Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Maximum Pseudo-Likelihood Estimation of 1-Dim SDEDescriptionThe (S3) generic function Usage

fitsde(data, ...)

## Default S3 method:

fitsde(data, drift, diffusion, start = list(), pmle = c("euler","kessler",

"ozaki", "shoji"), optim.method = "L-BFGS-B",

lower = -Inf, upper = Inf, ...)

## S3 method for class 'fitsde'

summary(object, ...)

## S3 method for class 'fitsde'

coef(object, ...)

## S3 method for class 'fitsde'

vcov(object, ...)

## S3 method for class 'fitsde'

logLik(object, ...)

## S3 method for class 'fitsde'

AIC(object, ...)

## S3 method for class 'fitsde'

BIC(object, ...)

## S3 method for class 'fitsde'

confint(object,parm, level=0.95, ...)

Arguments

DetailsThe function The For more details see Value

Author(s)A.C. Guidoum, K. Boukhetala. ReferencesKessler, M. (1997). Estimation of an ergodic diffusion from discrete observations. Scand. J. Statist., 24, 211-229. Iacus, S.M. (2008). Simulation and inference for stochastic differential equations: with R examples. Springer-Verlag, New York. Iacus, S.M. (2009). sde: Simulation and Inference for Stochastic Differential Equations. R package version 2.0.10. Iacus, S.M. and all. (2014). The yuima Project: A Computational Framework for Simulation and Inference of Stochastic Differential Equations. Journal of Statistical Software, 57(4). Ozaki, T. (1992). A bridge between nonlinear time series models and nonlinear stochastic dynamical systems: A local linearization approach. Statistica Sinica, 2, 25-83. Shoji, L., Ozaki, T. (1998). Estimation for nonlinear stochastic differential equations by a local linearization method. Stochastic Analysis and Applications, 16, 733-752. Dacunha, D.C. and Florens, D.Z. (1986). Estimation of the Coefficients of a Diffusion from Discrete Observations. Stochastics. 19, 263–284. Dohnal, G. (1987). On estimating the diffusion coefficient. J. Appl.Prob., 24, 105–114. Genon, V.C. (1990). Maximum constrast estimation for diffusion processes from discrete observation. Statistics, 21, 99–116. Nicolau, J. (2004). Introduction to the estimation of stochastic differential equations based on discrete observations. Autumn School and International Conference, Stochastic Finance. Ait-Sahalia, Y. (1999). Transition densities for interest rate and other nonlinear diffusions. The Journal of Finance, 54, 1361–1395. Ait-Sahalia, Y. (2002). Maximum likelihood estimation of discretely sampled diffusions: a closed-form approximation approach. Econometrica. 70, 223–262. B.L.S. Prakasa Rao. (1999). Statistical Inference for Diffusion Type Processes. Arnold, London and Oxford University press, New York. Kutoyants, Y.A. (2004). Statistical Inference for Ergodic Diffusion Processes. Springer, London. See Also

Examples

##### Example 1:

## Modele GBM (BS)

## dX(t) = theta1 * X(t) * dt + theta2 * x * dW(t)

## Simulation of data

set.seed(1234)

X <- GBM(N =1000,theta=4,sigma=1)

## Estimation: true theta=c(4,1)

fx <- expression(theta[1]*x)

gx <- expression(theta[2]*x)

fres <- fitsde(data=X,drift=fx,diffusion=gx,start = list(theta1=1,theta2=1),

lower=c(0,0))

fres

summary(fres)

coef(fres)

logLik(fres)

AIC(fres)

BIC(fres)

vcov(fres)

confint(fres,level=0.95)

