Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

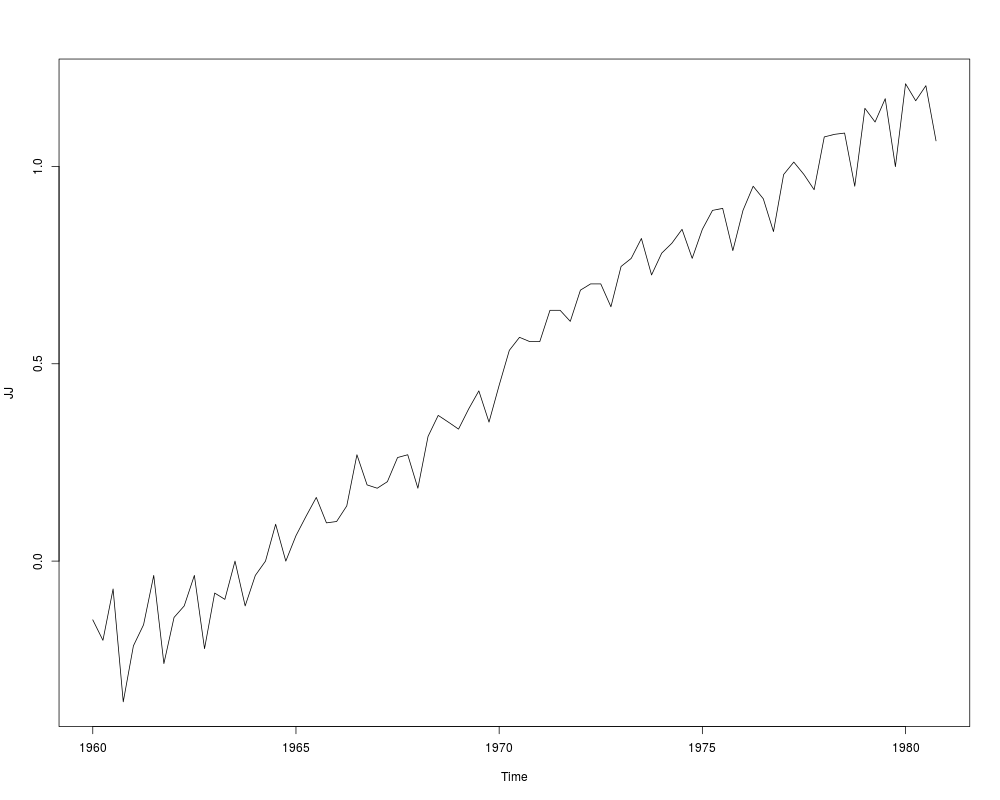

Quarterly Earnings per Johnson & Johnson ShareDescriptionQuarterly earnings (dollars) per Johnson & Johnson share 1960–80. UsageJohnsonJohnson FormatA quarterly time series SourceShumway, R. H. and Stoffer, D. S. (2000) Time Series Analysis and its Applications. Second Edition. Springer. Example 1.1. Examples

require(stats); require(graphics)

JJ <- log10(JohnsonJohnson)

plot(JJ)

