Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

Random Number Generators for 2-Dim SDEDescriptionThe (S3) generic function Usage

rsde2d(N, ...)

## Default S3 method:

rsde2d(N = 1000, M = 100, x0 = 0, y0 = 0, t0 = 0, T = 1, Dt, tau = 0.5,

driftx, diffx, drifty, diffy, alpha = 0.5, mu = 0.5, type = c("ito", "str"),

method = c("euler", "milstein", "predcorr", "smilstein", "taylor",

"heun", "rk1", "rk2", "rk3"), ...)

## S3 method for class 'rsde2d'

summary(object, ...)

## S3 method for class 'rsde2d'

mean(x, ...)

## S3 method for class 'rsde2d'

median(x, ...)

## S3 method for class 'rsde2d'

quantile(x, ...)

## S3 method for class 'rsde2d'

kurtosis(x, ...)

## S3 method for class 'rsde2d'

skewness(x, ...)

## S3 method for class 'rsde2d'

moment(x, order = 2, ...)

## S3 method for class 'rsde2d'

bconfint(x, level=0.95, ...)

## S3 method for class 'rsde2d'

plot(x, ...)

Arguments

DetailsThe function x(tau)={t>=0; x = X(tau)} y(tau)={t>=0; y = Y(tau)} with tau is a fixed time between Value

Author(s)A.C. Guidoum, K. Boukhetala. See Also

Examples

## Example 1:

## random numbers of two standard Brownian motion W1(t) and W2(t) at time = 1

set.seed(1234)

fx <- expression(0)

gx <- expression(1)

fy <- expression(0)

gy <- expression(1)

res1 <- rsde2d(driftx=fx,diffx=gx,drifty=fy,diffy=gy,tau=1)

res1

summary(res1)

X <- cbind(res1$x,res1$y)

## library(sm)

## sm.density(X,display="persp")

## Example 2:

## dX(t) = 5*(-1-Y(t))*X(t) * dt + 0.5 * dW1(t)

## dY(t) = 5*(-1-X(t))*Y(t) * dt + 0.5 * dW2(t)

## W1(t) and W2(t) two independent Brownian motion

set.seed(1234)

fx <- expression(5*(-1-y)*x)

gx <- expression(0.5)

fy <- expression(5*(-1-x)*y)

gy <- expression(0.5)

