Given the portfolio weights and a toy market, the function Invest simulates the growth of $1 of the corresponding portfolio and that of the benchmark.

Usage

Invest(market, weight, plot = TRUE)

Arguments

market

a toymkt object.

weight

the portfolio weights. The portfolio weights must be non-negative and sum to one (full investment with no short sales). It can be a zoo object or matrix/dataframe whose number of rows is at least as large as that of market$R. If the number of rows of weight is larger than required, only the initial rows will be used. weight can also be a numeric vector whose length is equal to the number of columns of market$R (the number of assets). In the latter case the portfolio is assumed to be constant-weighted through out.

plot

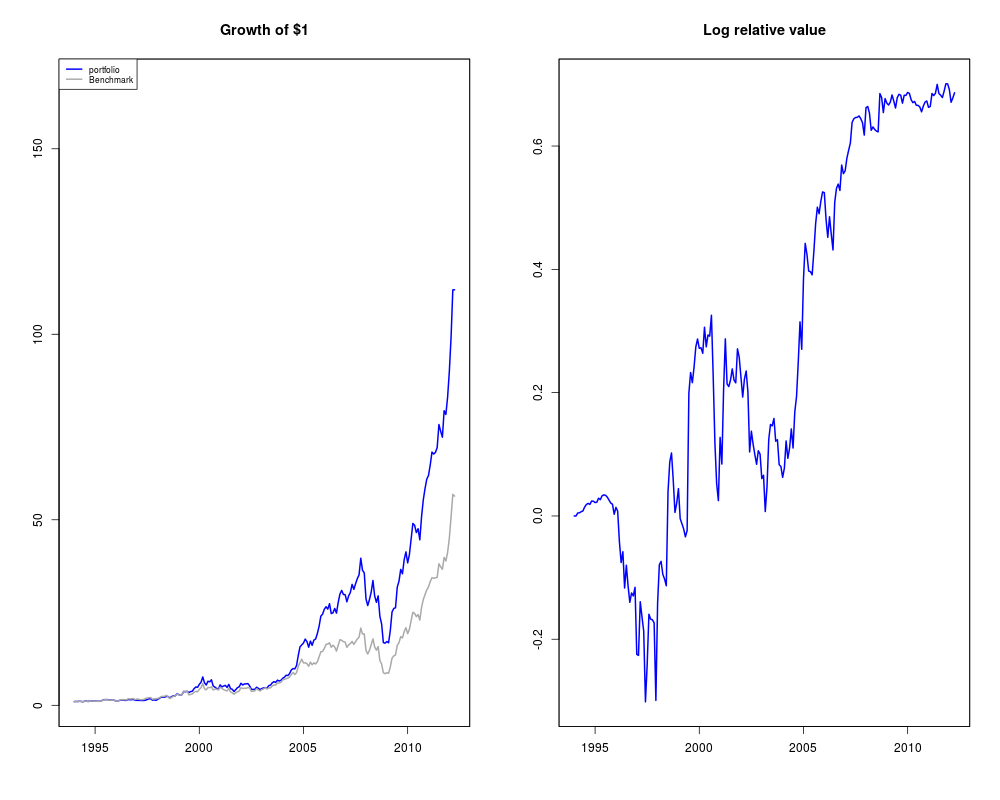

TRUE or FALSE. If TRUE, the growth of $1 of the portfolio will be plotted together with the growth of $1 of the market portfolio. The default value is TRUE.

Details

The relative value in the second plot is the ratio of the growth of $1 of the portfolio to that of the benchmark. It is called relative because the value is normalized by the value of the benchmark portfolio.

Value

A list containing the following components.

growth

a zoo object representing the growth of $1 of the portfolio and the benchmark.

R

a zoo object of simple returns of the two portfolios.

r

a zoo object of log returns of the two portfolios.

See Also

toymkt

Examples

# Performance of the equal-weighted portfolio

data(applestarbucks)

market <- toymkt(applestarbucks)

weight <- c(0.5, 0.5) # equal-weighted portfolio

result <- Invest(market, weight, plot = TRUE)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(RelValAnalysis)

Loading required package: zoo

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numeric

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/RelValAnalysis/Invest.Rd_%03d_medium.png", width=480, height=480)

> ### Name: Invest

> ### Title: Investing in a Toy Market

> ### Aliases: Invest

>

> ### ** Examples

>

> # Performance of the equal-weighted portfolio

> data(applestarbucks)

> market <- toymkt(applestarbucks)

Warning message:

In toymkt(applestarbucks) :

Since initial.weight is not given, the benchmark is assumed to be equal-weighted initially.

> weight <- c(0.5, 0.5) # equal-weighted portfolio

> result <- Invest(market, weight, plot = TRUE)

Warning message:

In Invest(market, weight, plot = TRUE) :

Since only one weight vector is supplied, the portfolio is assumed to be constant-weighted.

>

>

>

>

>

> dev.off()

null device

1

>

.

.