Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Maximum Likelihood Shrinkage in RegressionDescriptionIdentify and display TRACEs for the Q-shaped shrinkage path, including the M-extent of shrinkage along that path, that are most likely under normal distribution theory to yield optimal reducions in MSE Risk. Usage

RXridge(form, data, rscale = 1, Q = "qmse", steps = 8, nq = 21,

qmax = 5, qmin = -5, omdmin = 9.9e-13)

Arguments

DetailsIllconditioned and/or nearly multicollinear regression models are unlikely to produce Ordinary Least Squares (OLS) regression coefficient estimates that are very close, numerically, to their unknown true values. Specifically, OLS estimates can then tend to have "wrong" numerical signs and/or unreasable relative magnitudes, while shrunken (generalized ridge) estimates chosen to maximize their likelihood of reducing Mean Squared Error (MSE) Risk (expected loss) can be much more stable and reasonable, numerically. On the other hand, because only OLS estimates are quaranteed to be minimax when risk is matrix valued (truly multivariate), no guarantee of an actual reduction in MSE Risk is necessarily associated with shrinkage. ValueAn output list object of class RXridge:

Author(s)Bob Obenchain <wizbob@att.net> ReferencesGoldstein M, Smith AFM. (1974) Ridge-type estimators for regression analysis. J. Roy. Stat. Soc. B 36, 284-291. (2-parameter shrinkage family.) Burr TL, Fry HA. (2005) Biased Regression: The Case for Cautious Application. Technometrics 47, 284-296. Obenchain RL. (2005) Shrinkage Regression: ridge, BLUP, Bayes, spline and Stein. Electronic book-in-progress (200+ pages.) http://members.iquest.net/~softrx/. Obenchain RL. (2011) shrink.PDF Vignette-like documentation stored in the R library/RXshrink/doc folder. 23 pages. See Also

Examplesdata(longley2) form <- GNP~GNP.deflator+Unemployed+Armed.Forces+Population+Year+Employed rxrobj <- RXridge(form, data=longley2) rxrobj names(rxrobj) plot(rxrobj) Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(RXshrink)

Loading required package: lars

Loaded lars 1.2

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/RXshrink/RXridge.Rd_%03d_medium.png", width=480, height=480)

> ### Name: RXridge

> ### Title: Maximum Likelihood Shrinkage in Regression

> ### Aliases: RXridge

> ### Keywords: regression hplot

>

> ### ** Examples

>

> data(longley2)

> form <- GNP~GNP.deflator+Unemployed+Armed.Forces+Population+Year+Employed

> rxrobj <- RXridge(form, data=longley2)

> rxrobj

RXridge Object: Shrinkage-Ridge Regression Model Specification

Data Frame: longley2

Regression Equation:

GNP ~ GNP.deflator + Unemployed + Armed.Forces + Population +

Year + Employed

Number of Regressor Variables, p = 6

Number of Observations, n = 29

Principal Axis Summary Statistics of Ill-Conditioning...

LAMBDA SV COMP RHO TRAT

1 124.55432117 11.1603907 0.466590166 0.98409260 179.451944

2 34.04395492 5.8347198 -0.009779055 -0.01078296 -1.966301

3 7.97601572 2.8241841 0.228918857 0.12217872 22.279619

4 1.31429584 1.1464274 -0.557948473 -0.12088200 -22.043160

5 0.06505309 0.2550551 0.613987118 0.02959472 5.396677

6 0.04635925 0.2153120 -0.471410409 -0.01918176 -3.497845

Residual Mean Square for Error = 0.0008420418

Estimate of Residual Std. Error = 0.02901796

Classical Maximum Likelihood choice of SHAPE(Q) and EXTENT(M) of

shrinkage in the 2-parameter generalized ridge family...

