Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

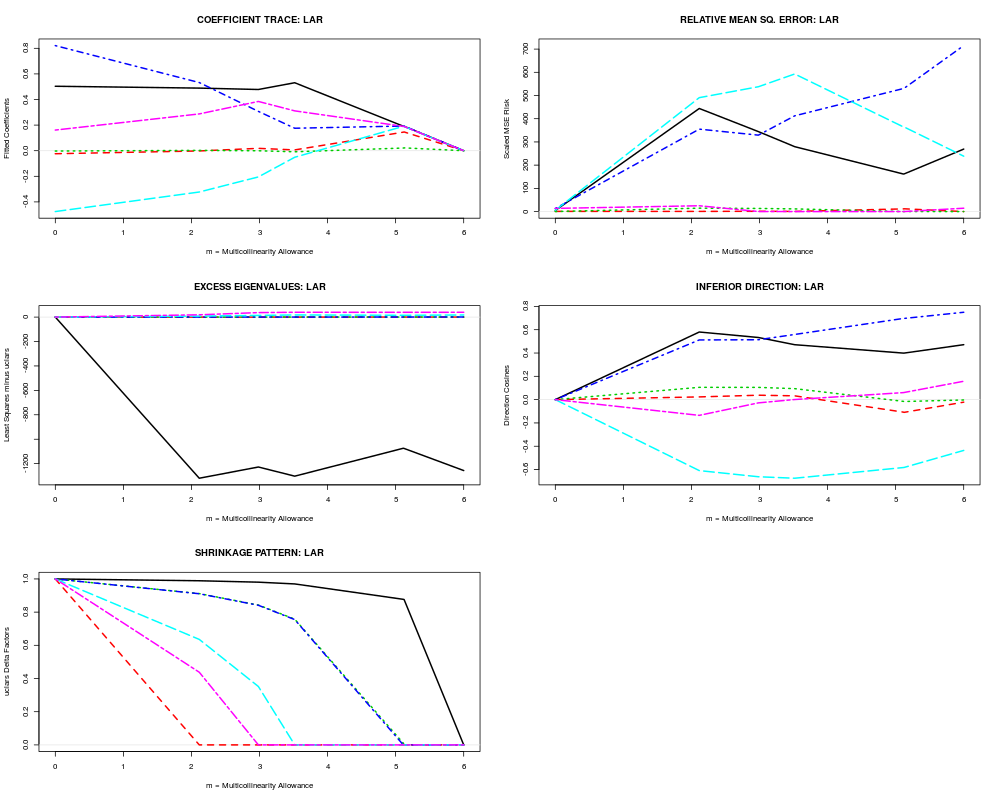

Maximum Likelihood Least Angle Regression on Uncorrelated X-ComponentsDescriptionApply least angle regression estimation to the uncorrelated components of a possibly ill-conditioned linear regression model and generate normal-theory maximum likelihood TRACE displays. Usage

RXuclars(form, data, rscale = 1, type = "lar", trace = FALSE,

eps = .Machine$double.eps, omdmin = 9.9e-13, ...)

Arguments

DetailsRXuclars() applies Least Angle Regression to the uncorrelated components of a possibly ill-conditioned set of X-variables. A closed-form expression for the lars/lasso shrinkage delta factors exits in this case: Delta(i) = max(0,1-k/abs[PC(i)]), where PC(i) is the principal correlation between Y and the i-th principal coordinates of X. Note that the k-factor in this formulation is limited to a subset of [0,1]. MCAL=0 occurs at k=0, while MCAL = P results when k is the maximum absolute principal correlation. ValueAn output list object of class RXuclars:

Author(s)Bob Obenchain <wizbob@att.net> ReferencesEfron B, Hastie T, Johnstone I, Tibshirani R. (2004) Least angle regression. Ann. Statis. 32, 407-499 (with discussion.) Obenchain RL. (1994-2005) Shrinkage Regression: ridge, BLUP, Bayes, spline and Stein. members.iquest.net/~softrx. Obenchain RL. (2011) shrink.PDF Vignette-like documentation stored in the R library/RXshrink/doc folder. 23 pages. See Also

Examplesdata(longley2) form <- GNP~GNP.deflator+Unemployed+Armed.Forces+Population+Year+Employed rxuobj <- RXuclars(form, data=longley2) rxuobj plot(rxuobj) Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(RXshrink)

Loading required package: lars

Loaded lars 1.2

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/RXshrink/RXuclars.Rd_%03d_medium.png", width=480, height=480)

> ### Name: RXuclars

> ### Title: Maximum Likelihood Least Angle Regression on Uncorrelated

> ### X-Components

> ### Aliases: RXuclars

> ### Keywords: regression hplot

>

> ### ** Examples

>

> data(longley2)

> form <- GNP~GNP.deflator+Unemployed+Armed.Forces+Population+Year+Employed

> rxuobj <- RXuclars(form, data=longley2)

> rxuobj

RXuclars Object: Uncorrelated Component LARS Shrinkage

Data Frame: longley2

Regression Equation:

GNP ~ GNP.deflator + Unemployed + Armed.Forces + Population +

Year + Employed

Number of Regressor Variables, p = 6

Number of Observations, n = 29

Principal Axis Summary Statistics of Ill-Conditioning...

LAMBDA SV COMP RHO TRAT

1 124.55432117 11.1603907 0.466590166 0.98409260 179.451944

2 34.04395492 5.8347198 -0.009779055 -0.01078296 -1.966301

3 7.97601572 2.8241841 0.228918857 0.12217872 22.279619

4 1.31429584 1.1464274 -0.557948473 -0.12088200 -22.043160

5 0.06505309 0.2550551 0.613987118 0.02959472 5.396677

6 0.04635925 0.2153120 -0.471410409 -0.01918176 -3.497845

Residual Mean Square for Error = 0.0008420418

Estimate of Residual Std. Error = 0.02901796

The extent of shrinkage (M value) most likely to be optimal

depends upon whether one uses the Classical, Empirical Bayes, or

Random Coefficient criterion. In each case, the objective is to

minimize the minus-two-log-likelihood statistics listed below:

M CLIK EBAY RCOF

0 0.000000 Inf Inf Inf

1 2.114916 149.4278 472.3079 100.5459

2 2.983319 157.4982 825.7711 113.6821

3 3.517121 164.6308 1259.1945 124.0563

4 5.112223 187.2225 4980.0349 159.4655

5 5.124154 187.5178 5027.7148 159.7195

6 6.000000 212.3044 33230.5079 212.3044

Extent of shrinkage statistics...

TSMSE MCAL

0 37.86637 0.000000

1 1330.28575 2.114916

2 1226.23804 2.983319

3 1296.89147 3.517121

4 1068.18888 5.112223

5 1069.64994 5.124154

6 1237.17669 6.000000

Output from LARS invocation...

Call:

lars(x = sx$u, y = cry, type = type, trace = trace, normalize = eps)

R-squared: 0.999

Sequence of LAR moves:

Var 1 3 4 5 6 2

Step 1 2 3 4 5 6

> plot(rxuobj)

>

>

>

>

>

> dev.off()

null device

1

>

|