Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

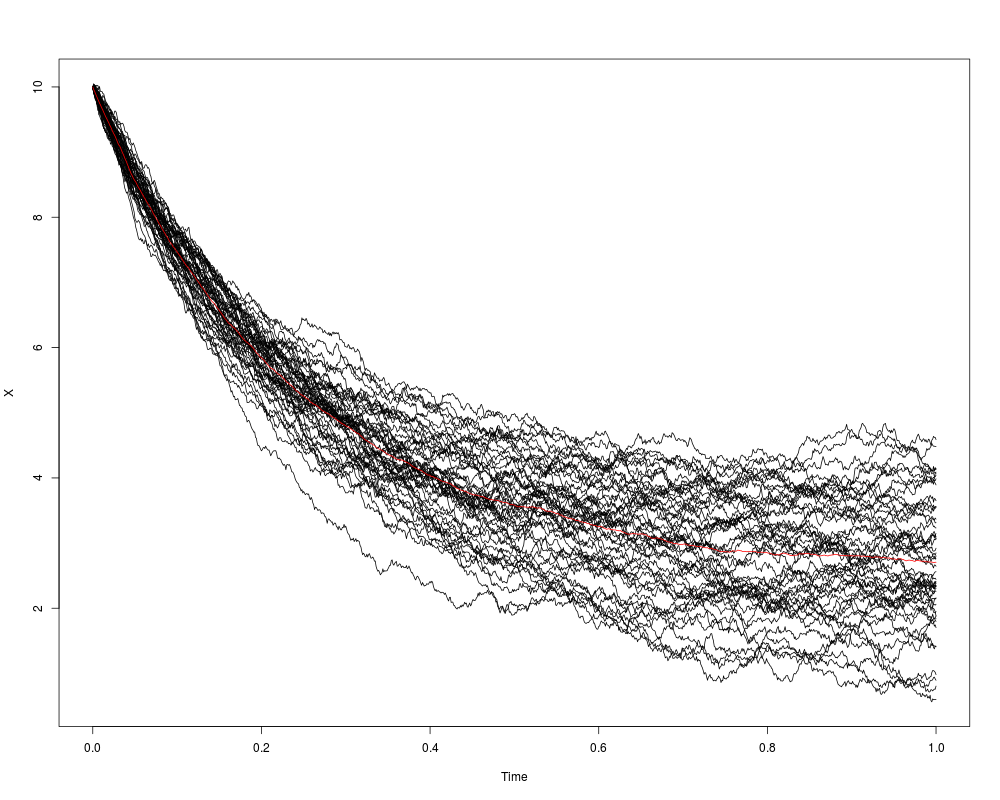

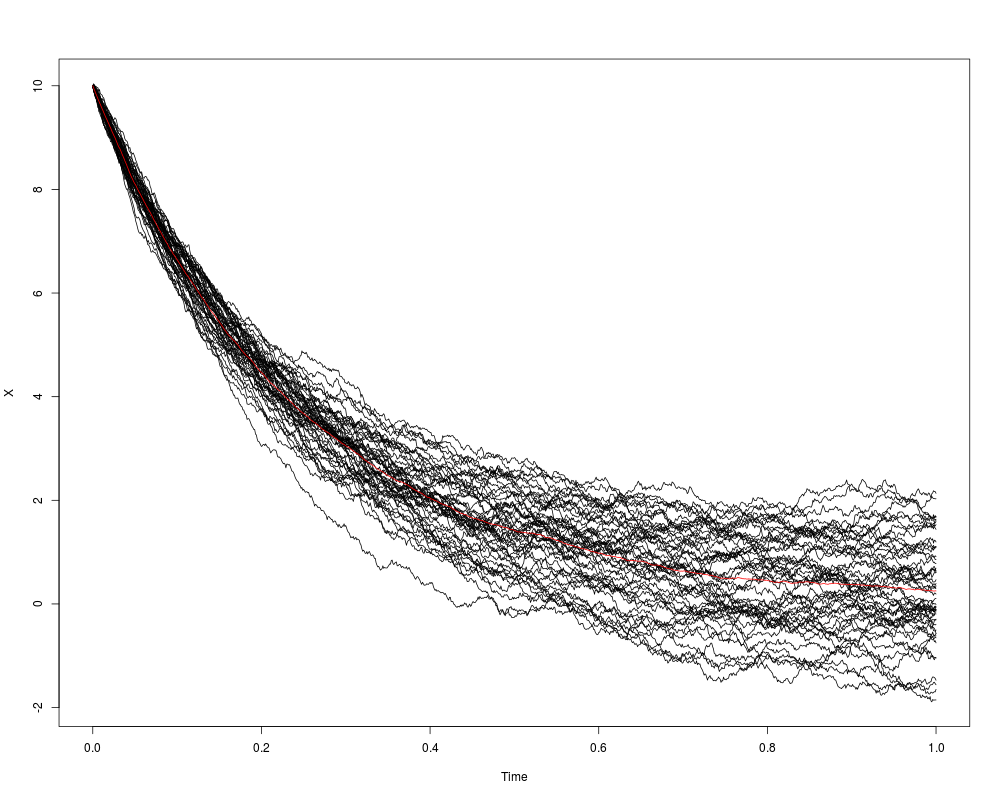

Hull-White/Vasicek, Ornstein-Uhlenbeck processDescriptionThe (S3) generic function for simulation of Hull-White/Vasicek or gaussian diffusion models, and Ornstein-Uhlenbeck process. UsageHWV(N, ...) OU(N, ...) ## Default S3 method: HWV(N = 100, M = 1, x0 = 2, t0 = 0, T = 1, Dt, mu = 4, theta = 1, sigma = 0.1, ...) ## Default S3 method: OU(N =100,M=1,x0=2,t0=0,T=1,Dt,mu=4,sigma=0.2, ...) Arguments

DetailsThe function dX(t) = mu *( theta- X(t)) dt + sigma dW(t) The function dX(t) = -mu * X(t) dt + sigma dW(t) Constraints: mu, sigma >0. Please note that the process is stationary only if mu >0. Value

Author(s)A.C. Guidoum, K. Boukhetala. ReferencesVasicek, O. (1977). An Equilibrium Characterization of the Term Structure. Journal of Financial Economics, 5, 177–188. See Also

Examples## Hull-White/Vasicek Models ## dX(t) = 4 * (2.5 - X(t)) * dt + 1 *dW(t), X0=10 set.seed(1234) X <- HWV(N=1000,M=50,mu = 4, theta = 2.5,sigma = 1,x0=10) plot(X,plot.type="single") lines(as.vector(time(X)),rowMeans(X),col="red") ## Ornstein-Uhlenbeck