A character vector, with names of variables. The first block of

independent variables.

...

A character vector, with names of variables. Subsequent blocks of

independent variables.

dataset

A data frame containing variables refered to in

formulas, passed to data argument of lm

type

Family argument to pass to glm. Specify "binomial" for

binary logistic regression models.

assumptions.check

Boolean, if TRUE, then assumption checks are run and

output is produced. If FALSE, only model summary and coefficient tables are

produced.

outliers.check

Determines how many observations to display for

outliers check. Default is significant observations. "All" shows all

residual and Cook's D values.

transform.outcome

A boolean. If TRUE, a variable transformation of the

outcome is substituted in the final model if outcome is non-normal. NOT

IMPLEMENTED YET.

Details

Calls other functions to generate model objects and test them, given

specified model parameters and other options. Formatted output is produced

via model_output

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(AutoModel)

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/AutoModel/run_model.Rd_%03d_medium.png", width=480, height=480)

> ### Name: run_model

> ### Title: Automated Multiple Regression Modelling

> ### Aliases: run_model

>

> ### ** Examples

>

> run_model("y", c("lag.quarterly.revenue"), c("price.index", "income.level"),

+ dataset=freeny)

REGRESSION OUTPUT

Durbin-Watson = 2.11 p value = 0.4729

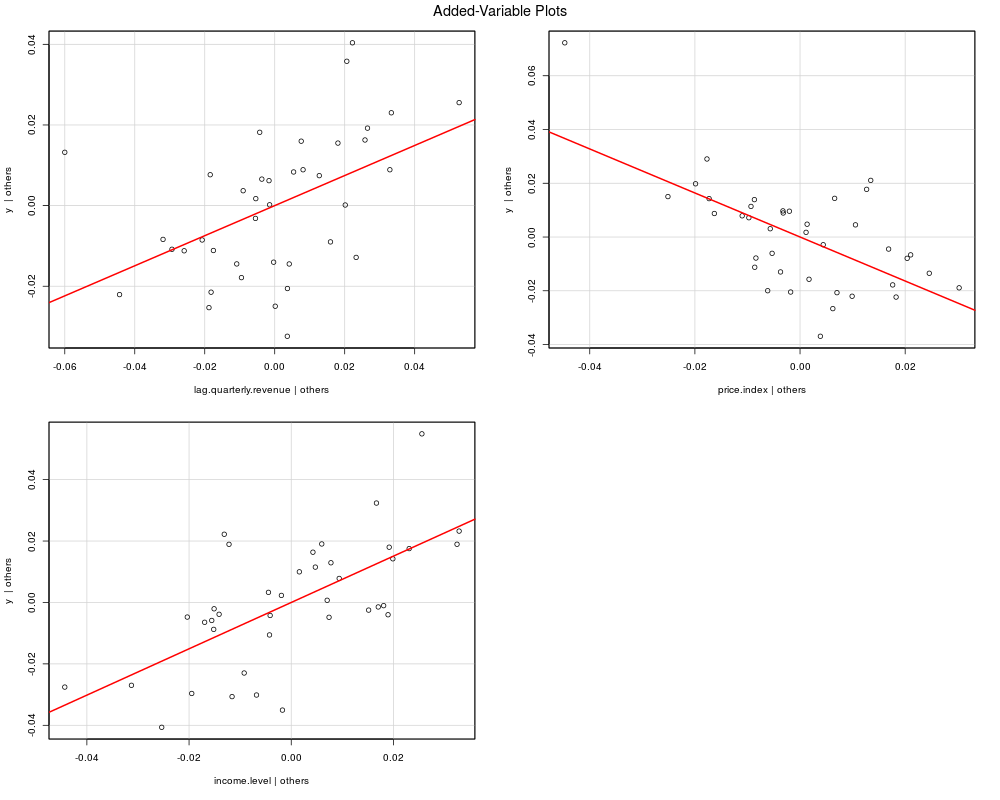

Partial Regression plots (all relationships should be linear):