##### Example 2:

## Nonlinear mean reversion (Ait-Sahalia) modele

## dX(t) = (theta1 + theta2*x + theta3*x^2) * dt + theta4 * x^theta5 * dW(t)

## Simulation of the process X(t)

set.seed(1234)

f <- expression(1 - 11*x + 2*x^2)

g <- expression(x^0.5)

res <- snssde1d(drift=f,diffusion=g,M=1,N=1000,Dt=0.001,x0=5)

mydata1 <- res$X

## Estimation

## true param theta= c(1,-11,2,1,0.5)

true <- c(1,-11,2,1,0.5)

pmle <- eval(formals(fitsde.default)$pmle)

fx <- expression(theta[1] + theta[2]*x + theta[3]*x^2)

gx <- expression(theta[4]*x^theta[5])

fres <- lapply(1:4, function(i) fitsde(mydata1,drift=fx,diffusion=gx,

pmle=pmle[i],start = list(theta1=1,theta2=1,theta3=1,theta4=1,

theta5=1),optim.method = "L-BFGS-B"))

Coef <- data.frame(true,do.call("cbind",lapply(1:4,function(i) coef(fres[[i]]))))

names(Coef) <- c("True",pmle)

Summary <- data.frame(do.call("rbind",lapply(1:4,function(i) logLik(fres[[i]]))),

do.call("rbind",lapply(1:4,function(i) AIC(fres[[i]]))),

do.call("rbind",lapply(1:4,function(i) BIC(fres[[i]]))),

row.names=pmle)

names(Summary) <- c("logLik","AIC","BIC")

Coef

Summary

##### Example 3:

## dX(t) = (theta1*x*t+theta2*tan(x)) *dt + theta3*t *dW(t)

## Simulation of data

set.seed(1234)

f <- expression(2*x*t-tan(x))

g <- expression(1.25*t)

sim <- snssde1d(drift=f,diffusion=g,M=1,N=1000,Dt=0.001,x0=10)

mydata2 <- sim$X

## Estimation

## true param theta= c(2,-1,1.25)

true <- c(2,-1,1.25)

fx <- expression(theta[1]*x*t+theta[2]*tan(x))

gx <- expression(theta[3]*t)

fres <- lapply(1:4, function(i) fitsde(mydata2,drift=fx,diffusion=gx,

pmle=pmle[i],start = list(theta1=1,theta2=1,theta3=1),

optim.method = "L-BFGS-B"))

Coef <- data.frame(true,do.call("cbind",lapply(1:4,function(i) coef(fres[[i]]))))

names(Coef) <- c("True",pmle)

Summary <- data.frame(do.call("rbind",lapply(1:4,function(i) logLik(fres[[i]]))),

do.call("rbind",lapply(1:4,function(i) AIC(fres[[i]]))),

do.call("rbind",lapply(1:4,function(i) BIC(fres[[i]]))),

row.names=pmle)

names(Summary) <- c("logLik","AIC","BIC")

