Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

test for optimal Sharpe ratioDescriptionPerforms one sample tests of Sharpe ratio of the Markowitz portfolio. Usage

sropt_test(X,alternative=c("greater","two.sided","less"),

zeta.s=0,ope=1,conf.level=0.95)

Arguments

DetailsSuppose xi are n independent draws of a q-variate normal random variable with mean mu and covariance matrix Sigma. This code tests the hypothesis H0: mu' Sigma^-1 mu = delta_0^2 The default alternative hypothesis is the one-sided H1: mu' Sigma^-1 mu > delta_0^2 but this can be set otherwise. Note there is no 'drag' term here since this represents a linear offset of the population parameter. ValueA list with class

Author(s)Steven E. Pav shabbychef@gmail.com See Also

Other sropt: Examples

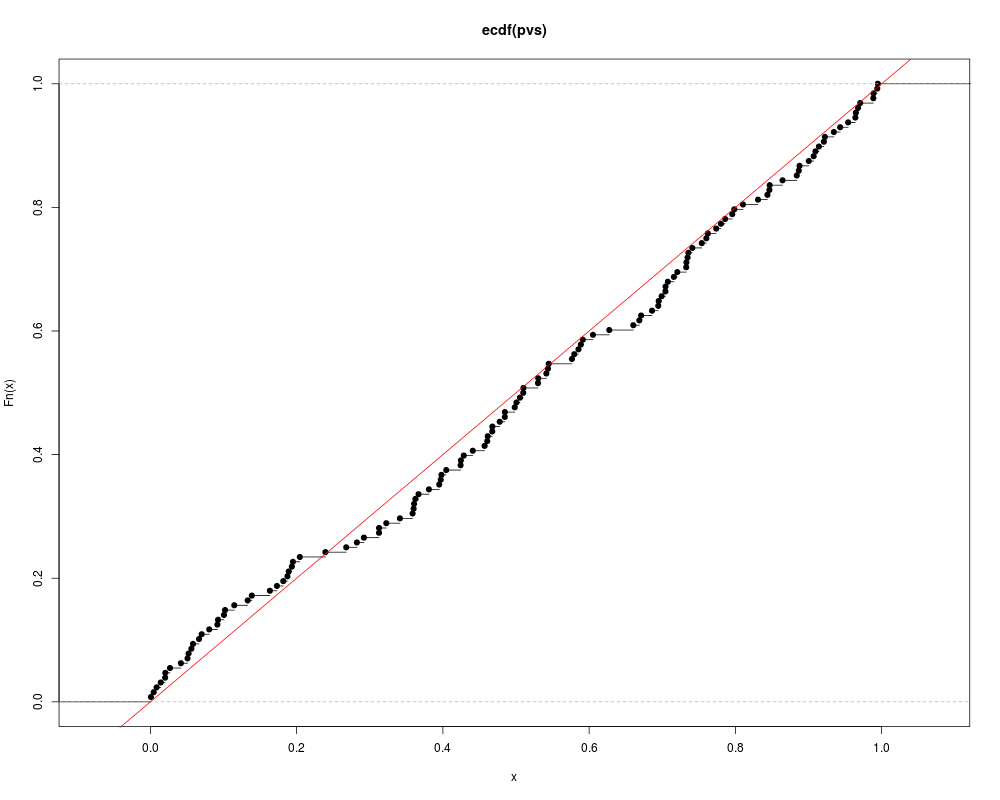

# test for uniformity

pvs <- replicate(128,{ x <- sropt_test(matrix(rnorm(1000*4),ncol=4),alternative="two.sided")

x$p.value })

plot(ecdf(pvs))

abline(0,1,col='red')

# input a sropt objects:

nfac <- 5

nyr <- 10

ope <- 253

# simulations with no covariance structure.

# under the null:

set.seed(as.integer(charToRaw("be determinstic")))

Returns <- matrix(rnorm(ope*nyr*nfac,mean=0,sd=0.0125),ncol=nfac)

asro <- as.sropt(Returns,drag=0,ope=ope)

stest <- sropt_test(asro,alternative="two.sided")

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(SharpeR)

Attaching package: 'SharpeR'

The following object is masked from 'package:base':

summary

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/SharpeR/sropt_test.Rd_%03d_medium.png", width=480, height=480)

> ### Name: sropt_test

> ### Title: test for optimal Sharpe ratio

> ### Aliases: sropt_test

> ### Keywords: htest

>

> ### ** Examples

>

>

> # test for uniformity

> pvs <- replicate(128,{ x <- sropt_test(matrix(rnorm(1000*4),ncol=4),alternative="two.sided")

+ x$p.value })

> plot(ecdf(pvs))

> abline(0,1,col='red')

>

> # input a sropt objects:

> nfac <- 5

> nyr <- 10

> ope <- 253

> # simulations with no covariance structure.

> # under the null:

> set.seed(as.integer(charToRaw("be determinstic")))

> Returns <- matrix(rnorm(ope*nyr*nfac,mean=0,sd=0.0125),ncol=nfac)

> asro <- as.sropt(Returns,drag=0,ope=ope)

> stest <- sropt_test(asro,alternative="two.sided")

>

>

>

>

>

>

> dev.off()

null device

1

>

|