Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Repeat Sales Estimation using Fourier ExpansionsDescriptionStandard and Weighted Least Squares Repeat Sales Estimation using Fourier Expansions Usagerepsalefourier(price0,time0,price1,time1,mergefirst=1,q=1, graph=TRUE, graph.conf=TRUE,conf=.95,stage3=FALSE,stage3_xlist=~timesale, print=TRUE) Arguments

DetailsThe repeat sales model is y(t) - y(s) = δ(t) - δ(s) + u(t) - u(s) where y is the log of sale price, s denotes the earlier sale in a repeat sales pair, and t denotes the later sale. Each entry of the data set should represent a repeat sales pair, with price0 = y(s), price1 = y(t), time0 = s, and time1 = t. The function repsaledata can help transfer a standard hedonic data set to a set of repeat sales pairs. The repeat sales model can be derived from a hedonic price function with the form y_{i,t} = δ_t + X_i β + u_{i,t} where X_i is a vector of variables that are assumed constant over time. repsalefourier replaces δ_t with a smooth continuous function, g(T_i) where T_i denotes the time of sale for observation i. Letting g(T_i) = α_0 + α_1 z_i + α_2 z_i^2 + ∑_{i=1}^Q {λ_q sin(qz_i) + γ_q cos(qz_i) } , where z_i = 2 π (T_i - min(T_i))/(max(T_i) - min(T_i)) , the repeat sales model becomes y_{i,t} - y_{i,s} = g(T_i) - g(T_i^s) = α_1 (z_i - z_i^s) + α_2 (z_i^2 - z_i^{s2}) + ∑_{q=1}^Q { λ_q (sin(qz_i) - sin(qz_i^s)) + γ_q (cos(qz_i) - cos(z_i^s)) } + u_{i,t} - u_{i,t-s} After imposing the constraint that the price index in the base time period equals zero, the index is constructed from the estimated regression using the following expression: g(T_i) = α_1 z_i + α_2 z_i^2 + ∑_{q=1}^Q { λ_q sin(qz_i) + γ_q (cos(qz_i) - 1) } More details can be found in McMillen and Dombrow (2001). Repeat sales estimates are sometimes very sensitive to sales from the first few time periods, particularly when the sample size is small. The option mergefirst indicates the number of time periods for which the price index is constrained to equal zero. The default is mergefirst = 1, meaning that the price index equals zero for just the first time period. The repsalefourier command does not have an option for including an intercept in the model. Following Case and Shiller (1987), many authors use a three-stage procedure to construct repeat sales price indexes that are adjusted for heteroskedasticity related to the length of time between sales. Common specifications for the second-stage function are e^2 = α0 + α1 (t-s) or |e| = α0 + α1 (t-s), where e represents the first-stage residuals. The first equation implies an error variance of σ^2 = e^2 and the second equation leads to σ^2 = |e|^2. The repsalefourier function uses a standard F test to determine whether the slope cofficients are significant in the second-stage regression. The results are reported if print=T. The third-stage equation is (y(t) - y(s))/σ = (g(T) - g(T_s))/σ + (u(t) - u(s))/σ This equation is estimated by regressing y(t) - y(s) on z, z^2, sin(z)...sin(Qz), cos(z)...cos(Qz) using the weights option in lm with weights = 1/sigma^2 Value

