtest(gr_probit2, gr_probit3)

## equivalently:

anova(gr_probit2, gr_probit3, test = "Chisq")

## Table 21.3

summary(gr_probit1)

## Example 22.8, Table 22.7, p. 786

library("sampleSelection")

gr_2step <- selection(participation ~ age + I(age^2) + fincome + education + kids,

wage ~ experience + I(experience^2) + education + city,

data = PSID1976, method = "2step")

gr_ml <- selection(participation ~ age + I(age^2) + fincome + education + kids,

wage ~ experience + I(experience^2) + education + city,

data = PSID1976, method = "ml")

gr_ols <- lm(wage ~ experience + I(experience^2) + education + city,

data = PSID1976, subset = participation == "yes")

## NOTE: ML estimates agree with Greene, 5e errata.

## Standard errors are based on the Hessian (here), while Greene has BHHH/OPG.

####################

## Ship accidents ##

####################

## subset data

data("ShipAccidents", package = "AER")

sa <- subset(ShipAccidents, service > 0)

## Table 21.20

sa_full <- glm(incidents ~ type + construction + operation, family = poisson,

data = sa, offset = log(service))

summary(sa_full)

sa_notype <- glm(incidents ~ construction + operation, family = poisson,

data = sa, offset = log(service))

summary(sa_notype)

sa_noperiod <- glm(incidents ~ type + operation, family = poisson,

data = sa, offset = log(service))

summary(sa_noperiod)

## model comparison

anova(sa_full, sa_notype, test = "Chisq")

anova(sa_full, sa_noperiod, test = "Chisq")

## test for overdispersion

dispersiontest(sa_full)

dispersiontest(sa_full, trafo = 2)

######################################

## Fair's extramarital affairs data ##

######################################

## data

data("Affairs", package = "AER")

## Tab. 22.3 and 22.4

fm_ols <- lm(affairs ~ age + yearsmarried + religiousness + occupation + rating,

data = Affairs)

fm_probit <- glm(I(affairs > 0) ~ age + yearsmarried + religiousness + occupation + rating,

data = Affairs, family = binomial(link = "probit"))

fm_tobit <- tobit(affairs ~ age + yearsmarried + religiousness + occupation + rating,

data = Affairs)

fm_tobit2 <- tobit(affairs ~ age + yearsmarried + religiousness + occupation + rating,

right = 4, data = Affairs)

fm_pois <- glm(affairs ~ age + yearsmarried + religiousness + occupation + rating,

data = Affairs, family = poisson)

library("MASS")

fm_nb <- glm.nb(affairs ~ age + yearsmarried + religiousness + occupation + rating,

data = Affairs)

## Tab. 22.6

library("pscl")

fm_zip <- zeroinfl(affairs ~ age + yearsmarried + religiousness + occupation + rating | age +

yearsmarried + religiousness + occupation + rating, data = Affairs)

######################

## Strike durations ##

######################

## data and package

data("StrikeDuration", package = "AER")

library("MASS")

## Table 22.10

fit_exp <- fitdistr(StrikeDuration$duration, "exponential")

fit_wei <- fitdistr(StrikeDuration$duration, "weibull")

fit_wei$estimate[2]^(-1)

fit_lnorm <- fitdistr(StrikeDuration$duration, "lognormal")

1/fit_lnorm$estimate[2]

exp(-fit_lnorm$estimate[1])

## Weibull and lognormal distribution have

## different parameterizations, see Greene p. 794

## Example 22.10

library("survival")

fm_wei <- survreg(Surv(duration) ~ uoutput, dist = "weibull", data = StrikeDuration)

summary(fm_wei)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(AER)

Loading required package: car

Loading required package: lmtest

Loading required package: zoo

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numeric

Loading required package: sandwich

Loading required package: survival

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/AER/Greene2003.Rd_%03d_medium.png", width=480, height=480)

> ### Name: Greene2003

> ### Title: Data and Examples from Greene (2003)

> ### Aliases: Greene2003

> ### Keywords: datasets

>

> ### ** Examples

>

> #####################################

> ## US consumption data (1970-1979) ##

> #####################################

>

> ## Example 1.1

> data("USConsump1979", package = "AER")

> plot(expenditure ~ income, data = as.data.frame(USConsump1979), pch = 19)

> fm <- lm(expenditure ~ income, data = as.data.frame(USConsump1979))

> summary(fm)

