Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Moments and Mode of the Generalized Hyperbolic DistributionDescriptionFunctions to calculate the mean, variance, skewness, kurtosis and mode of a specific generalized hyperbolic distribution. Usage

ghypMean(mu = 0, delta = 1, alpha = 1, beta = 0, lambda = 1,

param = c(mu, delta, alpha, beta, lambda))

ghypVar(mu = 0, delta = 1, alpha = 1, beta = 0, lambda = 1,

param = c(mu, delta, alpha, beta, lambda))

ghypSkew(mu = 0, delta = 1, alpha = 1, beta = 0, lambda = 1,

param = c(mu, delta, alpha, beta, lambda))

ghypKurt(mu = 0, delta = 1, alpha = 1, beta = 0, lambda = 1,

param = c(mu, delta, alpha, beta, lambda))

ghypMode(mu = 0, delta = 1, alpha = 1, beta = 0, lambda = 1,

param = c(mu, delta, alpha, beta, lambda))

Arguments

Value

The mode is found by a numerical optimisation using

The parameterization of the generalized hyperbolic distribution used

for these functions is the (alpha, beta) one. See

Author(s)David Scott d.scott@auckland.ac.nz, Thomas Tran ReferencesPrause, K. (1999) The generalized hyperbolic models: Estimation, financial derivatives and risk measurement. PhD Thesis, Mathematics Faculty, University of Freiburg. See Also

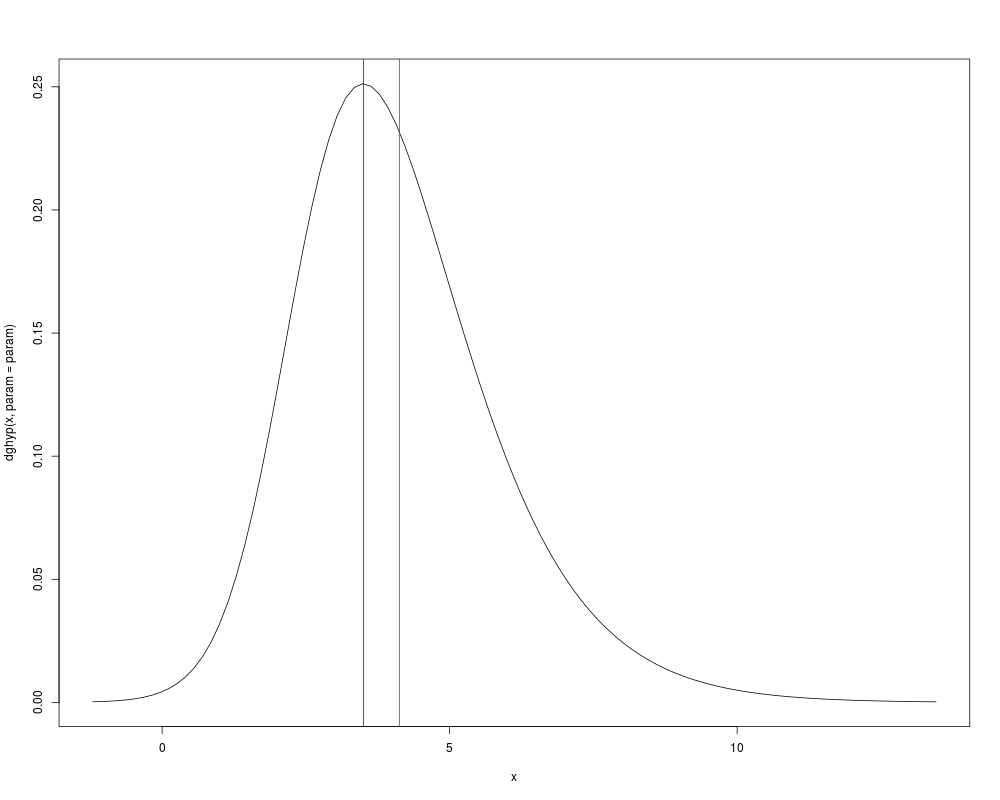

Examplesparam <- c(2, 2, 2, 1, 2) ghypMean(param = param) ghypVar(param = param) ghypSkew(param = param) ghypKurt(param = param) ghypMode(param = param) maxDens <- dghyp(ghypMode(param = param), param = param) ghypRange <- ghypCalcRange(param = param, tol = 10^(-3) * maxDens) curve(dghyp(x, param = param), ghypRange[1], ghypRange[2]) abline(v = ghypMode(param = param), col = "blue") abline(v = ghypMean(param = param), col = "red") Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(GeneralizedHyperbolic)

Loading required package: DistributionUtils

Loading required package: RUnit

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/GeneralizedHyperbolic/ghypMeanVarMode.Rd_%03d_medium.png", width=480, height=480)

> ### Name: Specific Generalized Hyperbolic Moments and Mode

> ### Title: Moments and Mode of the Generalized Hyperbolic Distribution

> ### Aliases: ghypMean ghypVar ghypSkew ghypKurt ghypMode

> ### Keywords: distribution

>

> ### ** Examples

>

> param <- c(2, 2, 2, 1, 2)

> ghypMean(param = param)

[1] 4.125532

> ghypVar(param = param)

[1] 3.192044

> ghypSkew(param = param)

[1] 0.7928604

> ghypKurt(param = param)

[1] 1.343511

> ghypMode(param = param)

[1] 3.499997

> maxDens <- dghyp(ghypMode(param = param), param = param)

> ghypRange <- ghypCalcRange(param = param, tol = 10^(-3) * maxDens)

> curve(dghyp(x, param = param), ghypRange[1], ghypRange[2])

> abline(v = ghypMode(param = param), col = "blue")

> abline(v = ghypMean(param = param), col = "red")

>

>

>

>

>

> dev.off()

null device

1

>

|