Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Brownian motion, Brownian bridge, geometric Brownian motion, and arithmetic Brownian motion simulatorsDescriptionThe (S3) generic function for simulation of brownian motion, brownian bridge, geometric brownian motion, and arithmetic brownian motion. UsageBM(N, ...) BB(N, ...) GBM(N, ...) ABM(N, ...) ## Default S3 method: BM(N =100,M=1,x0=0,t0=0,T=1,Dt, ...) ## Default S3 method: BB(N =100,M=1,x0=0,y=1,t0=0,T=1,Dt, ...) ## Default S3 method: GBM(N =100,M=1,x0=1,t0=0,T=1,Dt,theta=1,sigma=1, ...) ## Default S3 method: ABM(N =100,M=1,x0=0,t0=0,T=1,Dt,theta=1,sigma=1, ...) Arguments

DetailsThe function The function dX(t) = ((y-X(t))/(T-t)) dt + dW(t) The function dX(t) = theta X(t) dt + sigma X(t) dW(t) The function dX(t) = theta dt + sigma dW(t) Value

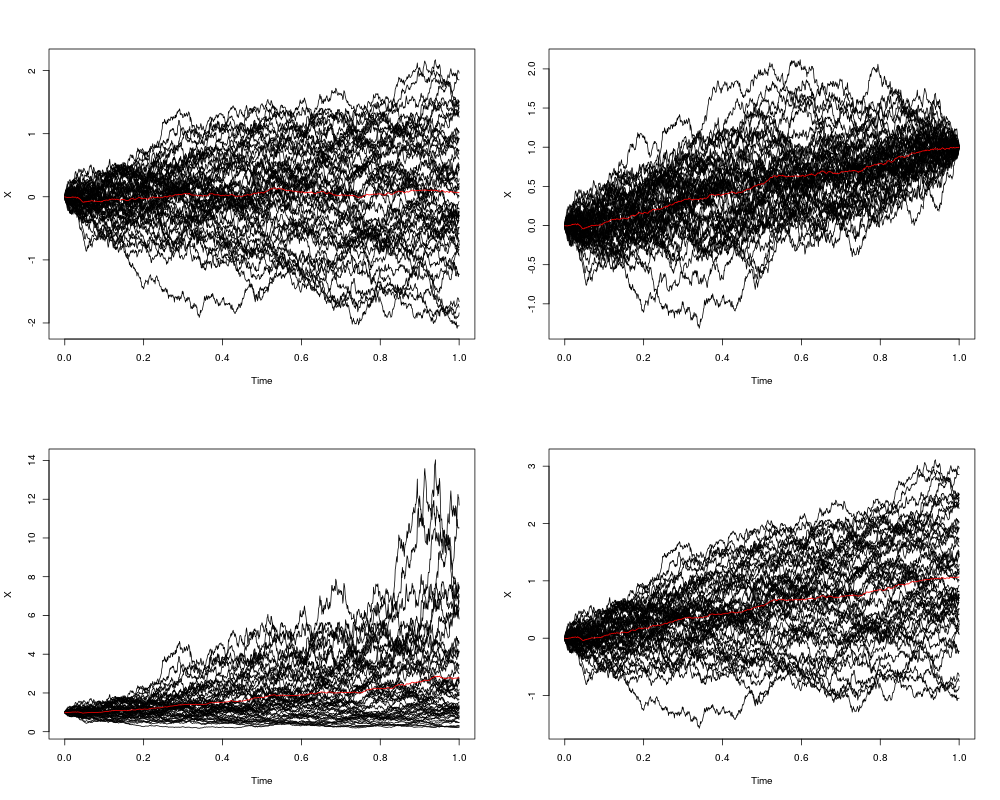

Author(s)A.C. Guidoum, K. Boukhetala. ReferencesAllen, E. (2007). Modeling with Ito stochastic differential equations. Springer-Verlag, New York. Jedrzejewski, F. (2009). Modeles aleatoires et physique probabiliste. Springer-Verlag, New York. Henderson, D and Plaschko, P. (2006). Stochastic differential equations in science and engineering. World Scientific. See AlsoThis functions Examplesop <- par(mfrow = c(2, 2)) ## Brownian motion set.seed(1234) X <- BM(N = 1000, M = 50) plot(X,plot.type="single") lines(as.vector(time(X)),rowMeans(X),col="red") ## Brownian bridge set.seed(1234) X <- BB(N = 1000, M =50) plot(X,plot.type="single") lines(as.vector(time(X)),rowMeans(X),col="red") ## Geometric Brownian motion set.seed(1234) X <- GBM(N = 1000, M = 50) plot(X,plot.type="single") lines(as.vector(time(X)),rowMeans(X),col="red") ## Arithmetic Brownian motion set.seed(1234) X <- ABM(N = 1000, M = 50) plot(X,plot.type="single") lines(as.vector(time(X)),rowMeans(X),col="red") par(op) Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(Sim.DiffProc)

Package 'Sim.DiffProc' version 3.2 loaded.

help(Sim.DiffProc) for summary information.

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/Sim.DiffProc/ABM.Rd_%03d_medium.png", width=480, height=480)

> ### Name: BM

> ### Title: Brownian motion, Brownian bridge, geometric Brownian motion, and

> ### arithmetic Brownian motion simulators

> ### Aliases: ABM BB BM GBM ABM.default BB.default BM.default GBM.default

> ### Keywords: BM sde ts

>

> ### ** Examples

>

>

> op <- par(mfrow = c(2, 2))

>

> ## Brownian motion

> set.seed(1234)

> X <- BM(N = 1000, M = 50)

> plot(X,plot.type="single")

> lines(as.vector(time(X)),rowMeans(X),col="red")

>

> ## Brownian bridge

> set.seed(1234)

> X <- BB(N = 1000, M =50)

> plot(X,plot.type="single")

> lines(as.vector(time(X)),rowMeans(X),col="red")

>

> ## Geometric Brownian motion

> set.seed(1234)

> X <- GBM(N = 1000, M = 50)

> plot(X,plot.type="single")

> lines(as.vector(time(X)),rowMeans(X),col="red")

>

> ## Arithmetic Brownian motion

> set.seed(1234)

> X <- ABM(N = 1000, M = 50)

> plot(X,plot.type="single")

> lines(as.vector(time(X)),rowMeans(X),col="red")

>

> par(op)

>

>

>

>

>

> dev.off()

null device

1

>

|