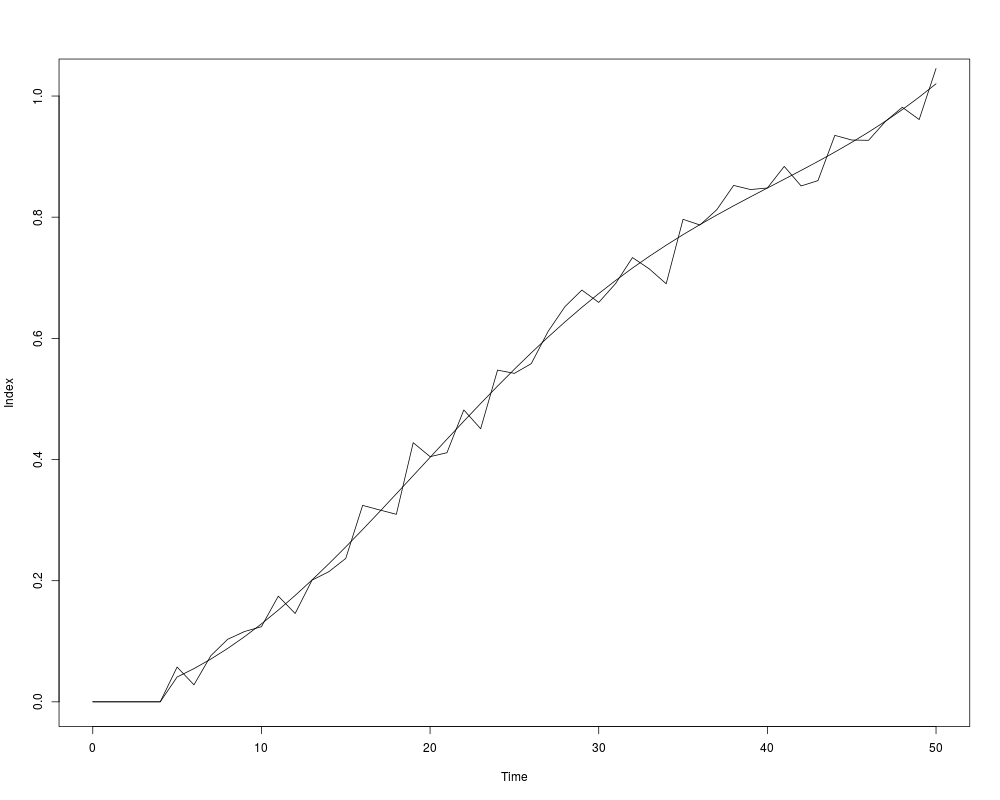

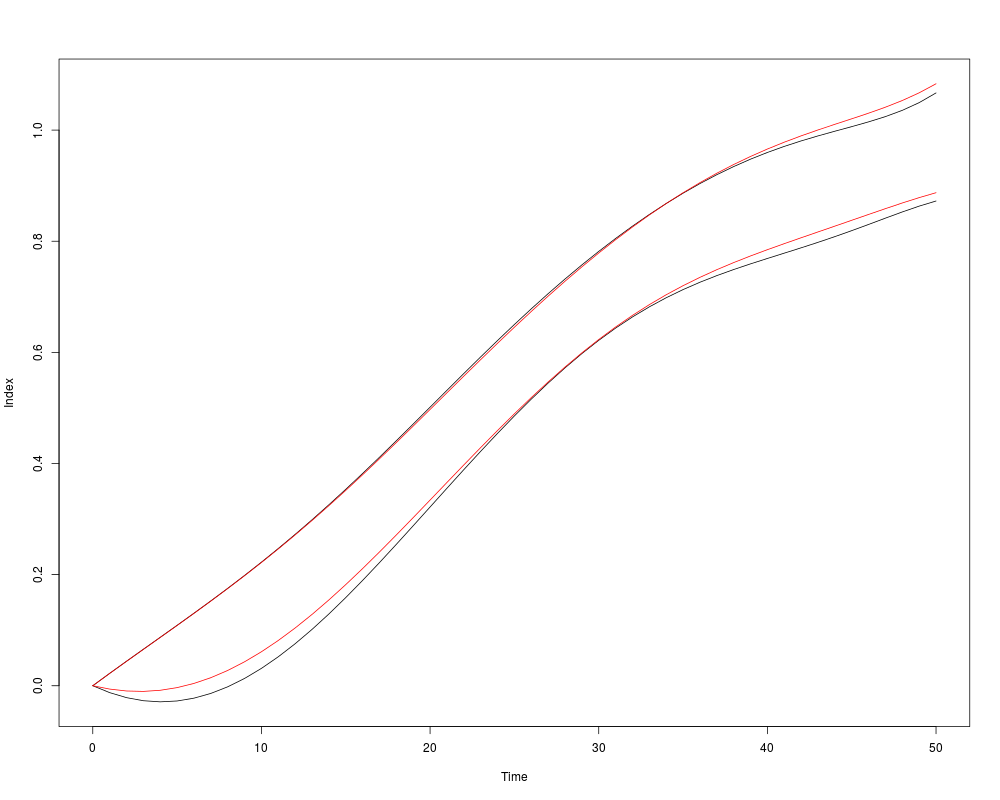

ReferencesCase, Karl and Robert Shiller, "Prices of Single-Family Homes since 1970: New Indexes for Four Cities," New England Economic Review (1987), 45-56. McMillen, Daniel P. and Jonathan Dombrow, "A Flexible Fourier Approach to Repeat Sales Price Indexes," Real Estate Economics 29 (2001), 207-225. See Alsorepsale repsaledata repsaleqreg Examplesset.seed(189) n = 2000 # sale dates range from 0-50 # drawn uniformly from all possible time0, time1 combinations with time0<time1 tmat <- expand.grid(seq(0,50), seq(0,50)) tmat <- tmat[tmat[,1]<tmat[,2], ] tobs <- sample(seq(1:nrow(tmat)),n,replace=TRUE) time0 <- tmat[tobs,1] time1 <- tmat[tobs,2] timesale <- time1-time0 timesale2 <- timesale^2 par(ask=TRUE) z0 <- 2*pi*time0/50 z0sq <- z0^2 sin0 <- sin(z0) cos0 <- cos(z0) z1 <- 2*pi*time1/50 z1sq <- z1^2 sin1 <- sin(z1) cos1 <- cos(z1) ybase0 <- z0 + .05*z0sq -.5*sin0 - .5*cos0 miny <- min(ybase0) ybase0 <- ybase0-miny ybase1 <- z1 + .05*z1sq -.5*sin1 - .5*cos1 - miny maxy <- max(ybase1) ybase0 <- ybase0/maxy ybase1 <- ybase1/maxy summary(data.frame(ybase0,ybase1)) sig1 = sd(c(ybase0,ybase1))/2 y0 <- ybase0 + rnorm(n,0,sig1) y1 <- ybase1 + rnorm(n,0,sig1) fit <- lm(y0~z0+z0sq+sin0+cos0) summary(fit) plot(time0,fitted(fit)) fit <- lm(y1~z1+z1sq+sin1+cos1) summary(fit) plot(time1,fitted(fit)) fit1 <- repsale(price1=y1,price0=y0,time1=time1,time0=time0,graph=FALSE, mergefirst=5) fit2 <- repsalefourier(price1=y1,price0=y0,time1=time1,time0=time0,q=1, graph=FALSE,mergefirst=5) timevar <- seq(0,50) plot(timevar,fit1$pindex,type="l",xlab="Time",ylab="Index", ylim=c(min(fit1$pindex),max(fit2$pindex))) lines(timevar,fit2$pindex) # variance rises with timesale # var(u0) = sig1^2; var(u1) = (sig1 + timesale/50)^2 # var(u1-u0) = var(u0) + var(u1) = 2*(sig1^2) + 2*sig1*timesale/10 + (timesale^2)/2500 y0 <- ybase0 + rnorm(n,0,sig1) y1 <- ybase1 + rnorm(n,0,sig1+timesale/50) par(ask=TRUE) fit1 <- repsalefourier(price0=y0, price1=y1, time0=time0, time1=time1, graph=FALSE) fit2 <- repsalefourier(price0=y0, price1=y1, time0=time0, time1=time1, graph=FALSE,stage3="abs",stage3_xlist=~timesale+timesale2) plot(timevar,fit1$lo,type="l",xlab="Time",ylab="Index", ylim=c(min(fit1$lo,fit2$lo),max(fit1$hi,fit2$hi))) lines(timevar,fit1$hi) lines(timevar,fit2$lo,col="red") lines(timevar,fit2$hi,col="red") Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(McSpatial)