## This example gives a possible-non-convergence warning on some

## platforms, but does seem to converge on x86 Linux and Windows.

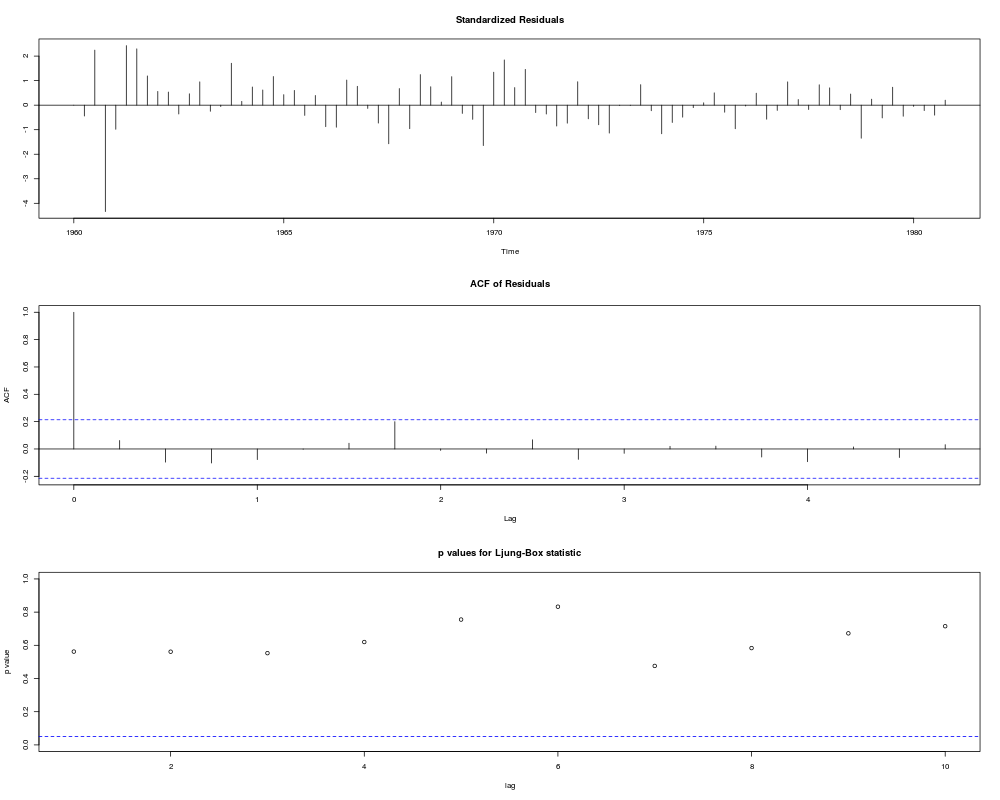

(fit <- StructTS(JJ, type = "BSM"))

tsdiag(fit)

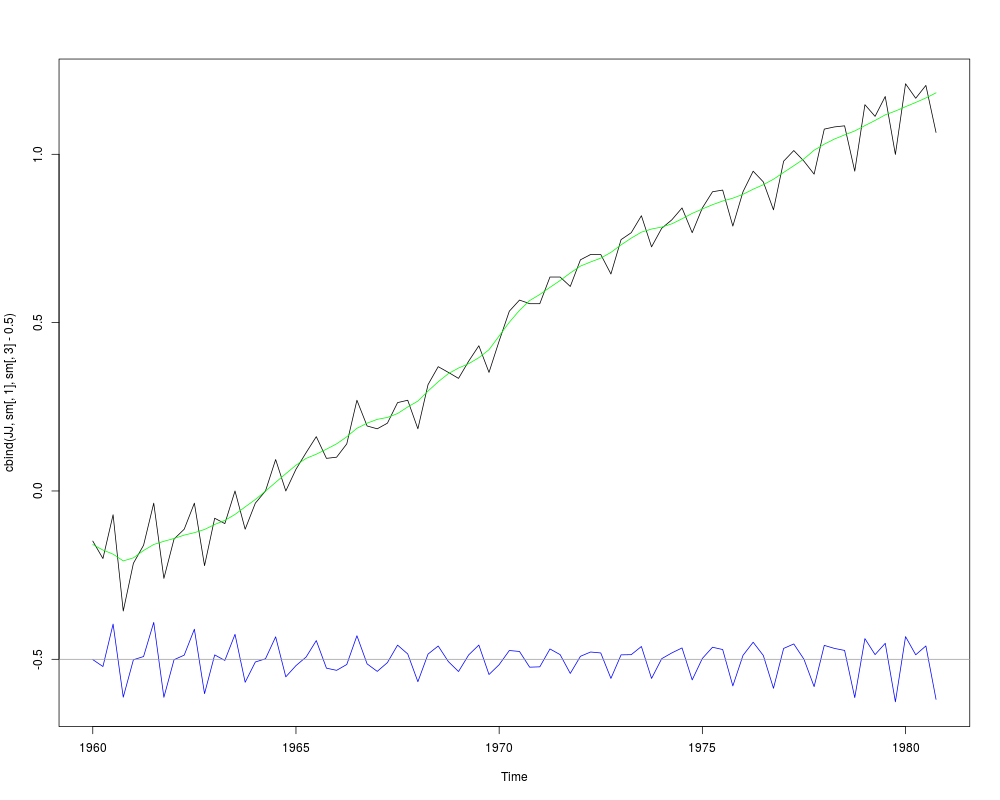

sm <- tsSmooth(fit)

plot(cbind(JJ, sm[, 1], sm[, 3]-0.5), plot.type = "single",

col = c("black", "green", "blue"))

abline(h = -0.5, col = "grey60")