Call:

lm(formula = expenditure ~ income, data = as.data.frame(USConsump1979))

Residuals:

Min 1Q Median 3Q Max

-11.291 -6.871 1.909 3.418 11.181

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -67.58065 27.91071 -2.421 0.0418 *

income 0.97927 0.03161 30.983 1.28e-09 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 8.193 on 8 degrees of freedom

Multiple R-squared: 0.9917, Adjusted R-squared: 0.9907

F-statistic: 959.9 on 1 and 8 DF, p-value: 1.28e-09

> abline(fm)

>

>

> #####################################

> ## US consumption data (1940-1950) ##

> #####################################

>

> ## data

> data("USConsump1950", package = "AER")

> usc <- as.data.frame(USConsump1950)

> usc$war <- factor(usc$war, labels = c("no", "yes"))

>

> ## Example 2.1

> plot(expenditure ~ income, data = usc, type = "n", xlim = c(225, 375), ylim = c(225, 350))

> with(usc, text(income, expenditure, time(USConsump1950)))

>

> ## single model

> fm <- lm(expenditure ~ income, data = usc)

> summary(fm)

Call:

lm(formula = expenditure ~ income, data = usc)

Residuals:

Min 1Q Median 3Q Max

-35.347 -26.440 9.068 20.000 31.642

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 51.8951 80.8440 0.642 0.5369

income 0.6848 0.2488 2.753 0.0224 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 27.59 on 9 degrees of freedom

Multiple R-squared: 0.4571, Adjusted R-squared: 0.3968

F-statistic: 7.579 on 1 and 9 DF, p-value: 0.02237

>

> ## different intercepts for war yes/no

> fm2 <- lm(expenditure ~ income + war, data = usc)

> summary(fm2)

Call:

lm(formula = expenditure ~ income + war, data = usc)

Residuals:

Min 1Q Median 3Q Max

-14.598 -4.418 -2.352 7.242 11.101

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 14.49540 27.29948 0.531 0.61

income 0.85751 0.08534 10.048 8.19e-06 ***

waryes -50.68974 5.93237 -8.545 2.71e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 9.195 on 8 degrees of freedom

Multiple R-squared: 0.9464, Adjusted R-squared: 0.933

F-statistic: 70.61 on 2 and 8 DF, p-value: 8.26e-06

>

> ## compare

> anova(fm, fm2)

Analysis of Variance Table

Model 1: expenditure ~ income

Model 2: expenditure ~ income + war

Res.Df RSS Df Sum of Sq F Pr(>F)

1 9 6850.0

2 8 676.5 1 6173.5 73.01 2.71e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

>

> ## visualize

> abline(fm, lty = 3)

> abline(coef(fm2)[1:2])

> abline(sum(coef(fm2)[c(1, 3)]), coef(fm2)[2], lty = 2)

>

> ## Example 3.2

> summary(fm)$r.squared

[1] 0.4571345

> summary(lm(expenditure ~ income, data = usc, subset = war == "no"))$r.squared

[1] 0.9369742

> summary(fm2)$r.squared

[1] 0.9463904

>

>

> ########################

> ## US investment data ##

> ########################

>

> data("USInvest", package = "AER")

>

> ## Chapter 3 in Greene (2003)

> ## transform (and round) data to match Table 3.1

> us <- as.data.frame(USInvest)

> us$invest <- round(0.1 * us$invest/us$price, digits = 3)

> us$gnp <- round(0.1 * us$gnp/us$price, digits = 3)

> us$inflation <- c(4.4, round(100 * diff(us$price)/us$price[-15], digits = 2))

> us$trend <- 1:15

> us <- us[, c(2, 6, 1, 4, 5)]

>

> ## p. 22-24

> coef(lm(invest ~ trend + gnp, data = us))

(Intercept) trend gnp

-0.49459760 -0.01700063 0.64781939

> coef(lm(invest ~ gnp, data = us))

(Intercept) gnp

-0.03333061 0.18388271

>

> ## Example 3.1, Table 3.2

> cor(us)[1,-1]

trend gnp interest inflation

0.7514213 0.8648613 0.5876756 0.4817416

> pcor <- solve(cor(us))

> dcor <- 1/sqrt(diag(pcor))

> pcor <- (-pcor * (dcor %o% dcor))[1,-1]

>

> ## Table 3.4

> fm <- lm(invest ~ trend + gnp + interest + inflation, data = us)

> fm1 <- lm(invest ~ 1, data = us)