Loading required package: lattice

Loading required package: locfit

locfit 1.5-9.1 2013-03-22

Loading required package: maptools

Loading required package: sp

Checking rgeos availability: TRUE

Loading required package: quantreg

Loading required package: SparseM

Attaching package: 'SparseM'

The following object is masked from 'package:base':

backsolve

Loading required package: RANN

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/McSpatial/repsalefourier.Rd_%03d_medium.png", width=480, height=480)

> ### Name: repsalefourier

> ### Title: Repeat Sales Estimation using Fourier Expansions

> ### Aliases: repsalefourier

> ### Keywords: Repeat Sales Series Expansions

>

> ### ** Examples

>

> set.seed(189)

> n = 2000

> # sale dates range from 0-50

> # drawn uniformly from all possible time0, time1 combinations with time0<time1

> tmat <- expand.grid(seq(0,50), seq(0,50))

> tmat <- tmat[tmat[,1]<tmat[,2], ]

> tobs <- sample(seq(1:nrow(tmat)),n,replace=TRUE)

> time0 <- tmat[tobs,1]

> time1 <- tmat[tobs,2]

> timesale <- time1-time0

> timesale2 <- timesale^2

>

> par(ask=TRUE)

> z0 <- 2*pi*time0/50

> z0sq <- z0^2

> sin0 <- sin(z0)

> cos0 <- cos(z0)

> z1 <- 2*pi*time1/50

> z1sq <- z1^2

> sin1 <- sin(z1)

> cos1 <- cos(z1)

> ybase0 <- z0 + .05*z0sq -.5*sin0 - .5*cos0

> miny <- min(ybase0)

> ybase0 <- ybase0-miny

> ybase1 <- z1 + .05*z1sq -.5*sin1 - .5*cos1 - miny

> maxy <- max(ybase1)

> ybase0 <- ybase0/maxy

> ybase1 <- ybase1/maxy

> summary(data.frame(ybase0,ybase1))

ybase0 ybase1

Min. :0.00000 Min. :0.01766

1st Qu.:0.06972 1st Qu.:0.58855

Median :0.24423 Median :0.81880

Mean :0.32742 Mean :0.71910

3rd Qu.:0.53337 3rd Qu.:0.91262

Max. :0.98338 Max. :1.00000

> sig1 = sd(c(ybase0,ybase1))/2

> y0 <- ybase0 + rnorm(n,0,sig1)

> y1 <- ybase1 + rnorm(n,0,sig1)

> fit <- lm(y0~z0+z0sq+sin0+cos0)

> summary(fit)

Call:

lm(formula = y0 ~ z0 + z0sq + sin0 + cos0)

Residuals:

Min 1Q Median 3Q Max

-0.46899 -0.11088 0.00102 0.10987 0.55996

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.126480 0.029869 4.235 2.39e-05 ***

z0 0.052986 0.033681 1.573 0.11584

z0sq 0.017544 0.006042 2.904 0.00373 **

sin0 -0.054164 0.012599 -4.299 1.80e-05 ***

cos0 -0.101442 0.021464 -4.726 2.45e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1621 on 1995 degrees of freedom

Multiple R-squared: 0.7489, Adjusted R-squared: 0.7484

F-statistic: 1487 on 4 and 1995 DF, p-value: < 2.2e-16

> plot(time0,fitted(fit))

> fit <- lm(y1~z1+z1sq+sin1+cos1)

> summary(fit)

Call:

lm(formula = y1 ~ z1 + z1sq + sin1 + cos1)

Residuals:

Min 1Q Median 3Q Max

-0.53279 -0.11361 0.00073 0.11066 0.56063

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.066206 0.062896 1.053 0.292642

z1 0.097339 0.045591 2.135 0.032879 *

z1sq 0.011277 0.006403 1.761 0.078365 .

sin1 -0.049476 0.013680 -3.617 0.000306 ***

cos1 -0.085123 0.022339 -3.811 0.000143 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1665 on 1995 degrees of freedom

