Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

American options pricing with Least Squares Monte Carlo methodDescriptionThe package compiles functions that calculate prices of American put options with Least Squares Monte Carlo method. The option types are plain vanilla American put, Asian American put, and Quanto American put. The pricing algorithms include variance reduction techniques such as Antithetic Variates and Control Variates. Additional functions are given to derive "price surfaces" at different volatilities and strikes, create 3-D plots, quickly generate Geometric Brownian motion, and calculate prices of European options with Black & Scholes analytical solution. Details

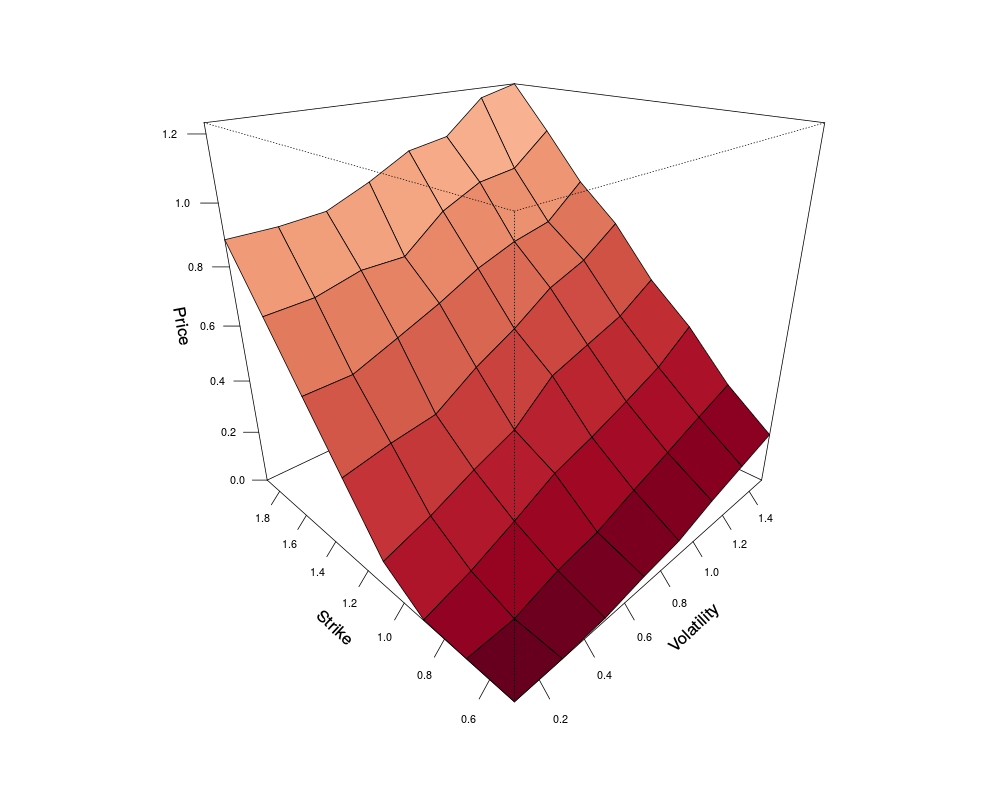

The Least Squares Monte Carlo is an approach developed to approximate the value of American options. It combines regression modeling and Monte Carlo simulation. The key feature of this method is estimation of the conditional expectation of the future pay-offs by a regression model (for details see Longstaff & Schwartz, 2000). The main pricing functions employing this method in the package are: Author(s)Mikhail A. Beketov Maintainer: Mikhail A. Beketov <mikhail.beketov@gmx.de> ReferencesGlasserman, P. 2004. Monte Carlo Methods in Financial Engineering. Springer. Longstaff, F.A., and E.S. Schwartz. 2000. Valuing american option by simulation: A simple least-squared approach. The Review of Financial Studies. 14:113-147. See AlsoFunctions: ExamplesPut<-AmerPutLSM(Spot=14.2, Strike=16.5, n=200, m=50) summary(Put) price(Put) plot(AmerPutLSMPriceSurf(vols = (seq(0.1, 1.5, 0.2)), n=200, m=10, strikes = (seq(0.5, 1.9, 0.2))), color = divPalette(150, "RdBu")) Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(LSMonteCarlo)

Loading required package: mvtnorm

Loading required package: fBasics

Loading required package: timeDate

Loading required package: timeSeries

Rmetrics Package fBasics

Analysing Markets and calculating Basic Statistics

Copyright (C) 2005-2014 Rmetrics Association Zurich

Educational Software for Financial Engineering and Computational Science

Rmetrics is free software and comes with ABSOLUTELY NO WARRANTY.

https://www.rmetrics.org --- Mail to: info@rmetrics.org

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/LSMonteCarlo/LSMonteCarlo-package.Rd_%03d_medium.png", width=480, height=480)

> ### Name: LSMonteCarlo-package

> ### Title: American options pricing with Least Squares Monte Carlo method

> ### Aliases: LSMonteCarlo-package LSMonteCarlo

> ### Keywords: Quantitative Finance Option pricing Monte Carlo Regression

>

> ### ** Examples

>

> Put<-AmerPutLSM(Spot=14.2, Strike=16.5, n=200, m=50)

> summary(Put)

American Put Option

Method: Simple Least Squares Monte Carlo

Option price 2.319598

Spot price 14.2

Strike 16.5

Volatility 0.2

Number of paths 200

Number of time-steps 50

Interest rate 0.06

Dividend rate 0

Maturity time 1

> price(Put)

[1] 2.319598

> plot(AmerPutLSMPriceSurf(vols = (seq(0.1, 1.5, 0.2)), n=200, m=10,

+ strikes = (seq(0.5, 1.9, 0.2))), color = divPalette(150, "RdBu"))

>

>

>

>

>

> dev.off()

null device

1

>

|