Coef

Summary

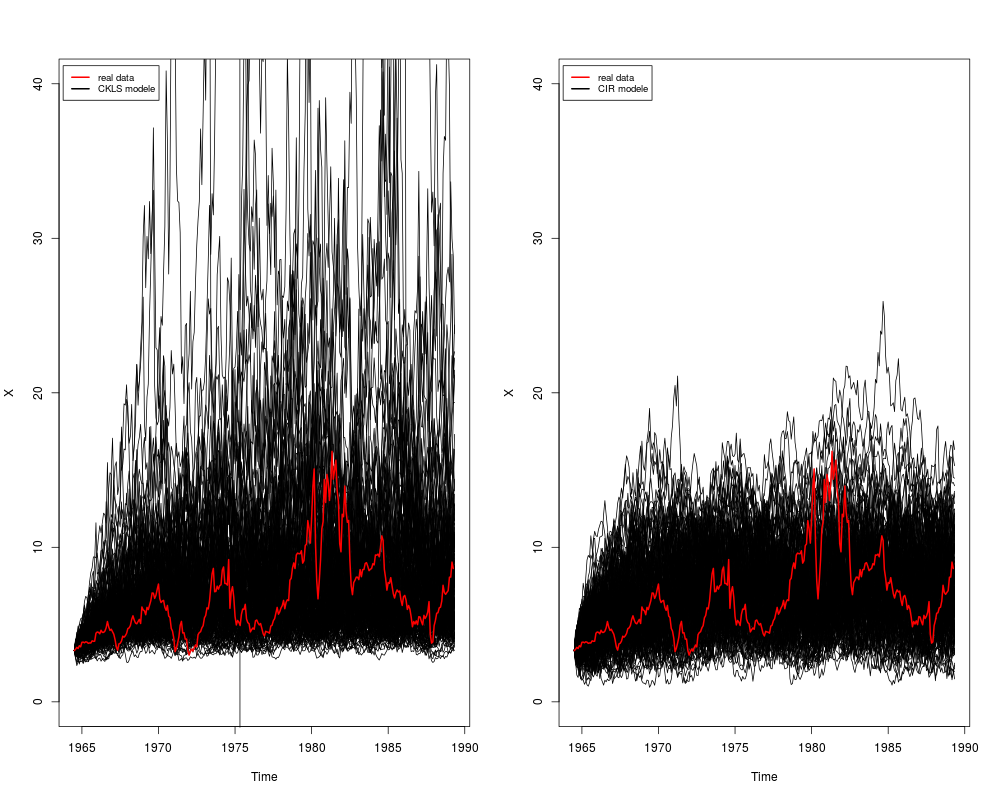

##### Example 4:

## Application to real data

## CKLS modele vs CIR modele

## CKLS (mod1): dX(t) = (theta1+theta2* X(t))* dt + theta3 * X(t)^theta4 * dW(t)

## CIR (mod2): dX(t) = (theta1+theta2* X(t))* dt + theta3 * sqrt(X(t)) * dW(t)

set.seed(1234)

data(Irates)

rates <- Irates[,"r1"]

rates <- window(rates, start=1964.471, end=1989.333)

fx1 <- expression(theta[1]+theta[2]*x)

gx1 <- expression(theta[3]*x^theta[4])

gx2 <- expression(theta[3]*sqrt(x))

fitmod1 <- fitsde(rates,drift=fx1,diffusion=gx1,pmle="euler",start = list(theta1=1,theta2=1,

theta3=1,theta4=1),optim.method = "L-BFGS-B")

fitmod2 <- fitsde(rates,drift=fx1,diffusion=gx2,pmle="euler",start = list(theta1=1,theta2=1,

theta3=1),optim.method = "L-BFGS-B")

summary(fitmod1)

summary(fitmod2)

coef(fitmod1)

coef(fitmod2)

confint(fitmod1,parm=c('theta2','theta3'))

confint(fitmod2,parm=c('theta2','theta3'))

AIC(fitmod1)

AIC(fitmod2)

## Display

## CKLS Modele

op <- par(mfrow = c(1, 2))

theta <- coef(fitmod1)

N <- length(rates)

res <- snssde1d(drift=fx1,diffusion=gx1,M=200,t0=time(rates)[1],T=time(rates)[N],

Dt=deltat(rates),x0=rates[1],N)

plot(res,plot.type="single",ylim=c(0,40))

lines(rates,col=2,lwd=2)

legend("topleft",c("real data","CKLS modele"),inset = .01,col=c(2,1),lwd=2,cex=0.8)

## CIR Modele

theta <- coef(fitmod2)

res <- snssde1d(drift=fx1,diffusion=gx2,M=200,t0=time(rates)[1],T=time(rates)[N],

Dt=deltat(rates),x0=rates[1],N)

plot(res,plot.type="single",ylim=c(0,40))

lines(rates,col=2,lwd=2)

legend("topleft",c("real data","CIR modele"),inset = .01,col=c(2,1),lwd=2,cex=0.8)

par(op)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(Sim.DiffProc)

Package 'Sim.DiffProc' version 3.2 loaded.

help(Sim.DiffProc) for summary information.