Multiple R-squared: 0.7127, Adjusted R-squared: 0.7121

F-statistic: 1237 on 4 and 1995 DF, p-value: < 2.2e-16

> plot(time1,fitted(fit))

>

> fit1 <- repsale(price1=y1,price0=y0,time1=time1,time0=time0,graph=FALSE,

+ mergefirst=5)

Call:

lm(formula = dy ~ xmat + 0)

Residuals:

Min 1Q Median 3Q Max

-0.76791 -0.15748 -0.00397 0.14970 0.76721

Coefficients:

Estimate Std. Error t value Pr(>|t|)

Time 6 0.05741 0.02860 2.007 0.044860 *

Time 7 0.02809 0.02881 0.975 0.329652

Time 8 0.07619 0.02834 2.688 0.007240 **

Time 9 0.10328 0.02664 3.877 0.000109 ***

Time 10 0.11611 0.02858 4.063 5.05e-05 ***

Time 11 0.12408 0.02939 4.223 2.53e-05 ***

Time 12 0.17446 0.02719 6.416 1.75e-10 ***

Time 13 0.14583 0.02836 5.142 3.00e-07 ***

Time 14 0.20087 0.02746 7.315 3.73e-13 ***

Time 15 0.21490 0.02943 7.301 4.13e-13 ***

Time 16 0.23677 0.02787 8.497 < 2e-16 ***

Time 17 0.32424 0.02677 12.113 < 2e-16 ***

Time 18 0.31677 0.02797 11.325 < 2e-16 ***

Time 19 0.30955 0.02992 10.347 < 2e-16 ***

Time 20 0.42779 0.02951 14.496 < 2e-16 ***

Time 21 0.40472 0.03106 13.032 < 2e-16 ***

Time 22 0.41121 0.02844 14.457 < 2e-16 ***

Time 23 0.48181 0.02746 17.546 < 2e-16 ***

Time 24 0.45078 0.02792 16.146 < 2e-16 ***

Time 25 0.54754 0.03002 18.240 < 2e-16 ***

Time 26 0.54222 0.02950 18.382 < 2e-16 ***

Time 27 0.55827 0.02995 18.643 < 2e-16 ***

Time 28 0.61153 0.02772 22.058 < 2e-16 ***

Time 29 0.65244 0.03033 21.512 < 2e-16 ***

Time 30 0.67971 0.02963 22.936 < 2e-16 ***

Time 31 0.65930 0.02859 23.064 < 2e-16 ***

Time 32 0.69045 0.02967 23.268 < 2e-16 ***

Time 33 0.73335 0.02935 24.985 < 2e-16 ***

Time 34 0.71458 0.02784 25.666 < 2e-16 ***

Time 35 0.69007 0.02876 23.991 < 2e-16 ***

Time 36 0.79646 0.02681 29.703 < 2e-16 ***

Time 37 0.78707 0.03031 25.968 < 2e-16 ***

Time 38 0.81238 0.02665 30.480 < 2e-16 ***

Time 39 0.85246 0.02847 29.940 < 2e-16 ***

Time 40 0.84563 0.02729 30.991 < 2e-16 ***

Time 41 0.84820 0.02801 30.277 < 2e-16 ***

Time 42 0.88384 0.02943 30.028 < 2e-16 ***

Time 43 0.85156 0.02878 29.584 < 2e-16 ***

Time 44 0.86039 0.02856 30.125 < 2e-16 ***

Time 45 0.93503 0.02803 33.356 < 2e-16 ***

Time 46 0.92738 0.02669 34.745 < 2e-16 ***

Time 47 0.92690 0.02774 33.418 < 2e-16 ***

Time 48 0.95810 0.02707 35.399 < 2e-16 ***

Time 49 0.98146 0.02731 35.939 < 2e-16 ***

Time 50 0.96114 0.02964 32.423 < 2e-16 ***

Time 51 1.04543 0.02733 38.259 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2303 on 1954 degrees of freedom