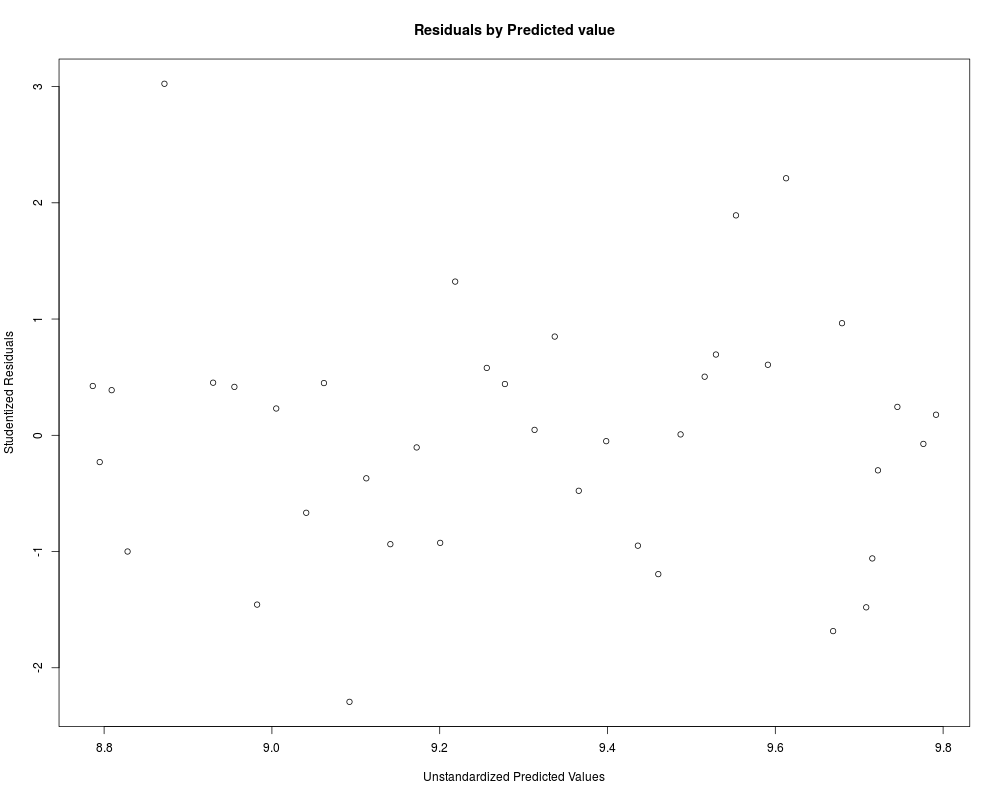

Plot of studentized residuals: uniform distibution across predicted values requiredCorrelation Matrix for model (correlation >.70 indicates severe multicollinearity)

y lag.quarterly.revenue price.index income.level

y 1.0000 0.9978 -0.9895 0.9839

lag.quarterly.revenue 0.9978 1.0000 -0.9894 0.9817

price.index -0.9895 -0.9894 1.0000 -0.9539

income.level 0.9839 0.9817 -0.9539 1.0000

Variance inflation factor (<10 desired):

lag.quarterly.revenue price.index income.level

194.85 78.58 45.52

Standardized Residuals (observations > 3.00 problematic):

No significant outliers

Cook's distance (values >.2 problematic):

1963.25

0.8918

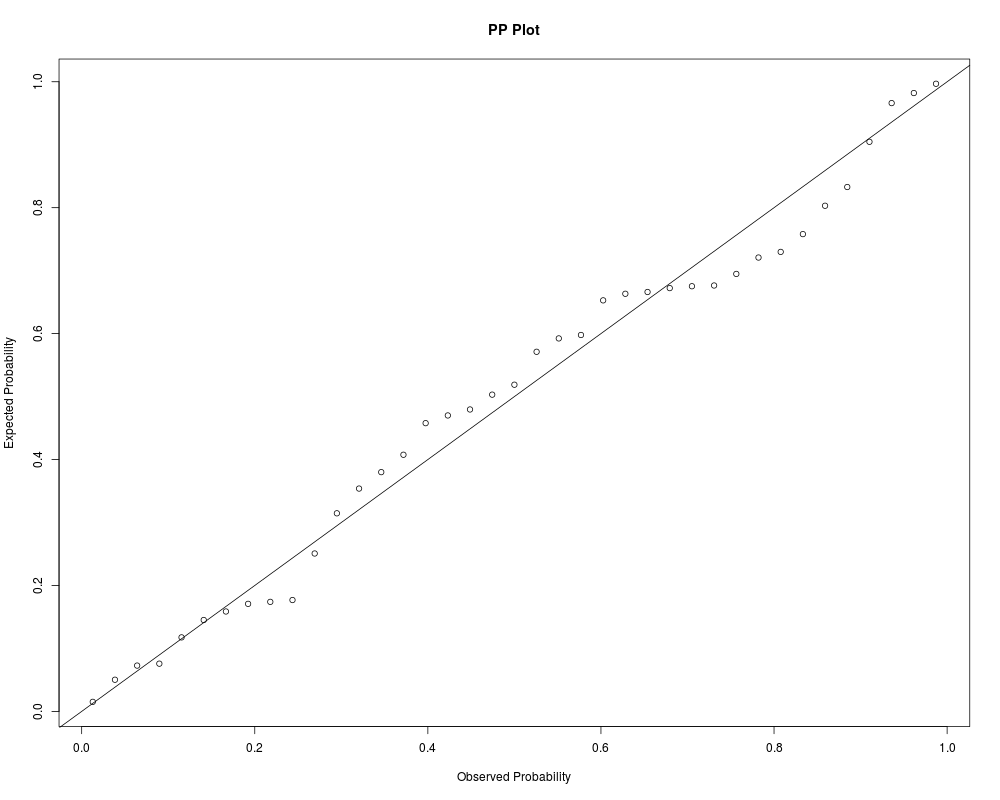

Normality of standardized model residuals: Shapiro-Wilk (p-value): 0.5586

Model change statistics

R R^2 Adj R^2 SE Est. Delta R^2 F Change df1 df2 p Fch Sig

Model 1 0.9978 0.9956 0.9955 0.0212 0.9956 8360.3793 1 37 0 ***

Model 2 0.9988 0.9977 0.9975 0.0159 0.0021 15.4599 2 35 0 ***

Model 1 : y ~ lag.quarterly.revenue

Model 2 : y ~ lag.quarterly.revenue + price.index + income.level

Model Coefficients

Model term estimate std.error statistic p.value sig

Model 1 (Intercept) 0.04169 0.10138 0.4112 0.6833

Model 1 lag.quarterly.revenue 0.99827 0.01092 91.4351 0.0000 ***

Model 2 (Intercept) 4.97077 1.24046 4.0072 0.0003 ***

Model 2 lag.quarterly.revenue 0.37305 0.11418 3.2673 0.0024 **

Model 2 price.index -0.81887 0.17152 -4.7742 0.0000 ***

Model 2 income.level 0.75435 0.14454 5.2189 0.0000 ***

>

>

>

>

>

> dev.off()

null device

1

>

.

.