> anova(fm1, fm)

Analysis of Variance Table

Model 1: invest ~ 1

Model 2: invest ~ trend + gnp + interest + inflation

Res.Df RSS Df Sum of Sq F Pr(>F)

1 14 0.0162736

2 10 0.0004394 4 0.015834 90.089 8.417e-08 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

>

> ## Example 4.1

> set.seed(123)

> w <- rnorm(10000)

> x <- rnorm(10000)

> eps <- 0.5 * w

> y <- 0.5 + 0.5 * x + eps

> b <- rep(0, 500)

> for(i in 1:500) {

+ ix <- sample(1:10000, 100)

+ b[i] <- lm.fit(cbind(1, x[ix]), y[ix])$coef[2]

+ }

> hist(b, breaks = 20, col = "lightgray")

>

>

> ###############################

> ## Longley's regression data ##

> ###############################

>

> ## package and data

> data("Longley", package = "AER")

> library("dynlm")

>

> ## Example 4.6

> fm1 <- dynlm(employment ~ time(employment) + price + gnp + armedforces,

+ data = Longley)

> fm2 <- update(fm1, end = 1961)

> cbind(coef(fm2), coef(fm1))

[,1] [,2]

(Intercept) 1.459415e+06 1.169088e+06

time(employment) -7.217561e+02 -5.764643e+02

price -1.811230e+02 -1.976807e+01

gnp 9.106778e-02 6.439397e-02

armedforces -7.493705e-02 -1.014525e-02

>

> ## Figure 4.3

> plot(rstandard(fm2), type = "b", ylim = c(-3, 3))

> abline(h = c(-2, 2), lty = 2)

>

>

> #########################################

> ## US gasoline market data (1960-1995) ##

> #########################################

>

> ## data

> data("USGasG", package = "AER")

>

> ## Greene (2003)

> ## Example 2.3

> fm <- lm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

+ data = as.data.frame(USGasG))

> summary(fm)

Call:

lm(formula = log(gas/population) ~ log(price) + log(income) +

log(newcar) + log(usedcar), data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.065042 -0.018842 0.001528 0.020786 0.058084

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -12.34184 0.67489 -18.287 <2e-16 ***

log(price) -0.05910 0.03248 -1.819 0.0786 .

log(income) 1.37340 0.07563 18.160 <2e-16 ***

log(newcar) -0.12680 0.12699 -0.998 0.3258

log(usedcar) -0.11871 0.08134 -1.459 0.1545

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.03304 on 31 degrees of freedom

Multiple R-squared: 0.958, Adjusted R-squared: 0.9526

F-statistic: 176.7 on 4 and 31 DF, p-value: < 2.2e-16

>

> ## Example 4.4

> ## estimates and standard errors (note different offset for intercept)

> coef(fm)

(Intercept) log(price) log(income) log(newcar) log(usedcar)

-12.34184054 -0.05909513 1.37339912 -0.12679667 -0.11870847

> sqrt(diag(vcov(fm)))

(Intercept) log(price) log(income) log(newcar) log(usedcar)

0.67489471 0.03248496 0.07562767 0.12699351 0.08133710

> ## confidence interval

> confint(fm, parm = "log(income)")

2.5 % 97.5 %

log(income) 1.219155 1.527643

> ## test linear hypothesis

> linearHypothesis(fm, "log(income) = 1")

Linear hypothesis test

Hypothesis:

log(income) = 1

Model 1: restricted model

Model 2: log(gas/population) ~ log(price) + log(income) + log(newcar) +

log(usedcar)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 32 0.060445

2 31 0.033837 1 0.026608 24.377 2.57e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

>

> ## Figure 7.5

> plot(price ~ gas, data = as.data.frame(USGasG), pch = 19,

+ col = (time(USGasG) > 1973) + 1)

> legend("topleft", legend = c("after 1973", "up to 1973"), pch = 19, col = 2:1, bty = "n")

>

> ## Example 7.6

> ## re-used in Example 8.3

> ## linear time trend

> ltrend <- 1:nrow(USGasG)

> ## shock factor

> shock <- factor(time(USGasG) > 1973, levels = c(FALSE, TRUE), labels = c("before", "after"))

>

> ## 1960-1995

> fm1 <- lm(log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

+ data = as.data.frame(USGasG))

> summary(fm1)