Q CRLQ M K CHISQ

1 5.0 0.03065132 5.973237 9.992836e+06 212.2772

2 4.5 0.03143266 5.971855 2.123279e+06 212.2758

3 4.0 0.03244203 5.970023 4.476833e+05 212.2739

4 3.5 0.03402277 5.967055 9.194427e+04 212.2709

5 3.0 0.03715373 5.960805 1.752828e+04 212.2644

6 2.5 0.04516043 5.942561 2.721213e+03 212.2453

7 2.0 0.07215281 5.858787 2.496728e+02 212.1532

8 1.5 0.18443773 5.252697 9.850159e+00 211.3015

9 1.0 0.52547213 2.111210 5.428963e-01 202.9410

10 0.5 0.79341430 1.816359 4.358166e-01 183.5424

11 0.0 0.89070908 2.678418 1.513692e+00 166.6511

12 -0.5 0.93599740 3.140371 7.907552e+00 151.8817

13 -1.0 0.95935445 3.453422 5.035840e+01 139.1481

14 -1.5 0.97160704 3.723747 3.725912e+02 129.0260

15 -2.0 0.97800933 3.935491 3.139861e+03 121.8070

16 -2.5 0.98131461 4.068103 2.941270e+04 117.2079

17 -3.0 0.98299124 4.168863 2.970284e+05 114.5558

18 -3.5 0.98382102 4.283839 3.143926e+06 113.1458

19 -4.0 0.98421686 4.427912 3.417785e+07 112.4479

20 -4.5 0.98439456 4.586356 3.768549e+08 112.1289

21 -5.0 0.98446554 4.729924 4.185069e+09 112.0005

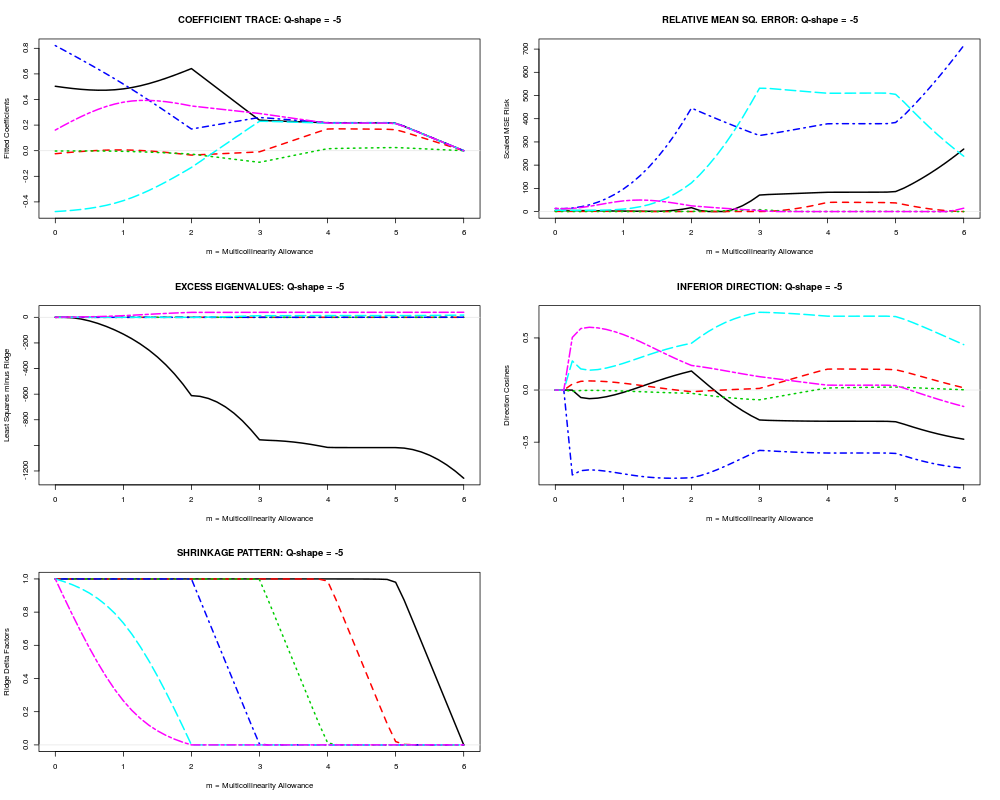

Q = -5 is the path shape most likely to lead to minimum

MSE risk because this shape maximizes CRLQ and minimizes CHISQ.

RXridge: Shrinkage PATH Shape = -5

The extent of shrinkage (M value) most likely to be optimal

in the Q-shape = -5 2-parameter ridge family can depend

upon whether one uses the Classical, Empirical Bayes, or Random

Coefficient criterion. In each case, the objective is to

minimize the minus-two-log-likelihood statistics listed below:

M K CLIK EBAY RCOF

0 0.000 0.000000e+00 Inf Inf Inf

1 0.125 1.216886e-09 1.756397e+12 113.2484 113.7283

2 0.250 2.723817e-09 1.759946e+12 112.8258 113.6267

3 0.375 4.619196e-09 1.761921e+12 113.3184 114.2927

4 0.500 7.041824e-09 1.763266e+12 114.2322 115.2383

5 0.625 1.018846e-08 1.764282e+12 115.4263 116.3236

6 0.750 1.433883e-08 1.765097e+12 116.8508 117.4949

7 0.875 1.989252e-08 1.765775e+12 118.4883 118.7274

8 1.000 2.742919e-08 1.766353e+12 120.3319 120.0052

9 1.125 3.782128e-08 1.766854e+12 122.3731 121.3120

10 1.250 5.247015e-08 1.767295e+12 124.5961 122.6278

11 1.375 7.384438e-08 1.767690e+12 126.9746 123.9280

12 1.500 1.068417e-07 1.768051e+12 129.4727 125.1831

13 1.625 1.628770e-07 1.768393e+12 132.0423 126.3550

14 1.750 2.762155e-07 1.701520e+12 134.5264 127.2992

15 1.875 6.182665e-07 1.272220e+12 136.0903 127.1936

16 2.000 6.643946e-04 1.015978e+12 125.4323 114.7166

17 2.125 7.362916e-01 3.287066e+10 166.0541 114.1279

18 2.250 1.717996e+00 3.205070e+10 224.4040 123.2937

19 2.375 3.092344e+00 3.183538e+10 283.5606 129.9525

20 2.500 5.153758e+00 2.280920e+10 342.6568 134.7201

21 2.625 8.589062e+00 1.368552e+10 401.6391 138.2106

22 2.750 1.545756e+01 7.604699e+09 460.4319 140.7063

23 2.875 3.603308e+01 3.262206e+09 518.4773 141.8635

24 3.000 1.151864e+03 1.020496e+08 568.7408 134.7453

25 3.125 3.681964e+04 3.192275e+06 620.4632 127.5772

26 3.250 8.582348e+04 1.369417e+06 680.1102 127.9952

27 3.375 1.544348e+05 7.609366e+05 740.5562 128.9705

28 3.500 2.573141e+05 4.566294e+05 801.2635 130.0100

29 3.625 4.286244e+05 2.740626e+05 862.0149 130.9378

30 3.750 7.703843e+05 1.524187e+05 922.6029 131.6017

31 3.875 1.783600e+06 6.576456e+04 982.5073 131.6508

32 4.000 2.001657e+07 5.802433e+03 1034.0751 128.3256

33 4.125 2.246123e+08 5.233168e+02 1037.2882 123.8210

34 4.250 5.199270e+08 2.503376e+02 1039.1120 122.3877

35 4.375 9.341967e+08 1.669789e+02 1042.2842 121.5122

36 4.500 1.555265e+09 1.313719e+02 1047.3773 120.8768

37 4.625 2.588153e+09 1.157462e+02 1056.0587 120.4012

38 4.750 4.641076e+09 1.121409e+02 1073.4679 120.1243

39 4.875 1.062368e+10 1.206503e+02 1124.3692 120.4956

40 5.000 7.624894e+10 1.585962e+02 1675.8231 129.9001

41 5.125 5.472829e+11 1.878722e+02 5146.2928 160.3667

42 5.250 1.252858e+12 1.954643e+02 9119.6085 176.2351

43 5.375 2.246916e+12 1.994637e+02 13126.9105 186.3760

44 5.500 3.740036e+12 2.022119e+02 17143.1003 193.8197

45 5.625 6.229664e+12 2.043992e+02 21162.8987 199.6993

46 5.750 1.120975e+13 2.063548e+02 25184.5175 204.5580

47 5.875 2.615094e+13 2.083713e+02 29207.1835 208.6979

48 6.000 Inf 2.123044e+02 33230.5079 212.3044

Extent of shrinkage statistics...

TSMSE KONST MCAL

0 37.86637 0.000000e+00 0.000

1 35.63211 1.216886e-09 0.125

2 39.12317 2.723817e-09 0.250

3 47.93770 4.619196e-09 0.375

4 61.61001 7.041824e-09 0.500

5 79.63968 1.018846e-08 0.625

6 101.56149 1.433883e-08 0.750

7 127.06069 1.989252e-08 0.875

8 156.63450 2.742919e-08 1.000

9 190.20102 3.782128e-08 1.125

10 228.25031 5.247015e-08 1.250

11 271.54570 7.384438e-08 1.375

12 321.12648 1.068417e-07 1.500

13 379.33422 1.628770e-07 1.625

14 446.84128 2.762155e-07 1.750

15 524.02860 6.182665e-07 1.875

16 611.40396 6.643946e-04 2.000

17 616.62297 7.362916e-01 2.125

18 634.98390 1.717996e+00 2.250

19 662.37733 3.092344e+00 2.375

20 694.87755 5.153758e+00 2.500

21 741.92078 8.589062e+00 2.625

22 799.43676 1.545756e+01 2.750

23 867.39853 3.603308e+01 2.875

24 942.97404 1.151864e+03 3.000

25 946.23548 3.681964e+04 3.125

26 949.33386 8.582348e+04 3.250

27 955.90253 1.544348e+05 3.375

28 964.03468 2.573141e+05 3.500

29 973.73298 4.286244e+05 3.625

30 984.99979 7.703843e+05 3.750

31 997.81842 1.783600e+06 3.875

32 1010.78728 2.001657e+07 4.000

33 1012.16892 2.246123e+08 4.125

34 1012.23283 5.199270e+08 4.250

35 1012.24831 9.341967e+08 4.375

36 1012.25508 1.555265e+09 4.500

37 1012.26255 2.588153e+09 4.625

38 1012.27763 4.641076e+09 4.750

39 1012.32214 1.062368e+10 4.875

40 1012.83817 7.624894e+10 5.000

41 1018.54240 5.472829e+11 5.125

42 1030.33840 1.252858e+12 5.250

43 1047.92954 2.246916e+12 5.375

44 1071.29714 3.740036e+12 5.500

45 1100.43720 6.229664e+12 5.625

46 1135.37352 1.120975e+13 5.750

47 1181.88392 2.615094e+13 5.875

48 1237.17669 Inf 6.000

> names(rxrobj)

[1] "data" "form" "p" "n" "r2" "s2"

[7] "prinstat" "crlqstat" "qmse" "qp" "coef" "rmse"

[13] "exev" "infd" "spat" "mlik" "sext"

> plot(rxrobj)

>

>

>

>

>

> dev.off()

null device

1

>

|