Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

GmedianCovDescriptionComputes recursively the Geometric median and the (geometric) median covariation matrix with fast averaged stochastic gradient algorithms. The estimation of the Geometric median is performed first and then the median covariation matrix is estimated, as well as its leading eigenvectors. The original recursive estimator of the median covariation matrix may not be a non negative matrix. A fast projected estimator onto the convex closed cone of the non negative matrices allows to get a non negative solution. UsageGmedianCov(X, init=NULL, nn=TRUE, scores=2, gamma=2, gc=2, alpha=0.75, nstart=1) Arguments

DetailsThe (fast) computation of the eigenvectors is performed by Value

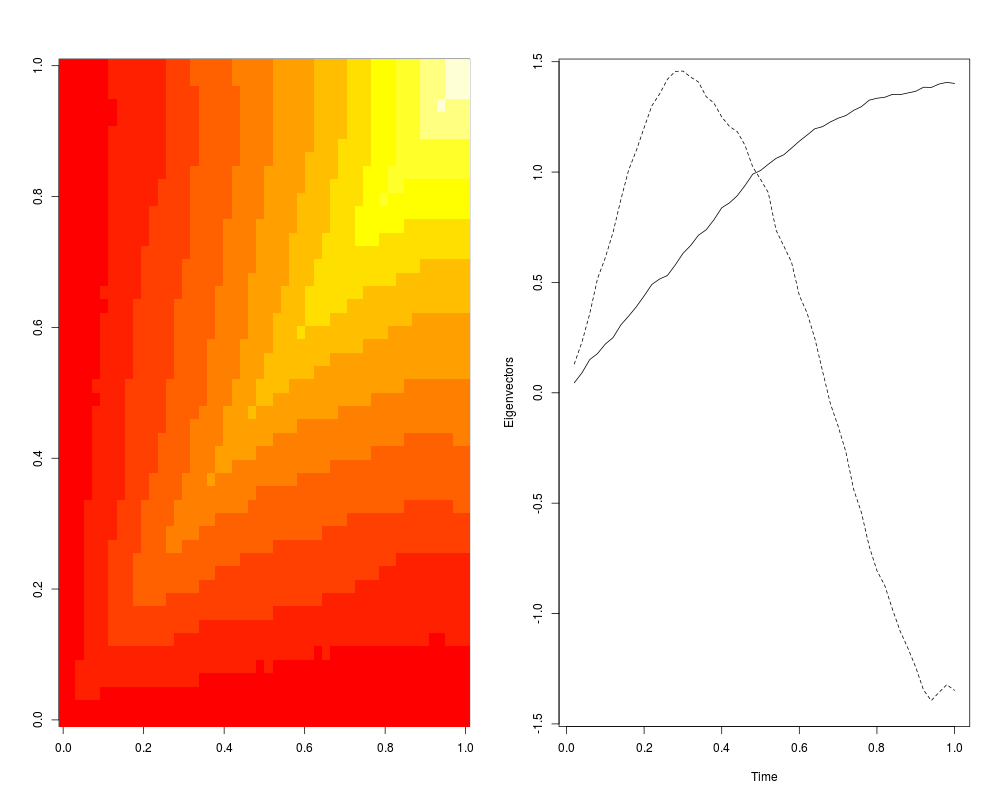

ReferencesCardot, H., Cenac, P. and Zitt, P-A. (2013). Efficient and fast estimation of the geometric median in Hilbert spaces with an averaged stochastic gradient algorithm. Bernoulli, 19, 18-43. Cardot, H. and Godichon-Baggioni, A. (2015). Fast Estimation of the Median Covariation Matrix with Application to Online Robust Principal Components Analysis. http://arxiv.org/abs/1504.02852 See AlsoSee also Examples## Simulated data - Brownian paths n <- 1e3 d <- 50 x <- matrix(rnorm(n*d,sd=1/sqrt(d)), n, d) x <- t(apply(x,1,cumsum)) ## Estimation median.est <- GmedianCov(x) par(mfrow=c(1,2)) image(median.est$covmedian) ## median covariation function plot(c(1:d)/d,median.est$vectors[,1]*sqrt(d),type="l",xlab="Time", ylab="Eigenvectors",ylim=c(-1.4,1.4)) lines(c(1:d)/d,median.est$vectors[,2]*sqrt(d),lty=2) Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(Gmedian)

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/Gmedian/GmedianCov.Rd_%03d_medium.png", width=480, height=480)

> ### Name: GmedianCov

> ### Title: GmedianCov

> ### Aliases: GmedianCov

> ### Keywords: Gmedian

>

> ### ** Examples

>

> ## Simulated data - Brownian paths

> n <- 1e3

> d <- 50

> x <- matrix(rnorm(n*d,sd=1/sqrt(d)), n, d)

> x <- t(apply(x,1,cumsum))

>

> ## Estimation

> median.est <- GmedianCov(x)

>

> par(mfrow=c(1,2))

> image(median.est$covmedian) ## median covariation function

> plot(c(1:d)/d,median.est$vectors[,1]*sqrt(d),type="l",xlab="Time",

+ ylab="Eigenvectors",ylim=c(-1.4,1.4))

> lines(c(1:d)/d,median.est$vectors[,2]*sqrt(d),lty=2)

>

>

>

>

>

> dev.off()

null device

1

>

|