Call:

lm(formula = log(gas/population) ~ log(income) + log(price) +

log(newcar) + log(usedcar) + ltrend, data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.055238 -0.017715 0.003659 0.016481 0.053522

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -17.385790 1.679289 -10.353 2.03e-11 ***

log(income) 1.954626 0.192854 10.135 3.34e-11 ***

log(price) -0.115530 0.033479 -3.451 0.00168 **

log(newcar) 0.205282 0.152019 1.350 0.18700

log(usedcar) -0.129274 0.071412 -1.810 0.08028 .

ltrend -0.019118 0.005957 -3.210 0.00316 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.02898 on 30 degrees of freedom

Multiple R-squared: 0.9687, Adjusted R-squared: 0.9635

F-statistic: 185.8 on 5 and 30 DF, p-value: < 2.2e-16

> ## pooled

> fm2 <- lm(

+ log(gas/population) ~ shock + log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

+ data = as.data.frame(USGasG))

> summary(fm2)

Call:

lm(formula = log(gas/population) ~ shock + log(income) + log(price) +

log(newcar) + log(usedcar) + ltrend, data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.045360 -0.019697 0.003931 0.015112 0.047550

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -16.374402 1.456263 -11.244 4.33e-12 ***

shockafter 0.077311 0.021872 3.535 0.00139 **

log(income) 1.838167 0.167258 10.990 7.43e-12 ***

log(price) -0.178005 0.033508 -5.312 1.06e-05 ***

log(newcar) 0.209842 0.129267 1.623 0.11534

log(usedcar) -0.128132 0.060721 -2.110 0.04359 *

ltrend -0.016862 0.005105 -3.303 0.00255 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.02464 on 29 degrees of freedom

Multiple R-squared: 0.9781, Adjusted R-squared: 0.9736

F-statistic: 216.3 on 6 and 29 DF, p-value: < 2.2e-16

> ## segmented

> fm3 <- lm(

+ log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) + log(usedcar) + ltrend),

+ data = as.data.frame(USGasG))

> summary(fm3)

Call:

lm(formula = log(gas/population) ~ shock/(log(income) + log(price) +

log(newcar) + log(usedcar) + ltrend), data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.027349 -0.006332 0.001295 0.007159 0.022016

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -4.13439 5.03963 -0.820 0.420075

shockafter -4.74111 5.51576 -0.860 0.398538

shockbefore:log(income) 0.42400 0.57973 0.731 0.471633

shockafter:log(income) 1.01408 0.24904 4.072 0.000439 ***

shockbefore:log(price) 0.09455 0.24804 0.381 0.706427

shockafter:log(price) -0.24237 0.03490 -6.946 3.5e-07 ***

shockbefore:log(newcar) 0.58390 0.21670 2.695 0.012665 *

shockafter:log(newcar) 0.33017 0.15789 2.091 0.047277 *

shockbefore:log(usedcar) -0.33462 0.15215 -2.199 0.037738 *

shockafter:log(usedcar) -0.05537 0.04426 -1.251 0.222972

shockbefore:ltrend 0.02637 0.01762 1.497 0.147533

shockafter:ltrend -0.01262 0.00329 -3.835 0.000798 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.01488 on 24 degrees of freedom

Multiple R-squared: 0.9934, Adjusted R-squared: 0.9904

F-statistic: 328.5 on 11 and 24 DF, p-value: < 2.2e-16

>

> ## Chow test

> anova(fm3, fm1)

Analysis of Variance Table

Model 1: log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

log(usedcar) + ltrend)

Model 2: log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + ltrend

Res.Df RSS Df Sum of Sq F Pr(>F)

1 24 0.0053144

2 30 0.0251878 -6 -0.019873 14.958 4.595e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> library("strucchange")

> sctest(log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

+ data = USGasG, point = c(1973, 1), type = "Chow")

Chow test

data: log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + ltrend

F = 14.958, p-value = 4.595e-07

> ## Recursive CUSUM test

> rcus <- efp(log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + ltrend,

+ data = USGasG, type = "Rec-CUSUM")

> plot(rcus)

> sctest(rcus)

Recursive CUSUM test

data: rcus

S = 1.4977, p-value = 0.0002437

> ## Note: Greene's remark that the break is in 1984 (where the process crosses its boundary)

> ## is wrong. The break appears to be no later than 1976.