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/Sim.DiffProc/fitsde.Rd_%03d_medium.png", width=480, height=480)

> ### Name: fitsde

> ### Title: Maximum Pseudo-Likelihood Estimation of 1-Dim SDE

> ### Aliases: fitsde fitsde.default summary.fitsde print.fitsde vcov.fitsde

> ### AIC.fitsde BIC.fitsde logLik.fitsde coef.fitsde confint.fitsde

> ### Keywords: fit ts sde

>

> ### ** Examples

>

> ##### Example 1:

>

> ## Modele GBM (BS)

> ## dX(t) = theta1 * X(t) * dt + theta2 * x * dW(t)

> ## Simulation of data

> set.seed(1234)

>

> X <- GBM(N =1000,theta=4,sigma=1)

> ## Estimation: true theta=c(4,1)

> fx <- expression(theta[1]*x)

> gx <- expression(theta[2]*x)

>

> fres <- fitsde(data=X,drift=fx,diffusion=gx,start = list(theta1=1,theta2=1),

+ lower=c(0,0))

> fres

Call:

fitsde(data = X, drift = fx, diffusion = gx, start = list(theta1 = 1,

theta2 = 1), lower = c(0, 0))

Coefficients:

theta1 theta2

3.160720 1.000225

> summary(fres)

Pseudo maximum likelihood estimation

Method: Euler

Call:

fitsde(data = X, drift = fx, diffusion = gx, start = list(theta1 = 1,

theta2 = 1), lower = c(0, 0))

Coefficients:

Estimate Std. Error

theta1 3.160720 1.00022484

theta2 1.000225 0.02236563

-2 log L: -1330.008

> coef(fres)

theta1 theta2

3.160720 1.000225

> logLik(fres)

[1] 665.004

> AIC(fres)

[1] -1326.008

> BIC(fres)

[1] -1316.19

> vcov(fres)

theta1 theta2

theta1 1.000450e+00 -1.385373e-08

theta2 -1.385373e-08 5.002214e-04

> confint(fres,level=0.95)

2.5 % 97.5 %

theta1 1.200315 5.121125

theta2 0.956389 1.044061

>

> ## No test:

> ##### Example 2:

>

>

> ## Nonlinear mean reversion (Ait-Sahalia) modele

> ## dX(t) = (theta1 + theta2*x + theta3*x^2) * dt + theta4 * x^theta5 * dW(t)

> ## Simulation of the process X(t)

> set.seed(1234)

>

> f <- expression(1 - 11*x + 2*x^2)

> g <- expression(x^0.5)

> res <- snssde1d(drift=f,diffusion=g,M=1,N=1000,Dt=0.001,x0=5)

> mydata1 <- res$X

>

> ## Estimation

> ## true param theta= c(1,-11,2,1,0.5)

> true <- c(1,-11,2,1,0.5)

> pmle <- eval(formals(fitsde.default)$pmle)

>

> fx <- expression(theta[1] + theta[2]*x + theta[3]*x^2)

> gx <- expression(theta[4]*x^theta[5])

>

> fres <- lapply(1:4, function(i) fitsde(mydata1,drift=fx,diffusion=gx,

+ pmle=pmle[i],start = list(theta1=1,theta2=1,theta3=1,theta4=1,

+ theta5=1),optim.method = "L-BFGS-B"))

> Coef <- data.frame(true,do.call("cbind",lapply(1:4,function(i) coef(fres[[i]]))))

> names(Coef) <- c("True",pmle)

> Summary <- data.frame(do.call("rbind",lapply(1:4,function(i) logLik(fres[[i]]))),

+ do.call("rbind",lapply(1:4,function(i) AIC(fres[[i]]))),

+ do.call("rbind",lapply(1:4,function(i) BIC(fres[[i]]))),

+ row.names=pmle)

> names(Summary) <- c("logLik","AIC","BIC")

