R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(AutoModel)

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/AutoModel/model_output.Rd_%03d_medium.png", width=480, height=480)

> ### Name: model_output

> ### Title: Multiple Regression Output

> ### Aliases: model_output

>

> ### ** Examples

>

> freeny_model_formulas <- create_formula_objects("y",

+ c("lag.quarterly.revenue"), c("price.index"))

> freeny_models <- create_model_objects(freeny_model_formulas,

+ dataset = freeny)

> freeny_model <- freeny_models[[length(freeny_models)]]

> checks <- assumptions_check(freeny_model)

> model_output(freeny_models, freeny, checks, freeny_model_formulas,

+ outliers = "significant")

REGRESSION OUTPUT

Durbin-Watson = 2.357 p value = 0.797

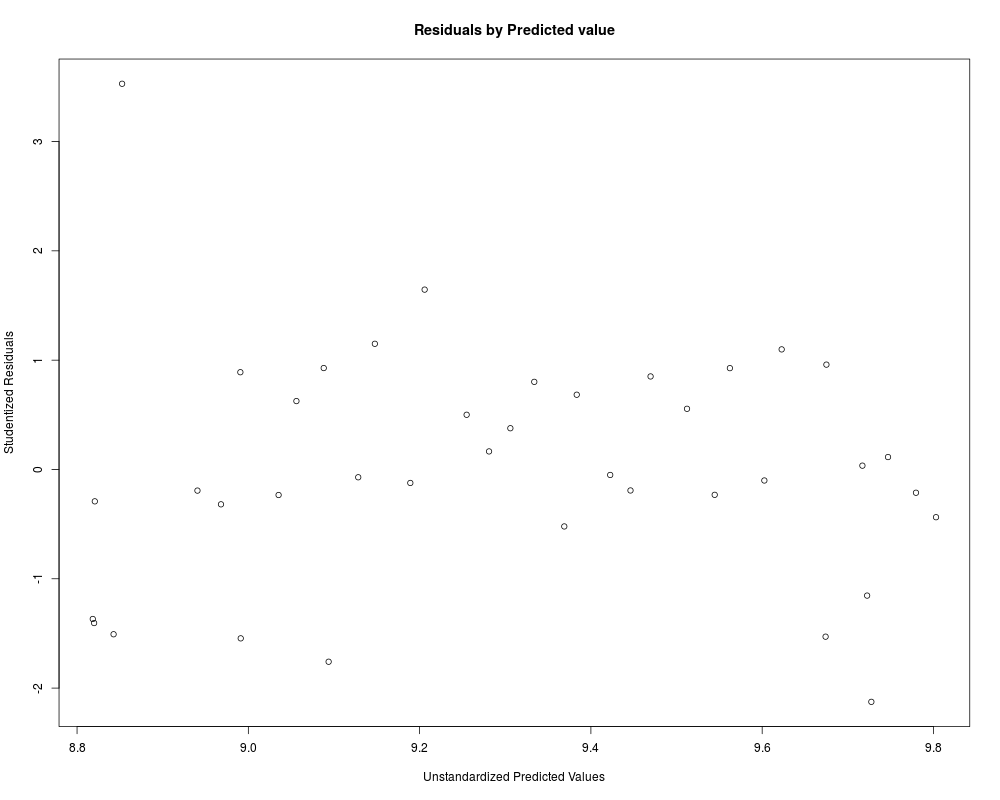

Partial Regression plots (all relationships should be linear):

Plot of studentized residuals: uniform distibution across predicted values requiredCorrelation Matrix for model (correlation >.70 indicates severe multicollinearity)

y lag.quarterly.revenue price.index

y 1.0000 0.9978 -0.9895

lag.quarterly.revenue 0.9978 1.0000 -0.9894

price.index -0.9895 -0.9894 1.0000

Variance inflation factor (<10 desired):