>

> ## Example 12.2

> library("dynlm")

> resplot <- function(obj, bound = TRUE) {

+ res <- residuals(obj)

+ sigma <- summary(obj)$sigma

+ plot(res, ylab = "Residuals", xlab = "Year")

+ grid()

+ abline(h = 0)

+ if(bound) abline(h = c(-2, 2) * sigma, col = "red")

+ lines(res)

+ }

> resplot(dynlm(log(gas/population) ~ log(price), data = USGasG))

> resplot(dynlm(log(gas/population) ~ log(price) + log(income), data = USGasG))

> resplot(dynlm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar) +

+ log(transport) + log(nondurable) + log(durable) +log(service) + ltrend, data = USGasG))

> ## different shock variable than in 7.6

> shock <- factor(time(USGasG) > 1974, levels = c(FALSE, TRUE), labels = c("before", "after"))

> resplot(dynlm(log(gas/population) ~ shock/(log(price) + log(income) + log(newcar) + log(usedcar) +

+ log(transport) + log(nondurable) + log(durable) + log(service) + ltrend), data = USGasG))

> ## NOTE: something seems to be wrong with the sigma estimates in the `full' models

>

> ## Table 12.4, OLS

> fm <- dynlm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

+ data = USGasG)

> summary(fm)

Time series regression with "ts" data:

Start = 1960, End = 1995

Call:

dynlm(formula = log(gas/population) ~ log(price) + log(income) +

log(newcar) + log(usedcar), data = USGasG)

Residuals:

Min 1Q Median 3Q Max

-0.065042 -0.018842 0.001528 0.020786 0.058084

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -12.34184 0.67489 -18.287 <2e-16 ***

log(price) -0.05910 0.03248 -1.819 0.0786 .

log(income) 1.37340 0.07563 18.160 <2e-16 ***

log(newcar) -0.12680 0.12699 -0.998 0.3258

log(usedcar) -0.11871 0.08134 -1.459 0.1545

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.03304 on 31 degrees of freedom

Multiple R-squared: 0.958, Adjusted R-squared: 0.9526

F-statistic: 176.7 on 4 and 31 DF, p-value: < 2.2e-16

> resplot(fm, bound = FALSE)

> dwtest(fm)

Durbin-Watson test

data: fm

DW = 0.6047, p-value = 3.387e-09

alternative hypothesis: true autocorrelation is greater than 0

>

> ## ML

> g <- as.data.frame(USGasG)

> y <- log(g$gas/g$population)

> X <- as.matrix(cbind(log(g$price), log(g$income), log(g$newcar), log(g$usedcar)))

> arima(y, order = c(1, 0, 0), xreg = X)

Call:

arima(x = y, order = c(1, 0, 0), xreg = X)

Coefficients:

ar1 intercept X1 X2 X3 X4

0.9304 -9.7548 -0.2082 1.0818 0.0884 -0.0350

s.e. 0.0554 1.1262 0.0337 0.1269 0.1186 0.0612

sigma^2 estimated as 0.0003094: log likelihood = 93.37, aic = -172.74

>

>

> #######################################

> ## US macroeconomic data (1950-2000) ##

> #######################################

> ## data and trend

> data("USMacroG", package = "AER")

> ltrend <- 0:(nrow(USMacroG) - 1)

>

> ## Example 5.3

> ## OLS and IV regression

> library("dynlm")

> fm_ols <- dynlm(consumption ~ gdp, data = USMacroG)

> fm_iv <- dynlm(consumption ~ gdp | L(consumption) + L(gdp), data = USMacroG)

>

> ## Hausman statistic

> library("MASS")

> b_diff <- coef(fm_iv) - coef(fm_ols)

> v_diff <- summary(fm_iv)$cov.unscaled - summary(fm_ols)$cov.unscaled

> (t(b_diff) %*% ginv(v_diff) %*% b_diff) / summary(fm_ols)$sigma^2

[,1]

[1,] 9.703933

>

> ## Wu statistic

> auxreg <- dynlm(gdp ~ L(consumption) + L(gdp), data = USMacroG)

> coeftest(dynlm(consumption ~ gdp + fitted(auxreg), data = USMacroG))[3,3]

[1] 4.944502

> ## agrees with Greene (but not with errata)

>

> ## Example 6.1

> ## Table 6.1

> fm6.1 <- dynlm(log(invest) ~ tbill + inflation + log(gdp) + ltrend, data = USMacroG)

> fm6.3 <- dynlm(log(invest) ~ I(tbill - inflation) + log(gdp) + ltrend, data = USMacroG)