> Coef

True euler kessler ozaki shoji

theta1 1.0 0.6873700 0.66607155 0.65115001 0.68374592

theta2 -11.0 -6.9947010 -6.86096214 -6.85205839 -6.92324706

theta3 2.0 0.1152499 0.06059366 0.06270915 0.07623474

theta4 1.0 1.0022594 1.00664000 1.00512419 1.00547899

theta5 0.5 0.5055101 0.50662118 0.50800957 0.50539687

> Summary

logLik AIC BIC

euler 2758.713 -5507.427 -5503.609

kessler 2758.610 -5507.219 -5503.402

ozaki 2758.528 -5507.056 -5503.239

shoji 2758.709 -5507.419 -5503.601

>

>

> ##### Example 3:

>

> ## dX(t) = (theta1*x*t+theta2*tan(x)) *dt + theta3*t *dW(t)

> ## Simulation of data

> set.seed(1234)

>

> f <- expression(2*x*t-tan(x))

> g <- expression(1.25*t)

> sim <- snssde1d(drift=f,diffusion=g,M=1,N=1000,Dt=0.001,x0=10)

> mydata2 <- sim$X

>

> ## Estimation

> ## true param theta= c(2,-1,1.25)

> true <- c(2,-1,1.25)

>

> fx <- expression(theta[1]*x*t+theta[2]*tan(x))

> gx <- expression(theta[3]*t)

>

> fres <- lapply(1:4, function(i) fitsde(mydata2,drift=fx,diffusion=gx,

+ pmle=pmle[i],start = list(theta1=1,theta2=1,theta3=1),

+ optim.method = "L-BFGS-B"))

Warning messages:

1: In log(1 + (A(t0, x0, theta)/(x0 * Ax(t0, x0, theta))) * (exp(Ax(t0, :

NaNs produced

2: In log(1 + (A(t0, x0, theta)/(x0 * Ax(t0, x0, theta))) * (exp(Ax(t0, :

NaNs produced

3: In log(1 + (A(t0, x0, theta)/(x0 * Ax(t0, x0, theta))) * (exp(Ax(t0, :

NaNs produced

4: In log(1 + (A(t0, x0, theta)/(x0 * Ax(t0, x0, theta))) * (exp(Ax(t0, :

NaNs produced

5: In log(1 + (A(t0, x0, theta)/(x0 * Ax(t0, x0, theta))) * (exp(Ax(t0, :

NaNs produced

6: In log(1 + (A(t0, x0, theta)/(x0 * Ax(t0, x0, theta))) * (exp(Ax(t0, :

NaNs produced

7: In log(1 + (A(t0, x0, theta)/(x0 * Ax(t0, x0, theta))) * (exp(Ax(t0, :

NaNs produced

> Coef <- data.frame(true,do.call("cbind",lapply(1:4,function(i) coef(fres[[i]]))))

> names(Coef) <- c("True",pmle)

> Summary <- data.frame(do.call("rbind",lapply(1:4,function(i) logLik(fres[[i]]))),

+ do.call("rbind",lapply(1:4,function(i) AIC(fres[[i]]))),

+ do.call("rbind",lapply(1:4,function(i) BIC(fres[[i]]))),

+ row.names=pmle)

> names(Summary) <- c("logLik","AIC","BIC")

> Coef

True euler kessler ozaki shoji

theta1 2.00 1.914026 0.95314362 1.9115444 1.9085177

theta2 -1.00 -0.990799 0.01136956 -0.9897514 -0.9612274

theta3 1.25 1.255735 1.64358954 1.2834434 1.3245215

> Summary

logLik AIC BIC

euler 2801.036 -5596.073 -5588.255

kessler 2584.406 -5162.812 -5154.994

ozaki 2778.965 -5551.929 -5544.112

shoji 2793.992 -5581.984 -5574.166

> ## End(No test)

>

> ##### Example 4:

>

> ## Application to real data

> ## CKLS modele vs CIR modele

> ## CKLS (mod1): dX(t) = (theta1+theta2* X(t))* dt + theta3 * X(t)^theta4 * dW(t)