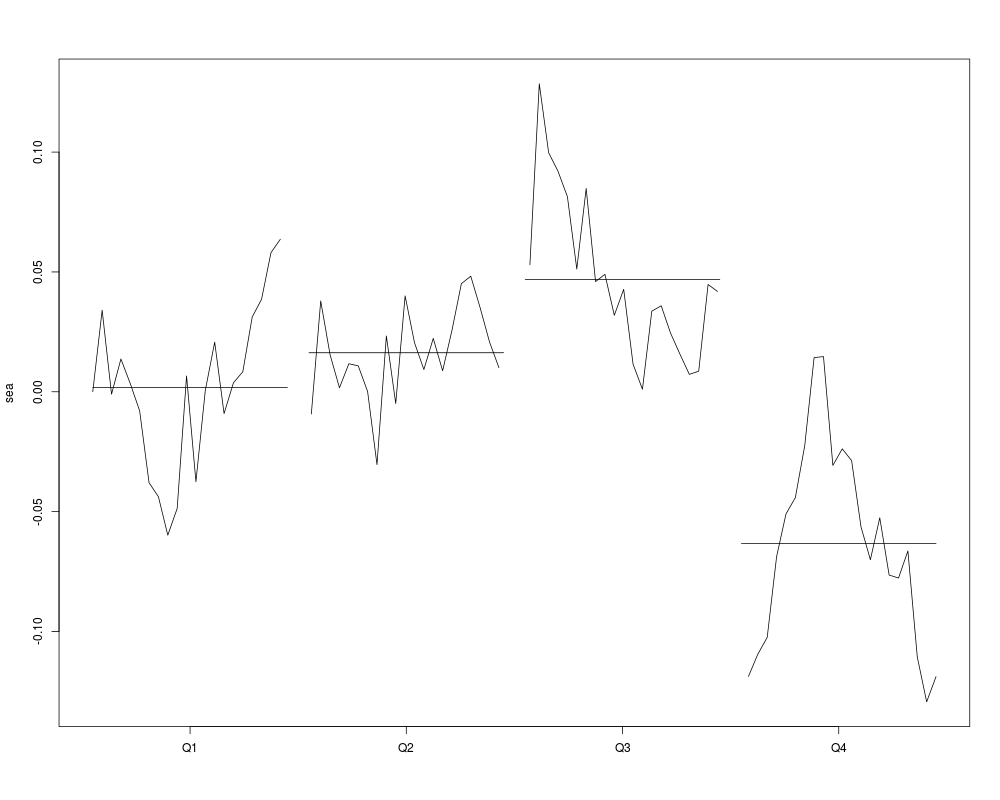

monthplot(fit)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(datasets)

> png(filename="/home/ddbj/snapshot/RGM3/R_rel/result/datasets/JohnsonJohnson.Rd_%03d_medium.png", width=480, height=480)

> ### Name: JohnsonJohnson

> ### Title: Quarterly Earnings per Johnson & Johnson Share

> ### Aliases: JohnsonJohnson

> ### Keywords: datasets

>

> ### ** Examples

> ## No test:

> require(stats); require(graphics)

> JJ <- log10(JohnsonJohnson)

> plot(JJ)

> ## This example gives a possible-non-convergence warning on some

> ## platforms, but does seem to converge on x86 Linux and Windows.

> (fit <- StructTS(JJ, type = "BSM"))

Call:

StructTS(x = JJ, type = "BSM")

Variances:

level slope seas epsilon

1.948e-04 6.548e-06 4.138e-04 2.647e-04

> tsdiag(fit)

> sm <- tsSmooth(fit)

> plot(cbind(JJ, sm[, 1], sm[, 3]-0.5), plot.type = "single",

+ col = c("black", "green", "blue"))

> abline(h = -0.5, col = "grey60")

>

> monthplot(fit)

> ## End(No test)

>

>

>

>

> dev.off()

null device

1

>

|

Created & Maintained by Osamu Ogasawara (osamu.ogasawara@gmail.com) and