Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

The Gamma-Gamma DistributionDescriptionDensity and random generation for the Gamma-Gamma distribution with parameters

Usagedggamma(x, shape1, rate1, shape2) rggamma(n, shape1, rate1, shape2) Arguments

DetailsA Gamma-Gamma distribution with parameters f(x) = [(r^a)/(Gamma(a))][Gamma(a+b)/Gamma(b)] [x^(b-1)/(r+x)^(a+b)] for x > 0 where a,r > 0 and b = 1,2,…. The distribution is generated using the following scheme:

Then, X follows a Gamma-Gamma distribution. Value

ReferencesBernardo JM, Smith AFM. (1994) Bayesian Theory. Wiley, New York. See Also

Examples

############################################################

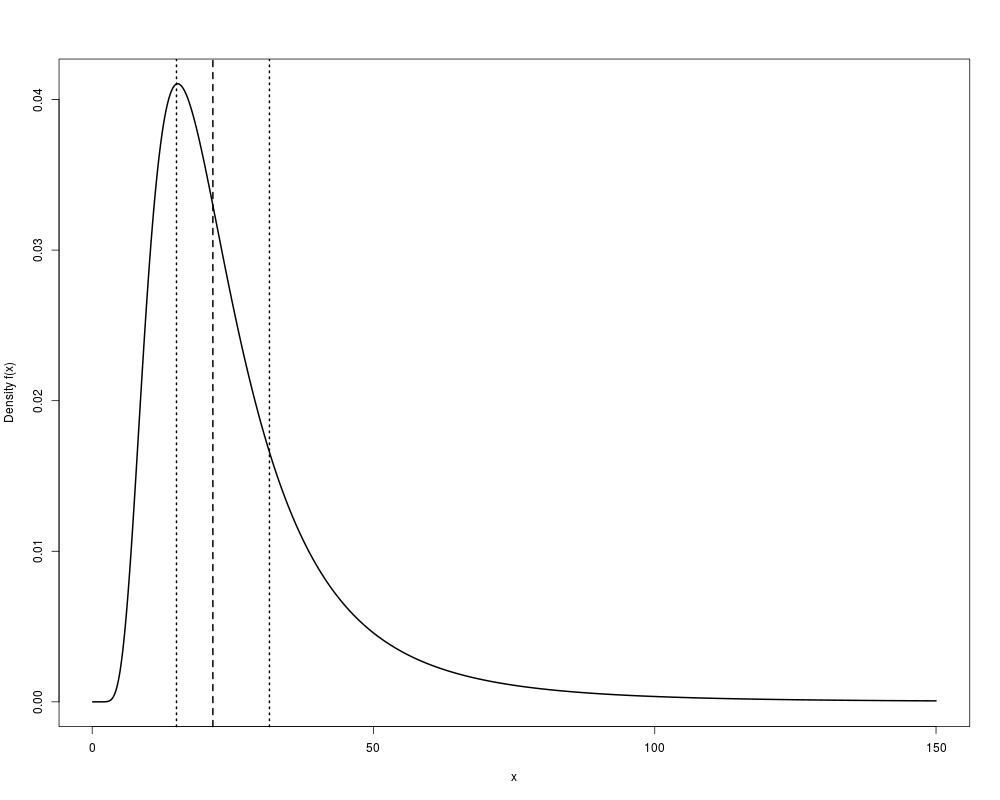

# Construct a plot of the density function with median and

# quantiles marked.

# define parameters

shape1 <- 4

rate1 <- 4

shape2 <- 20

# construct density plot

x <- seq(0.1,150,0.1)

plot(dggamma(x,shape1,rate1,shape2)~x,

type="l",lwd=2,main="",xlab="x",ylab="Density f(x)")

# determine median and quantiles

set.seed(123)

X <- rggamma(5000,shape1,rate1,shape2)

quants <- quantile(X,prob=c(0.25,0.5,0.75))

# add quantities to plot

abline(v=quants,lty=c(3,2,3),lwd=2)

############################################################

# Consider the following set-up:

# Let x ~ N(theta,sigma2), sigma2 is unknown variance.

# Consider a prior on theta and sigma2 defined by

# theta|sigma2 ~ N(mu,(r*sigma)^2)

# sigma2 ~ InverseGamma(a/2,b/2), (b/2) = rate.

#

# We want to generate random variables from the marginal

# (prior predictive) distribution of the sufficient

# statistic T = (xbar,s2) where the sample size n = 25.

# define parameters

a <- 4

b <- 4

mu <- 1

r <- 3

n <- 25

# generate random variables from Gamma-Gamma

set.seed(123)

shape1 <- a/2

rate1 <- b

shape2 <- 0.5*(n-1)

Y <- rggamma(5000,shape1,rate1,shape2)

# generate variables from a non-central t given Y

df <- n+a-1

scale <- (Y+b)*(1/n + r^2)/(n+a-1)

X <- rt(5000,df=df)*sqrt(scale) + mu

# the pair (X,Y) comes from the correct marginal density

# mean of xbar and s2, and xbar*s2

mean(X)

mean(Y)

mean(X*Y)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(BAEssd)

Loading required package: mvtnorm

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/BAEssd/GammaGamma.Rd_%03d_medium.png", width=480, height=480)

> ### Name: GammaGamma

> ### Title: The Gamma-Gamma Distribution

> ### Aliases: GammaGamma dggamma rggamma

>

> ### ** Examples

>

> ############################################################

> # Construct a plot of the density function with median and

> # quantiles marked.

>

> # define parameters

> shape1 <- 4

> rate1 <- 4

> shape2 <- 20

>

> # construct density plot

> x <- seq(0.1,150,0.1)

> plot(dggamma(x,shape1,rate1,shape2)~x,

+ type="l",lwd=2,main="",xlab="x",ylab="Density f(x)")

>

> # determine median and quantiles

> set.seed(123)

> X <- rggamma(5000,shape1,rate1,shape2)

> quants <- quantile(X,prob=c(0.25,0.5,0.75))

>

> # add quantities to plot

> abline(v=quants,lty=c(3,2,3),lwd=2)

>

>

> ############################################################

> # Consider the following set-up:

> # Let x ~ N(theta,sigma2), sigma2 is unknown variance.

> # Consider a prior on theta and sigma2 defined by

> # theta|sigma2 ~ N(mu,(r*sigma)^2)

> # sigma2 ~ InverseGamma(a/2,b/2), (b/2) = rate.

> #

> # We want to generate random variables from the marginal

> # (prior predictive) distribution of the sufficient

> # statistic T = (xbar,s2) where the sample size n = 25.

>

> # define parameters

> a <- 4

> b <- 4

> mu <- 1

> r <- 3

> n <- 25

>

>

> # generate random variables from Gamma-Gamma

> set.seed(123)

> shape1 <- a/2

> rate1 <- b

> shape2 <- 0.5*(n-1)

>

> Y <- rggamma(5000,shape1,rate1,shape2)

>

> # generate variables from a non-central t given Y

> df <- n+a-1

> scale <- (Y+b)*(1/n + r^2)/(n+a-1)

>

> X <- rt(5000,df=df)*sqrt(scale) + mu

>

> # the pair (X,Y) comes from the correct marginal density

>

> # mean of xbar and s2, and xbar*s2

> mean(X)

[1] 0.9701382

> mean(Y)

[1] 51.11077

> mean(X*Y)

[1] 9.203261

>

>

>

>

>

> dev.off()

null device

1

>

|