> ## CIR (mod2): dX(t) = (theta1+theta2* X(t))* dt + theta3 * sqrt(X(t)) * dW(t)

> set.seed(1234)

>

> data(Irates)

> rates <- Irates[,"r1"]

> rates <- window(rates, start=1964.471, end=1989.333)

>

> fx1 <- expression(theta[1]+theta[2]*x)

> gx1 <- expression(theta[3]*x^theta[4])

> gx2 <- expression(theta[3]*sqrt(x))

>

> fitmod1 <- fitsde(rates,drift=fx1,diffusion=gx1,pmle="euler",start = list(theta1=1,theta2=1,

+ theta3=1,theta4=1),optim.method = "L-BFGS-B")

> fitmod2 <- fitsde(rates,drift=fx1,diffusion=gx2,pmle="euler",start = list(theta1=1,theta2=1,

+ theta3=1),optim.method = "L-BFGS-B")

> summary(fitmod1)

Pseudo maximum likelihood estimation

Method: Euler

Call:

fitsde(data = rates, drift = fx1, diffusion = gx1, pmle = "euler",

start = list(theta1 = 1, theta2 = 1, theta3 = 1, theta4 = 1),

optim.method = "L-BFGS-B")

Coefficients:

Estimate Std. Error

theta1 2.0769516 0.98838467

theta2 -0.2631871 0.19544290

theta3 0.1302158 0.02523105

theta4 1.4513173 0.10323740

-2 log L: 475.7572

> summary(fitmod2)

Pseudo maximum likelihood estimation

Method: Euler

Call:

fitsde(data = rates, drift = fx1, diffusion = gx2, pmle = "euler",

start = list(theta1 = 1, theta2 = 1, theta3 = 1), optim.method = "L-BFGS-B")

Coefficients:

Estimate Std. Error

theta1 2.6387593 1.18754725

theta2 -0.3606083 0.18896205

theta3 0.8650745 0.03549428

-2 log L: 563.7025

> coef(fitmod1)

theta1 theta2 theta3 theta4

2.0769516 -0.2631871 0.1302158 1.4513173

> coef(fitmod2)

theta1 theta2 theta3

2.6387593 -0.3606083 0.8650745

> confint(fitmod1,parm=c('theta2','theta3'))

2.5 % 97.5 %

theta2 -0.64624812 0.1198740

theta3 0.08076388 0.1796678

> confint(fitmod2,parm=c('theta2','theta3'))

2.5 % 97.5 %

theta2 -0.7309671 0.009750478

theta3 0.7955070 0.934642013

> AIC(fitmod1)

[1] 483.7572

> AIC(fitmod2)

[1] 569.7025

> ## No test:

> ## Display

> ## CKLS Modele

> op <- par(mfrow = c(1, 2))

> theta <- coef(fitmod1)

> N <- length(rates)

> res <- snssde1d(drift=fx1,diffusion=gx1,M=200,t0=time(rates)[1],T=time(rates)[N],

+ Dt=deltat(rates),x0=rates[1],N)

> plot(res,plot.type="single",ylim=c(0,40))

> lines(rates,col=2,lwd=2)

> legend("topleft",c("real data","CKLS modele"),inset = .01,col=c(2,1),lwd=2,cex=0.8)

>

> ## CIR Modele

> theta <- coef(fitmod2)

> res <- snssde1d(drift=fx1,diffusion=gx2,M=200,t0=time(rates)[1],T=time(rates)[N],

+ Dt=deltat(rates),x0=rates[1],N)

> plot(res,plot.type="single",ylim=c(0,40))

> lines(rates,col=2,lwd=2)

> legend("topleft",c("real data","CIR modele"),inset = .01,col=c(2,1),lwd=2,cex=0.8)

> par(op)

> ## End(No test)

>

>

>

>

>

> dev.off()

null device

1

>

|