> summary(fm6.1)

Time series regression with "ts" data:

Start = 1950(2), End = 2000(4)

Call:

dynlm(formula = log(invest) ~ tbill + inflation + log(gdp) +

ltrend, data = USMacroG)

Residuals:

Min 1Q Median 3Q Max

-0.22313 -0.05540 -0.00312 0.04246 0.31989

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -9.134091 1.366459 -6.684 2.3e-10 ***

tbill -0.008598 0.003195 -2.691 0.00774 **

inflation 0.003306 0.002337 1.415 0.15872

log(gdp) 1.930156 0.183272 10.532 < 2e-16 ***

ltrend -0.005659 0.001488 -3.803 0.00019 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.08618 on 198 degrees of freedom

Multiple R-squared: 0.9798, Adjusted R-squared: 0.9793

F-statistic: 2395 on 4 and 198 DF, p-value: < 2.2e-16

> summary(fm6.3)

Time series regression with "ts" data:

Start = 1950(2), End = 2000(4)

Call:

dynlm(formula = log(invest) ~ I(tbill - inflation) + log(gdp) +

ltrend, data = USMacroG)

Residuals:

Min 1Q Median 3Q Max

-0.227897 -0.054542 -0.002435 0.039993 0.313928

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -7.907158 1.200631 -6.586 3.94e-10 ***

I(tbill - inflation) -0.004427 0.002270 -1.950 0.05260 .

log(gdp) 1.764062 0.160561 10.987 < 2e-16 ***

ltrend -0.004403 0.001331 -3.308 0.00111 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.0867 on 199 degrees of freedom

Multiple R-squared: 0.9794, Adjusted R-squared: 0.9791

F-statistic: 3154 on 3 and 199 DF, p-value: < 2.2e-16

> deviance(fm6.1)

[1] 1.470565

> deviance(fm6.3)

[1] 1.495811

> vcov(fm6.1)[2,3]

[1] -3.717454e-06

>

> ## F test

> linearHypothesis(fm6.1, "tbill + inflation = 0")

Linear hypothesis test

Hypothesis:

tbill + inflation = 0

Model 1: restricted model

Model 2: log(invest) ~ tbill + inflation + log(gdp) + ltrend

Res.Df RSS Df Sum of Sq F Pr(>F)

1 199 1.4958

2 198 1.4706 1 0.025246 3.3991 0.06673 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> ## alternatively

> anova(fm6.1, fm6.3)

Analysis of Variance Table

Model 1: log(invest) ~ tbill + inflation + log(gdp) + ltrend

Model 2: log(invest) ~ I(tbill - inflation) + log(gdp) + ltrend

Res.Df RSS Df Sum of Sq F Pr(>F)

1 198 1.4706

2 199 1.4958 -1 -0.025246 3.3991 0.06673 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> ## t statistic

> sqrt(anova(fm6.1, fm6.3)[2,5])

[1] 1.843672

>

> ## Example 6.3

> ## Distributed lag model:

> ## log(Ct) = b0 + b1 * log(Yt) + b2 * log(C(t-1)) + u

> us <- log(USMacroG[, c(2, 5)])

> fm_distlag <- dynlm(log(consumption) ~ log(dpi) + L(log(consumption)),

+ data = USMacroG)

> summary(fm_distlag)

Time series regression with "ts" data:

Start = 1950(2), End = 2000(4)

Call:

dynlm(formula = log(consumption) ~ log(dpi) + L(log(consumption)),

data = USMacroG)

Residuals:

Min 1Q Median 3Q Max

-0.035243 -0.004606 0.000496 0.005147 0.041754

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.003142 0.010553 0.298 0.76624

log(dpi) 0.074958 0.028727 2.609 0.00976 **

L(log(consumption)) 0.924625 0.028594 32.337 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.008742 on 200 degrees of freedom

Multiple R-squared: 0.9997, Adjusted R-squared: 0.9997

F-statistic: 3.476e+05 on 2 and 200 DF, p-value: < 2.2e-16

>

> ## estimate and test long-run MPC

> coef(fm_distlag)[2]/(1-coef(fm_distlag)[3])

log(dpi)

0.9944606

> linearHypothesis(fm_distlag, "log(dpi) + L(log(consumption)) = 1")

Linear hypothesis test

Hypothesis:

log(dpi) + L(log(consumption)) = 1

Model 1: restricted model

Model 2: log(consumption) ~ log(dpi) + L(log(consumption))