lag.quarterly.revenue price.index

47.5 47.5

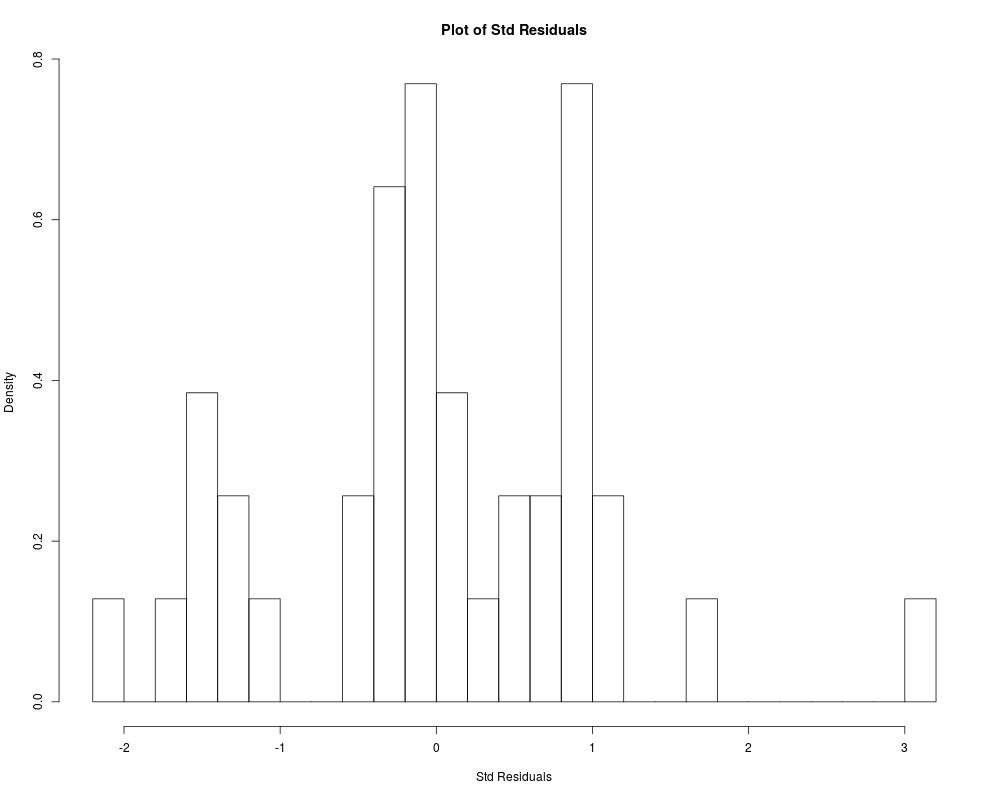

Standardized Residuals (observations > 3.00 problematic):

1963.25

3.073

Cook's distance (values >.2 problematic):

1963.25

1.169

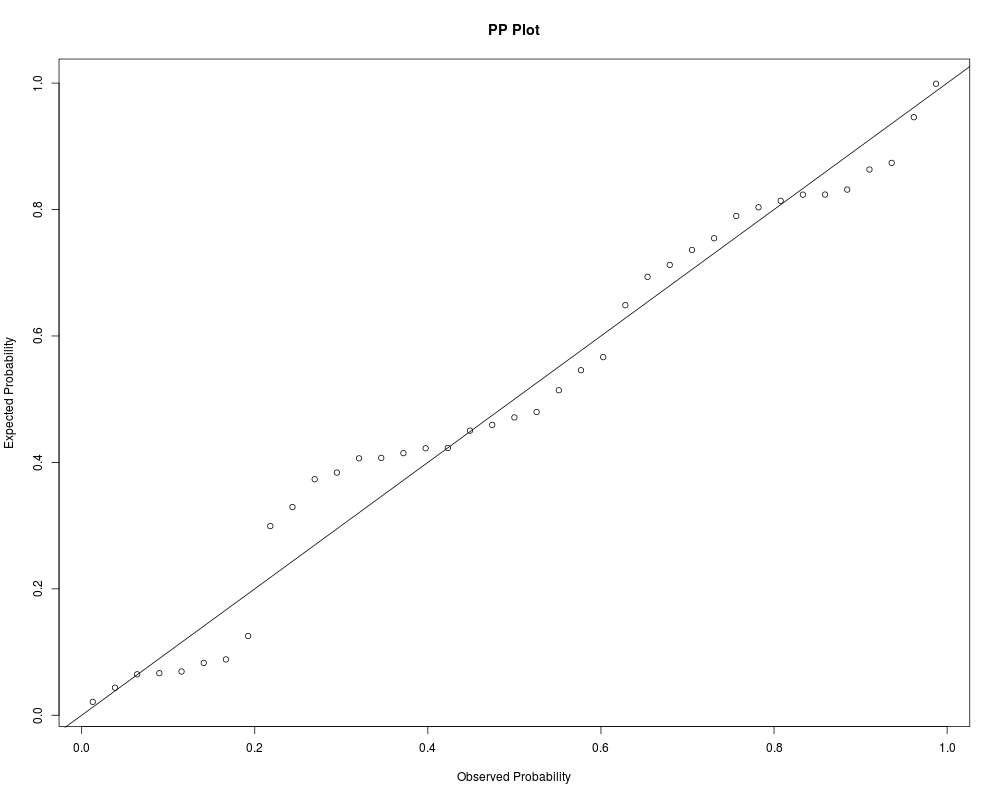

Normality of standardized model residuals: Shapiro-Wilk (p-value): 0.1296

Model change statistics

R R^2 Adj R^2 SE Est. Delta R^2 F Change df1 df2 p Fch Sig

Model 1 0.9978 0.9956 0.9955 0.0212 0.9956 8360.3793 1 37 0 ***

Model 2 0.9979 0.9958 0.9956 0.0209 0.0002 2.1304 1 36 0.1531

Model 1 : y ~ lag.quarterly.revenue

Model 2 : y ~ lag.quarterly.revenue + price.index

Model Coefficients

Model term estimate std.error statistic p.value sig

Model 1 (Intercept) 0.04169 0.10138 0.4112 0.6833

Model 1 lag.quarterly.revenue 0.99827 0.01092 91.4351 0.0000 ***

Model 2 (Intercept) 2.18577 1.47236 1.4845 0.1464

Model 2 lag.quarterly.revenue 0.89122 0.07412 12.0240 0.0000 ***

Model 2 price.index -0.25592 0.17534 -1.4596 0.1531

>

>

>

>

>

> dev.off()

null device

1

>

.

.