Process ## dX(t) = -4 * X(t) * dt + 1 *dW(t) , X0=2 set.seed(1234) X <- OU(N=1000,M=50,mu = 4,sigma = 1,x0=10) plot(X,plot.type="single") lines(as.vector(time(X)),rowMeans(X),col="red") Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(Sim.DiffProc)

Package 'Sim.DiffProc' version 3.2 loaded.

help(Sim.DiffProc) for summary information.

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/Sim.DiffProc/HWV.Rd_%03d_medium.png", width=480, height=480)

> ### Name: HWV

> ### Title: Hull-White/Vasicek, Ornstein-Uhlenbeck process

> ### Aliases: HWV OU HWV.default OU.default

> ### Keywords: sde ts

>

> ### ** Examples

>

> ## Hull-White/Vasicek Models

> ## dX(t) = 4 * (2.5 - X(t)) * dt + 1 *dW(t), X0=10

> set.seed(1234)

>

> X <- HWV(N=1000,M=50,mu = 4, theta = 2.5,sigma = 1,x0=10)

> plot(X,plot.type="single")

> lines(as.vector(time(X)),rowMeans(X),col="red")

>

> ## Ornstein-Uhlenbeck Process

> ## dX(t) = -4 * X(t) * dt + 1 *dW(t) , X0=2

> set.seed(1234)

>

> X <- OU(N=1000,M=50,mu = 4,sigma = 1,x0=10)

> plot(X,plot.type="single")

> lines(as.vector(time(X)),rowMeans(X),col="red")

>

>

>

>

>

> dev.off()

null device

1

>

|