Multiple R-squared: 0.8205, Adjusted R-squared: 0.8162

F-statistic: 194.1 on 46 and 1954 DF, p-value: < 2.2e-16

> fit2 <- repsalefourier(price1=y1,price0=y0,time1=time1,time0=time0,q=1,

+ graph=FALSE,mergefirst=5)

Call:

lm(formula = dy ~ xmat + 0)

Residuals:

Min 1Q Median 3Q Max

-0.82133 -0.16028 -0.00466 0.15482 0.75944

Coefficients:

Estimate Std. Error t value Pr(>|t|)

dz 0.086426 0.021788 3.967 7.55e-05 ***

dzsq 0.012088 0.003562 3.393 0.000704 ***

dsin(1z) -0.056430 0.007327 -7.702 2.09e-14 ***

dcos(1z) -0.079129 0.016125 -4.907 9.99e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2301 on 1996 degrees of freedom

Multiple R-squared: 0.8168, Adjusted R-squared: 0.8164

F-statistic: 2225 on 4 and 1996 DF, p-value: < 2.2e-16

> timevar <- seq(0,50)

> plot(timevar,fit1$pindex,type="l",xlab="Time",ylab="Index",

+ ylim=c(min(fit1$pindex),max(fit2$pindex)))

> lines(timevar,fit2$pindex)

>

>

>

> # variance rises with timesale

> # var(u0) = sig1^2; var(u1) = (sig1 + timesale/50)^2

> # var(u1-u0) = var(u0) + var(u1) = 2*(sig1^2) + 2*sig1*timesale/10 + (timesale^2)/2500

> y0 <- ybase0 + rnorm(n,0,sig1)

> y1 <- ybase1 + rnorm(n,0,sig1+timesale/50)

> par(ask=TRUE)

> fit1 <- repsalefourier(price0=y0, price1=y1, time0=time0, time1=time1,

+ graph=FALSE)

Call:

lm(formula = dy ~ xmat + 0)

Residuals:

Min 1Q Median 3Q Max

-3.1965 -0.3373 0.0067 0.3468 2.1758

Coefficients:

Estimate Std. Error t value Pr(>|t|)

dz 0.115576 0.069150 1.671 0.0948 .

dzsq 0.006168 0.010909 0.565 0.5719

dsin(1z) -0.081898 0.020915 -3.916 9.32e-05 ***

dcos(1z) -0.071968 0.046635 -1.543 0.1229

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.618 on 1996 degrees of freedom

Multiple R-squared: 0.3797, Adjusted R-squared: 0.3785

F-statistic: 305.5 on 4 and 1996 DF, p-value: < 2.2e-16

> fit2 <- repsalefourier(price0=y0, price1=y1, time0=time0, time1=time1,

+ graph=FALSE,stage3="abs",stage3_xlist=~timesale+timesale2)

F-value for heteroskedasticity test = 301.6005

p-value = 1

Call:

lm(formula = dy ~ xmat + 0, weights = wgt)

Weighted Residuals:

Min 1Q Median 3Q Max

-4.7727 -0.8578 0.0099 0.8443 3.8578

Coefficients:

Estimate Std. Error t value Pr(>|t|)

dz 0.135092 0.056093 2.408 0.0161 *

dzsq 0.003459 0.008834 0.392 0.6954

dsin(1z) -0.075015 0.017315 -4.332 1.55e-05 ***

dcos(1z) -0.054409 0.036713 -1.482 0.1385

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.239 on 1996 degrees of freedom

Multiple R-squared: 0.3086, Adjusted R-squared: 0.3072

F-statistic: 222.7 on 4 and 1996 DF, p-value: < 2.2e-16

> plot(timevar,fit1$lo,type="l",xlab="Time",ylab="Index",

+ ylim=c(min(fit1$lo,fit2$lo),max(fit1$hi,fit2$hi)))

> lines(timevar,fit1$hi)

> lines(timevar,fit2$lo,col="red")

> lines(timevar,fit2$hi,col="red")

>

>

>

>

>

>

> dev.off()

null device

1

>

|