Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Markov Chain Monte Carlo for Ordered Probit Changepoint Regression ModelDescriptionThis function generates a sample from the posterior distribution of an ordered probit regression model with multiple parameter breaks. The function uses the Markov chain Monte Carlo method of Chib (1998). The user supplies data and priors, and a sample from the posterior distribution is returned as an mcmc object, which can be subsequently analyzed with functions provided in the coda package. UsageMCMCoprobitChange(formula, data=parent.frame(), m = 1,

burnin = 1000, mcmc = 1000, thin = 1, tune = NA, verbose = 0,

seed = NA, beta.start = NA, gamma.start=NA, P.start = NA,

b0 = NULL, B0 = NULL, a = NULL, b = NULL,

marginal.likelihood = c("none", "Chib95"), gamma.fixed=0, ...)

Arguments

Details

The model takes the following form: Pr(y_t = 1) = Phi(gamma_(c, m) - x_i'beta_m) - Phi(gamma_(c-1, m) - x_i'beta) Where M is the number of states, and gamma_(c, m) and beta_m are paramters when a state is m at t. We assume Gaussian distribution for prior of beta: beta_m ~ N(b0,B0^(-1)), m = 1,...,M. And: p_mm ~ Beta(a, b), m = 1,...,M. Where M is the number of states. Note that when the fitted changepoint model has very few observations in any of states, the marginal likelihood outcome can be “nan," which indicates that too many breaks are assumed given the model and data. ValueAn mcmc object that contains the posterior sample. This

object can be summarized by functions provided by the coda package.

The object contains an attribute ReferencesJong Hee Park. 2011. “Changepoint Analysis of Binary and Ordinal Probit Models: An Application to Bank Rate Policy Under the Interwar Gold Standard." Political Analysis. 19: 188-204. Andrew D. Martin, Kevin M. Quinn, and Jong Hee Park. 2011. “MCMCpack: Markov Chain Monte Carlo in R.”, Journal of Statistical Software. 42(9): 1-21. http://www.jstatsoft.org/v42/i09/. Siddhartha Chib. 1998. “Estimation and comparison of multiple change-point models.” Journal of Econometrics. 86: 221-241. See Also

Examples

set.seed(1909)

N <- 200

x1 <- rnorm(N, 1, .5);

## set a true break at 100

z1 <- 1 + x1[1:100] + rnorm(100);

z2 <- 1 -0.2*x1[101:200] + rnorm(100);

z <- c(z1, z2);

y <- z

## generate y

y[z < 1] <- 1;

y[z >= 1 & z < 2] <- 2;

y[z >= 2] <- 3;

## inputs

formula <- y ~ x1

## fit multiple models with a varying number of breaks

out1 <- MCMCoprobitChange(formula, m=1,

mcmc=100, burnin=100, thin=1, tune=c(.5, .5), verbose=100,

b0=0, B0=10, marginal.likelihood = "Chib95")

out2 <- MCMCoprobitChange(formula, m=2,

mcmc=100, burnin=100, thin=1, tune=c(.5, .5, .5), verbose=100,

b0=0, B0=10, marginal.likelihood = "Chib95")

## Do model comparison

## NOTE: the chain should be run longer than this example!

BayesFactor(out1, out2)