Res.Df RSS Df Sum of Sq F Pr(>F)

1 201 0.015295

2 200 0.015286 1 9.1197e-06 0.1193 0.7301

> ## correct, see errata

>

> ## Example 6.4

> ## predict investiment in 2001(1)

> predict(fm6.1, interval = "prediction",

+ newdata = data.frame(tbill = 4.48, inflation = 5.262, gdp = 9316.8, ltrend = 204))

fit lwr upr

1 7.331178 7.158229 7.504126

>

> ## Example 7.7

> ## no GMM available in "strucchange"

> ## using OLS instead yields

> fs <- Fstats(log(m1/cpi) ~ log(gdp) + tbill, data = USMacroG,

+ vcov = NeweyWest, from = c(1957, 3), to = c(1991, 3))

> plot(fs)

> ## which looks somewhat similar ...

>

> ## Example 8.2

> ## Ct = b0 + b1*Yt + b2*Y(t-1) + v

> fm1 <- dynlm(consumption ~ dpi + L(dpi), data = USMacroG)

> ## Ct = a0 + a1*Yt + a2*C(t-1) + u

> fm2 <- dynlm(consumption ~ dpi + L(consumption), data = USMacroG)

>

> ## Cox test in both directions:

> coxtest(fm1, fm2)

Cox test

Model 1: consumption ~ dpi + L(dpi)

Model 2: consumption ~ dpi + L(consumption)

Estimate Std. Error z value Pr(>|z|)

fitted(M1) ~ M2 -284.908 0.01862 -15304.2817 < 2.2e-16 ***

fitted(M2) ~ M1 1.491 0.42735 3.4894 0.0004842 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> ## ... and do the same for jtest() and encomptest().

> ## Notice that in this particular case two of them are coincident.

> jtest(fm1, fm2)

J test

Model 1: consumption ~ dpi + L(dpi)

Model 2: consumption ~ dpi + L(consumption)

Estimate Std. Error t value Pr(>|t|)

M1 + fitted(M2) 1.0145 0.01614 62.8605 < 2.2e-16 ***

M2 + fitted(M1) -10.6766 1.48542 -7.1876 1.299e-11 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> encomptest(fm1, fm2)

Encompassing test

Model 1: consumption ~ dpi + L(dpi)

Model 2: consumption ~ dpi + L(consumption)

Model E: consumption ~ dpi + L(dpi) + L(consumption)

Res.Df Df F Pr(>F)

M1 vs. ME 199 -1 3951.448 < 2.2e-16 ***

M2 vs. ME 199 -1 51.661 1.299e-11 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> ## encomptest could also be performed `by hand' via

> fmE <- dynlm(consumption ~ dpi + L(dpi) + L(consumption), data = USMacroG)

> waldtest(fm1, fmE, fm2)

Wald test

Model 1: consumption ~ dpi + L(dpi)

Model 2: consumption ~ dpi + L(dpi) + L(consumption)

Model 3: consumption ~ dpi + L(consumption)

Res.Df Df F Pr(>F)

1 200

2 199 1 3951.448 < 2.2e-16 ***

3 200 -1 51.661 1.299e-11 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

>

> ## Table 9.1

> fm_ols <- lm(consumption ~ dpi, data = as.data.frame(USMacroG))

> fm_nls <- nls(consumption ~ alpha + beta * dpi^gamma,

+ start = list(alpha = coef(fm_ols)[1], beta = coef(fm_ols)[2], gamma = 1),

+ control = nls.control(maxiter = 100), data = as.data.frame(USMacroG))

> summary(fm_ols)

Call:

lm(formula = consumption ~ dpi, data = as.data.frame(USMacroG))

Residuals:

Min 1Q Median 3Q Max

-191.42 -56.08 1.38 49.53 324.14

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -80.354749 14.305852 -5.617 6.38e-08 ***

dpi 0.921686 0.003872 238.054 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 87.21 on 202 degrees of freedom

Multiple R-squared: 0.9964, Adjusted R-squared: 0.9964

F-statistic: 5.667e+04 on 1 and 202 DF, p-value: < 2.2e-16

> summary(fm_nls)

Formula: consumption ~ alpha + beta * dpi^gamma

Parameters:

Estimate Std. Error t value Pr(>|t|)

alpha 458.79851 22.50141 20.390 <2e-16 ***

beta 0.10085 0.01091 9.244 <2e-16 ***

gamma 1.24483 0.01205 103.263 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 50.09 on 201 degrees of freedom

