Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Make an object that inherits from class "manifest"DescriptionThis function is intended for users and sets up the left-hand side of the

factor analysis model and is a prerequisite for calling

Although it is possible to simply estimate and use the unbiased sample

covariance matrix, there are many other ways to estimate a covariance

that can be superior, particularly when the traditional maximum likelihood

discrepancy function is not chosen in the call to In technical terms, Usage## S4 method for signature 'missing,missing,list' make_manifest(covmat, n.obs = NA_integer_, shrink = FALSE) ## S4 method for signature 'missing,missing,hetcor' make_manifest(covmat, shrink = FALSE) ## S4 method for signature 'missing,missing,matrix' make_manifest(covmat, n.obs = NA_integer_, shrink = FALSE, sds = NULL) ## S4 method for signature 'missing,missing,CovMcd' make_manifest(covmat) # Use the methods above when only the covariance matrix is available # Use the methods below when the raw data are available (preferable) ## S4 method for signature 'data.frame,missing,missing' make_manifest(x, subset, shrink = FALSE, bootstrap = 0, how = "default", seed = 12345, wt = NULL, ...) ## S4 method for signature 'missing,data.frame,missing' make_manifest(data, subset, shrink = FALSE, bootstrap = 0, how = "default", seed = 12345, wt = NULL, ...) ## S4 method for signature 'missing,matrix,missing' make_manifest(data, subset, shrink = FALSE, bootstrap = 0, how = "default", seed = 12345, wt = NULL, ...) ## S4 method for signature 'matrix,missing,missing' make_manifest(x, subset, shrink = FALSE, bootstrap = 0, how = "default", seed = 12345, wt = NULL, ...) ## S4 method for signature 'formula,data.frame,missing' make_manifest(x, data, subset, shrink = FALSE, na.action = "na.pass", bootstrap = 0, how = "default", seed = 12345, wt = NULL, ...) Arguments

DetailsThe rules governing the calculation of the sample covariance matrix are as follows and

primarily depend on whether any of the manifest variables are ordered factors. First,

consider the case where all manifest variables are numeric. If any of these manifest

variables contain missing values, then the covariance matrix is estimated via maximum

likelihood under multivariate normality assumptions but requires the suggested mvnmle

package. Otherwise, the Next, consider the case where at least one manifest variable is an ordered factor. If

In general, bootstrapping is good for estimating the uncertainty of the estimated sample covariances and this uncertainty estimate is needed for the ADF discrepancy function and its special cases. In some cases, bootstrapping is the only way to obtain such an uncertainty estimate. ValueAn object that inherits from Author(s)Ben Goodrich ReferencesDey, D. K. and Srinivasan K. (1985) Estimation of a covariance matrix under Stein's loss. The Annals of Statistics, 13, 1581–1591. Pison, G., Rousseeuw, P.J., Filzmoser, P. and Croux, C. (2003) Robust factor analysis. Journal of Multivariate Analysis, 84, 145–172. See Also

Examplesman <- make_manifest(covmat = Harman23.cor) show(man) # some basic info if(require(nFactors)) screeplot(man) # advanced Scree plot cormat(man) # sample correlation matrix Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(FAiR)

Loading required package: rgenoud

## rgenoud (Version 5.7-12.4, Build Date: 2015-07-19)

## See http://sekhon.berkeley.edu/rgenoud for additional documentation.

## Please cite software as:

## Walter Mebane, Jr. and Jasjeet S. Sekhon. 2011.

## ``Genetic Optimization Using Derivatives: The rgenoud package for R.''

## Journal of Statistical Software, 42(11): 1-26.

##

Loading required package: gWidgetsRGtk2

Loading required package: RGtk2

Loading required package: gWidgets

Loading required package: cairoDevice

Loading required package: stats4

Loading required package: rrcov

Loading required package: robustbase

Scalable Robust Estimators with High Breakdown Point (version 1.3-11)

Loading required package: Matrix

## FAiR Version 0.4-15 Build Date: 2014-02-08

## See http://wiki.r-project.org/rwiki/doku.php?id=packages:cran:fair for more info

FAiR Copyright (C) 2008 -- 2012 Benjamin King Goodrich

This program comes with ABSOLUTELY NO WARRANTY.

This is free software, and you are welcome to redistribute it

under certain conditions, namely those specified in the LICENSE file

in the root directory of the source code.

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/FAiR/01make_manifest.Rd_%03d_medium.png", width=480, height=480)

> ### Name: make_manifest

> ### Title: Make an object that inherits from class "manifest"

> ### Aliases: make_manifest make_manifest-methods

> ### make_manifest,missing,missing,list-method

> ### make_manifest,missing,missing,hetcor-method

> ### make_manifest,missing,missing,matrix-method

> ### make_manifest,missing,missing,CovMcd-method

> ### make_manifest,data.frame,missing,missing-method

> ### make_manifest,missing,data.frame,missing-method

> ### make_manifest,missing,matrix,missing-method

> ### make_manifest,matrix,missing,missing-method

> ### make_manifest,formula,data.frame,missing-method

> ### Keywords: multivariate methods

>

> ### ** Examples

>

> man <- make_manifest(covmat = Harman23.cor)

Warning message:

In FAiR_make_manifest_list(covmat, shrink) :

it is strongly preferable to pass the raw data to make_manifest()

> show(man) # some basic info

Number of observations: 305

Number of manifest variables: 8

Proportion of positive correlations: 1

p-value for null hypothesis that manifest variables are uncorrelated: 0

p-value for null hypothesis that the anti-images are uncorrelated: 1.401625e-209

Kaiser-Meyer-Okin Measure of Sampling Adequacy: 0.8454609

Kaiser-Meyer-Okin Measure of Homogeneity of Each Manifest Variable

[,1]

height 0.8643147

arm.span 0.8162962

forearm 0.8576544

lower.leg 0.8866618

weight 0.7796144

bitro.diameter 0.8511215

chest.girth 0.8240441

chest.width 0.8984689

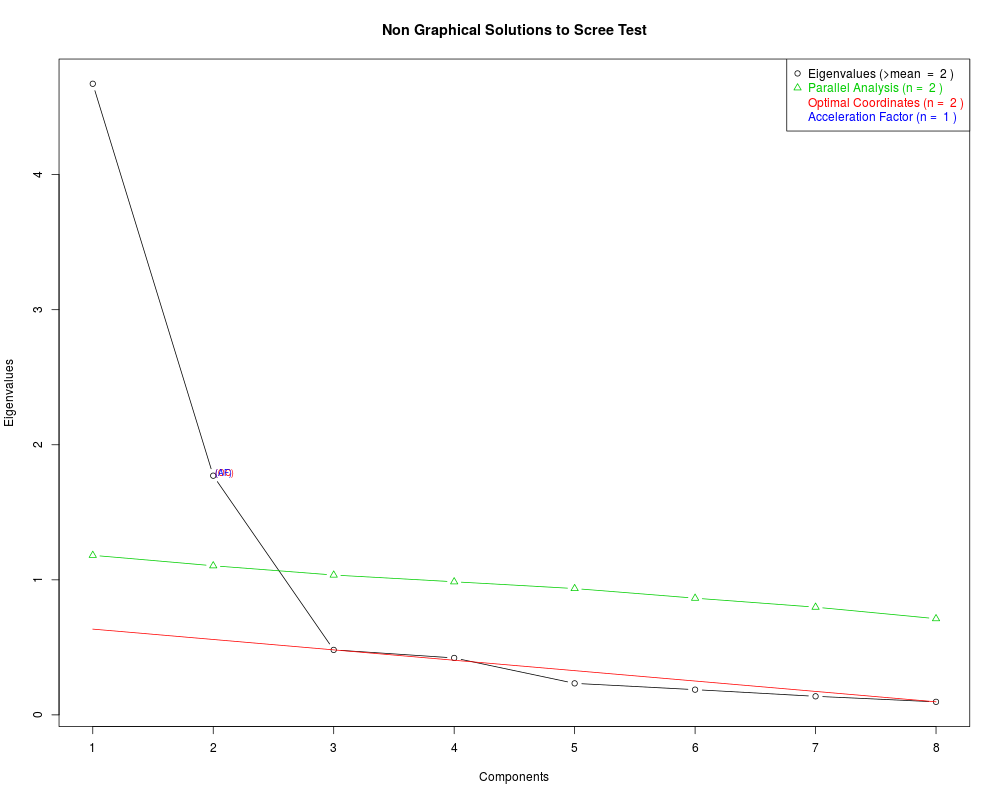

Eigenvalues of sample correlation matrix

[1] 4.67287960 1.77098284 0.48103549 0.42144078 0.23322126 0.18667352 0.13730387

[8] 0.09646264

> if(require(nFactors)) screeplot(man) # advanced Scree plot

Loading required package: nFactors

Loading required package: MASS

Loading required package: psych

Attaching package: 'psych'

The following object is masked from 'package:robustbase':

cushny

Loading required package: boot

Attaching package: 'boot'

The following object is masked from 'package:psych':

logit

The following object is masked from 'package:robustbase':

salinity

Loading required package: lattice

Attaching package: 'lattice'

The following object is masked from 'package:boot':

melanoma

Attaching package: 'nFactors'

The following object is masked from 'package:lattice':

parallel

> cormat(man) # sample correlation matrix

height arm.span forearm lower.leg weight bitro.diameter

height 1.000 0.846 0.805 0.859 0.473 0.398

arm.span 0.846 1.000 0.881 0.826 0.376 0.326

forearm 0.805 0.881 1.000 0.801 0.380 0.319

lower.leg 0.859 0.826 0.801 1.000 0.436 0.329

weight 0.473 0.376 0.380 0.436 1.000 0.762

bitro.diameter 0.398 0.326 0.319 0.329 0.762 1.000

chest.girth 0.301 0.277 0.237 0.327 0.730 0.583

chest.width 0.382 0.415 0.345 0.365 0.629 0.577

chest.girth chest.width

height 0.301 0.382

arm.span 0.277 0.415

forearm 0.237 0.345

lower.leg 0.327 0.365

weight 0.730 0.629

bitro.diameter 0.583 0.577

chest.girth 1.000 0.539

chest.width 0.539 1.000

>

>

>

>

>

> dev.off()

null device

1

>

|