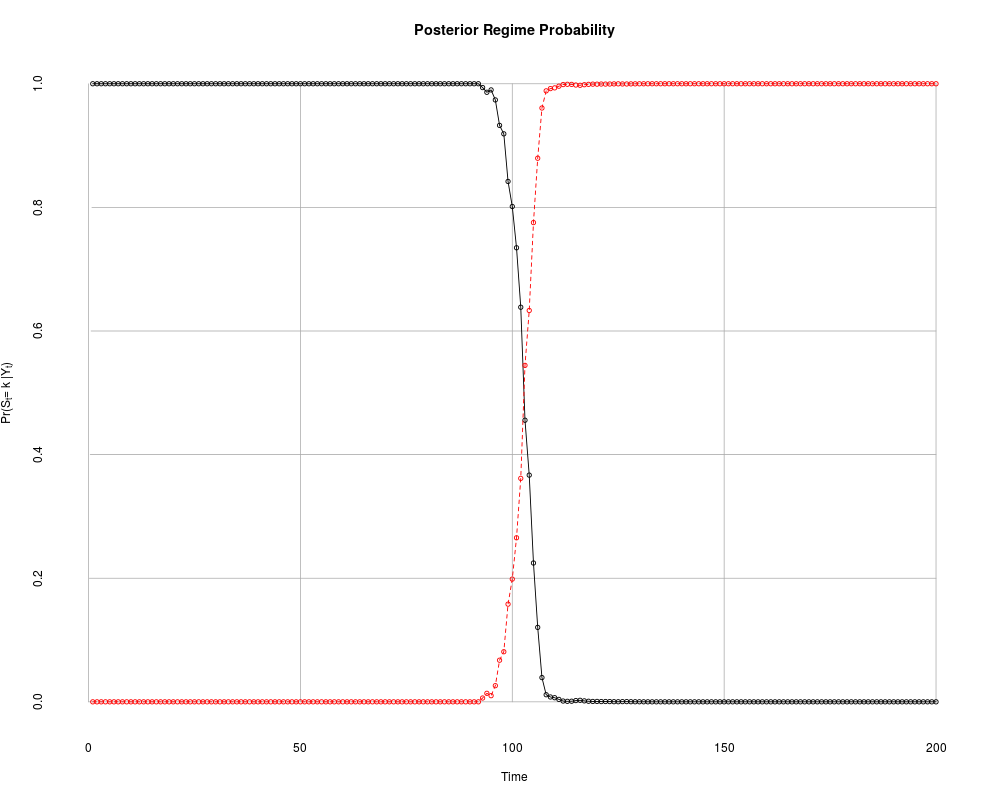

## draw plots using the "right" model

plotState(out1)

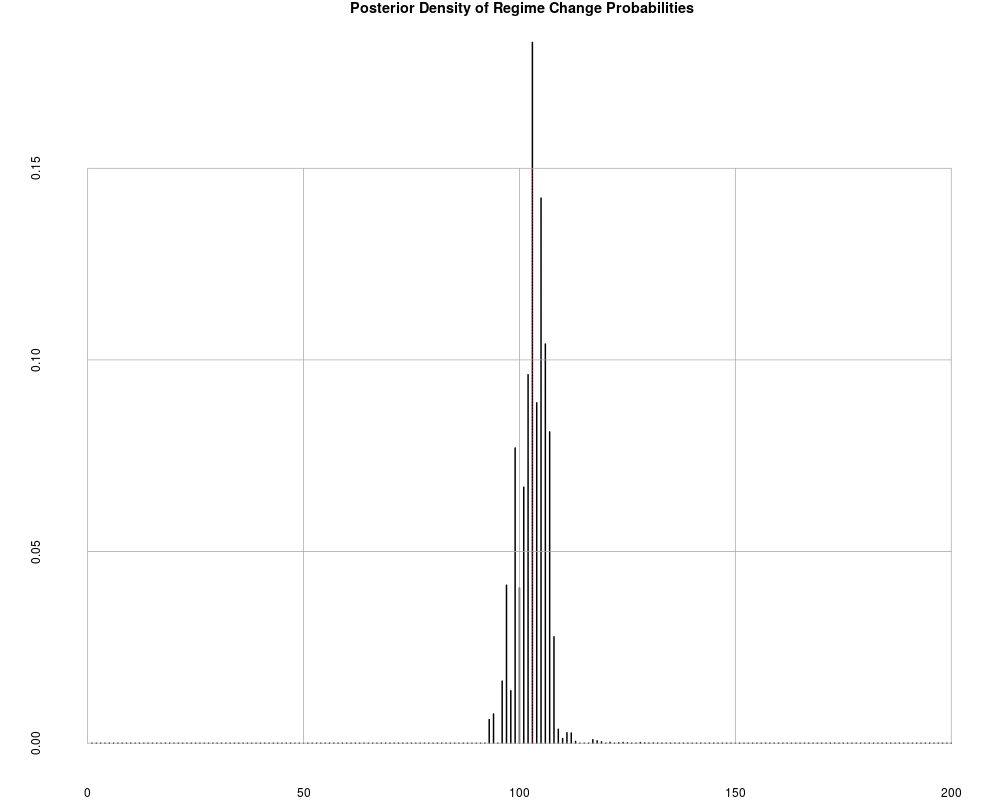

plotChangepoint(out1)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(MCMCpack)