Number of iterations to convergence: 64

Achieved convergence tolerance: 1.695e-06

> deviance(fm_ols)

[1] 1536322

> deviance(fm_nls)

[1] 504403.2

> vcov(fm_nls)

alpha beta gamma

alpha 506.3136444 -0.2345464437 0.2575688047

beta -0.2345464 0.0001190377 -0.0001314916

gamma 0.2575688 -0.0001314916 0.0001453206

>

> ## Example 9.7

> ## F test

> fm_nls2 <- nls(consumption ~ alpha + beta * dpi,

+ start = list(alpha = coef(fm_ols)[1], beta = coef(fm_ols)[2]),

+ control = nls.control(maxiter = 100), data = as.data.frame(USMacroG))

> anova(fm_nls, fm_nls2)

Analysis of Variance Table

Model 1: consumption ~ alpha + beta * dpi^gamma

Model 2: consumption ~ alpha + beta * dpi

Res.Df Res.Sum Sq Df Sum Sq F value Pr(>F)

1 201 504403

2 202 1536322 -1 -1031919 411.21 < 2.2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> ## Wald test

> linearHypothesis(fm_nls, "gamma = 1")

Linear hypothesis test

Hypothesis:

gamma = 1

Model 1: restricted model

Model 2: consumption ~ alpha + beta * dpi^gamma

Res.Df Df Chisq Pr(>Chisq)

1 202

2 201 1 412.47 < 2.2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

>

> ## Example 9.8, Table 9.2

> usm <- USMacroG[, c("m1", "tbill", "gdp")]

> fm_lin <- lm(m1 ~ tbill + gdp, data = usm)

> fm_log <- lm(m1 ~ tbill + gdp, data = log(usm))

> ## PE auxiliary regressions

> aux_lin <- lm(m1 ~ tbill + gdp + I(fitted(fm_log) - log(fitted(fm_lin))), data = usm)

> aux_log <- lm(m1 ~ tbill + gdp + I(fitted(fm_lin) - exp(fitted(fm_log))), data = log(usm))

> coeftest(aux_lin)[4,]

Estimate Std. Error t value Pr(>|t|)

2.093544e+02 2.675803e+01 7.823985e+00 2.900156e-13

> coeftest(aux_log)[4,]

Estimate Std. Error t value Pr(>|t|)

-4.188803e-05 2.613270e-04 -1.602897e-01 8.728146e-01

> ## matches results from errata

> ## With lmtest >= 0.9-24:

> ## petest(fm_lin, fm_log)

>

> ## Example 12.1

> fm_m1 <- dynlm(log(m1) ~ log(gdp) + log(cpi), data = USMacroG)

> summary(fm_m1)

Time series regression with "ts" data:

Start = 1950(1), End = 2000(4)

Call:

dynlm(formula = log(m1) ~ log(gdp) + log(cpi), data = USMacroG)

Residuals:

Min 1Q Median 3Q Max

-0.230620 -0.026026 0.008483 0.036407 0.205929

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -1.63306 0.22857 -7.145 1.62e-11 ***

log(gdp) 0.28705 0.04738 6.058 6.68e-09 ***

log(cpi) 0.97181 0.03377 28.775 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.08288 on 201 degrees of freedom

Multiple R-squared: 0.9895, Adjusted R-squared: 0.9894

F-statistic: 9489 on 2 and 201 DF, p-value: < 2.2e-16

>

> ## Figure 12.1

> par(las = 1)

> plot(0, 0, type = "n", axes = FALSE,

+ xlim = c(1950, 2002), ylim = c(-0.3, 0.225),

+ xaxs = "i", yaxs = "i",

+ xlab = "Quarter", ylab = "", main = "Least Squares Residuals")

> box()

> axis(1, at = c(1950, 1963, 1976, 1989, 2002))

> axis(2, seq(-0.3, 0.225, by = 0.075))

> grid(4, 7, col = grey(0.6))

> abline(0, 0)

> lines(residuals(fm_m1), lwd = 2)

>

> ## Example 12.3

> fm_pc <- dynlm(d(inflation) ~ unemp, data = USMacroG)

> summary(fm_pc)

Time series regression with "ts" data:

Start = 1950(3), End = 2000(4)

Call:

dynlm(formula = d(inflation) ~ unemp,

|