Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

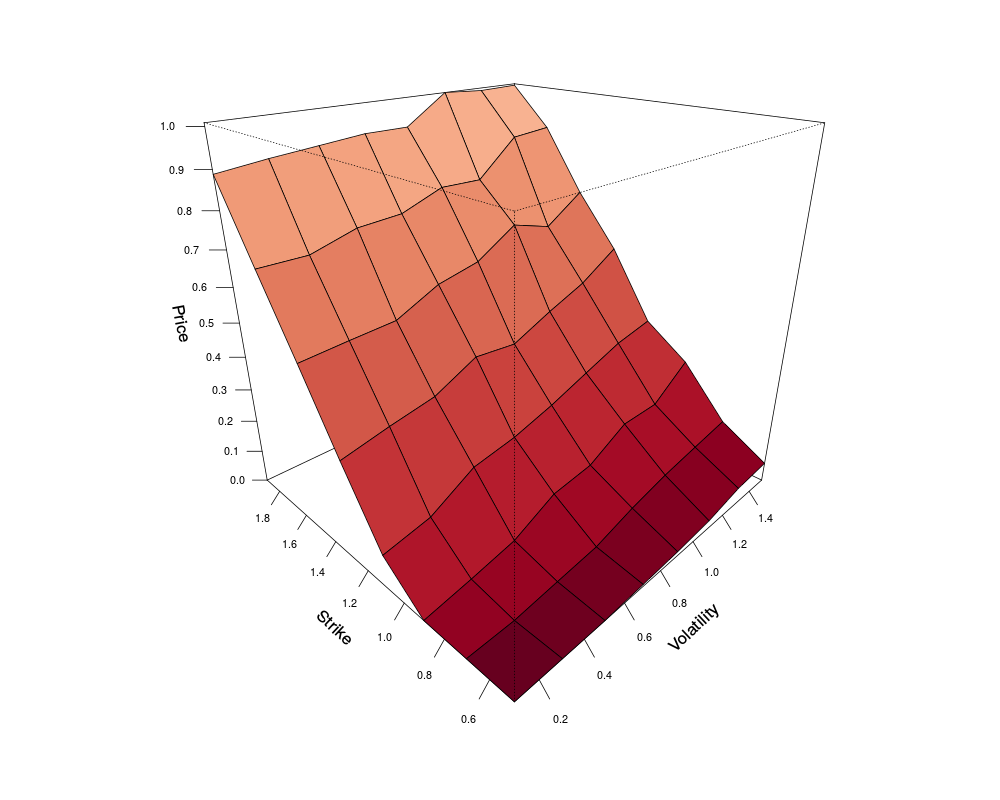

Deriving a table of Asian American put prices at different volatilities and strikesDescriptionThe function calculates the prices at different volatilities and strikes using the UsageAsianAmerPutLSMPriceSurf(Spot = 1, vols = (seq(0.1, 2, 0.1)), n = 1000, m = 365, strikes = (seq(0.5, 2.5, 0.1)), r = 0.06, dr = 0, mT = 1) Arguments

ValueThe function returns an object of the class PriceSurface that is a matrix of prices at different volatilities and strikes. Class-specific Author(s)Mikhail A. Beketov See AlsoFunctions: Examplessurface<-AsianAmerPutLSMPriceSurf(vols = (seq(0.1, 1.5, 0.2)), n=200, m=10, strikes = (seq(0.5, 1.9, 0.2))) summary(surface) plot(surface, color = divPalette(150, "RdBu")) Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(LSMonteCarlo)

Loading required package: mvtnorm

Loading required package: fBasics

Loading required package: timeDate

Loading required package: timeSeries

Rmetrics Package fBasics

Analysing Markets and calculating Basic Statistics

Copyright (C) 2005-2014 Rmetrics Association Zurich

Educational Software for Financial Engineering and Computational Science

Rmetrics is free software and comes with ABSOLUTELY NO WARRANTY.

https://www.rmetrics.org --- Mail to: info@rmetrics.org

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/LSMonteCarlo/AsianAmerPutLSMPriceSurf.Rd_%03d_medium.png", width=480, height=480)

> ### Name: AsianAmerPutLSMPriceSurf

> ### Title: Deriving a table of Asian American put prices at different

> ### volatilities and strikes

> ### Aliases: AsianAmerPutLSMPriceSurf

> ### Keywords: Monte Carlo Option pricing American put

>

> ### ** Examples

>

> surface<-AsianAmerPutLSMPriceSurf(vols = (seq(0.1, 1.5, 0.2)), n=200, m=10,

+ strikes = (seq(0.5, 1.9, 0.2)))

> summary(surface)

Volatility sequence:

0.1 0.3 0.5 0.7 0.9 1.1 1.3 1.5

Strike sequence:

0.5 0.7 0.9 1.1 1.3 1.5 1.7 1.9

Average price: 0.3909562

Minimum price: 0

Maximum price: 1.074814> plot(surface, color = divPalette(150, "RdBu"))

>

>

>

>

>

> dev.off()

null device

1

>

|