Loading required package: coda

Loading required package: MASS

##

## Markov Chain Monte Carlo Package (MCMCpack)

## Copyright (C) 2003-2016 Andrew D. Martin, Kevin M. Quinn, and Jong Hee Park

##

## Support provided by the U.S. National Science Foundation

## (Grants SES-0350646 and SES-0350613)

##

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/MCMCpack/MCMCoprobitChange.Rd_%03d_medium.png", width=480, height=480)

> ### Name: MCMCoprobitChange

> ### Title: Markov Chain Monte Carlo for Ordered Probit Changepoint

> ### Regression Model

> ### Aliases: MCMCoprobitChange

> ### Keywords: models

>

> ### ** Examples

>

> set.seed(1909)

> N <- 200

> x1 <- rnorm(N, 1, .5);

>

> ## set a true break at 100

> z1 <- 1 + x1[1:100] + rnorm(100);

> z2 <- 1 -0.2*x1[101:200] + rnorm(100);

> z <- c(z1, z2);

> y <- z

>

> ## generate y

> y[z < 1] <- 1;

> y[z >= 1 & z < 2] <- 2;

> y[z >= 2] <- 3;

>

> ## inputs

> formula <- y ~ x1

>

> ## fit multiple models with a varying number of breaks

> out1 <- MCMCoprobitChange(formula, m=1,

+ mcmc=100, burnin=100, thin=1, tune=c(.5, .5), verbose=100,

+ b0=0, B0=10, marginal.likelihood = "Chib95")

MCMCoprobitChange iteration 101 of 200

Acceptance rate for state 1 is 0.53000

Acceptance rate for state 2 is 0.20000

The number of observations in state 1 is 00097

The number of observations in state 2 is 00103

beta 0 = 0.09304 0.52479

beta 1 = -0.27336 0.16873

gamma 0 = 0.74271

gamma 1 = 0.99581

logmarglike = -220.60851

loglike = -192.32574

log_prior = -4.61781

log_beta = 4.33846

log_P = 3.63139

log_gamma = 15.69512

> out2 <- MCMCoprobitChange(formula, m=2,

+ mcmc=100, burnin=100, thin=1, tune=c(.5, .5, .5), verbose=100,

+ b0=0, B0=10, marginal.likelihood = "Chib95")

MCMCoprobitChange iteration 101 of 200

Acceptance rate for state 1 is 0.61000

Acceptance rate for state 2 is 0.81000

Acceptance rate for state 3 is 0.21000

The number of observations in state 1 is 00001

The number of observations in state 2 is 00001

The number of observations in state 3 is 00198

beta 0 = 0.09056 0.25382

beta 1 = -0.54118 -0.45300

beta 2 = -0.33464 0.54185

gamma 0 = 0.92141

gamma 1 = 1.23897

gamma 2 = 0.70838

logmarglike = -241.98699

loglike = -212.84326

log_prior = -8.97530

log_beta = 3.75571

log_P = 2.18454

log_gamma = 14.22818

>

> ## Do model comparison

> ## NOTE: the chain should be run longer than this example!

> BayesFactor(out1, out2)

The matrix of Bayes Factors is:

out1 out2

out1 1.00e+00 1.93e+09

out2 5.19e-10 1.00e+00

The matrix of the natural log Bayes Factors is:

out1 out2

out1 0.0 21.4

out2 -21.4 0.0

out1 :

call =

MCMCoprobitChange(formula = formula, m = 1, burnin = 100, mcmc = 100,

thin = 1, tune = c(0.5, 0.5), verbose = 100, b0 = 0, B0 = 10,

marginal.likelihood = "Chib95")

log marginal likelihood = -220.6085

out2 :

call =

MCMCoprobitChange(formula = formula, m = 2, burnin = 100, mcmc = 100,

thin = 1, tune = c(0.5, 0.5, 0.5), verbose = 100, b0 = 0,

B0 = 10, marginal.likelihood = "Chib95")

log marginal likelihood = -241.987

>

> ## draw plots using the "right" model

> plotState(out1)

> plotChangepoint(out1)

>

>

>

>

>

> dev.off()

null device

1

>

|