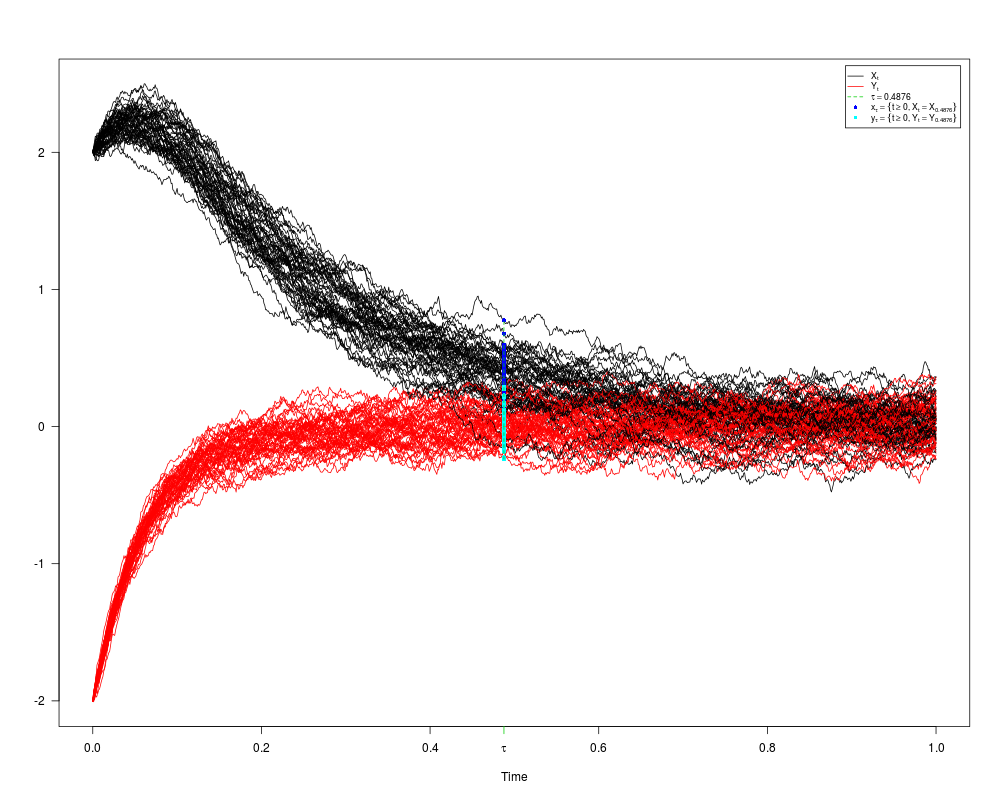

res2 <- rsde2d(driftx=fx,diffx=gx,drifty=fy,diffy=gy,tau=0.4876

,x0=2,y0=-2,M=50)

res2

summary(res2)

plot(res2,union=TRUE)

dev.new()

plot(res2,union=FALSE)

X <- cbind(res2$x,res2$y)

## sm.density(X,display="persp")

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(Sim.DiffProc)

Package 'Sim.DiffProc' version 3.2 loaded.

help(Sim.DiffProc) for summary information.

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/Sim.DiffProc/rsde2d.Rd_%03d_medium.png", width=480, height=480)

> ### Name: rsde2d

> ### Title: Random Number Generators for 2-Dim SDE

> ### Aliases: rsde2d rsde2d.default summary.rsde2d mean.rsde2d median.rsde2d

> ### quantile.rsde2d kurtosis.rsde2d skewness.rsde2d moment.rsde2d

> ### bconfint.rsde2d plot.rsde2d

> ### Keywords: sde ts mts random generators

>

> ### ** Examples

>

>

> ## Example 1:

> ## random numbers of two standard Brownian motion W1(t) and W2(t) at time = 1

> set.seed(1234)

>

> fx <- expression(0)

> gx <- expression(1)

> fy <- expression(0)

> gy <- expression(1)

> res1 <- rsde2d(driftx=fx,diffx=gx,drifty=fy,diffy=gy,tau=1)

> res1

$SDE

Ito Sde 2D:

| dX(t) = 0 * dt + 1 * dW1(t)

| dY(t) = 0 * dt + 1 * dW2(t)

Method:

| Euler scheme of order 0.5

Summary:

| Size of process | N = 1000.

| Number of simulation | M = 100.

| Initial values | (x0,y0) = (0,0).

| Time of process | t in [0,1].

| Discretization | Dt = 0.001.

$tau

[1] 1

$x

[1] -0.752480843 1.702508137 -0.886742315 1.102104818 -0.072030515

[6] 0.690516597 1.250107590 0.336372924 1.890800159 0.109238964

[11] 0.099397754 -0.637768773 -1.347715323 -2.440436791 0.909373295

[16] 0.836954108 0.526877871 0.284616553 2.733666268 1.192575060

[21] -1.665951693 -1.324730493 -0.365312965 0.006597265 0.904601706

[26] 0.402344080 -0.951783158 0.607011758 0.577166109 -1.688961042

[31] -1.217521278 1.871545948 -0.521119439 1.325818238 0.285569020

[36] 0.421780885 1.994326282 -1.050162417 0.552445149 0.206196169

[41] -1.070028554 -0.315776716 0.756446587 -0.369655616 0.629929557

[46] -0.311790467 -0.857326695 -0.570031127 0.192493894 -1.039283215

[51] 0.544427675 -0.528700758 -0.810824784 -1.347182044 0.466129652

[56] 0.528125966 1.773809511 -0.463832732 0.432883872 1.442536907

[61] 0.910333558 -0.421111647 0.434936145 1.468225095 0.554064864

[66] -0.061054415 0.354880902 -0.255413407 0.544084923 -0.744957932

[71] 0.446529741 2.333070081 -1.029377983 0.121452880 -0.114991379

[76] 0.503900038 1.098777909 -0.530587598 -0.024000252 -0.608981619

[81] 0.140523756 0.499919675 1.572362867 2.356740424 -0.235453842

[86] 0.177443346 0.414325908 -0.883922171 -0.319481616 0.167257016

[91] 0.255289435 -0.336055142 1.469777758 0.429926441 0.122399389

[96] 0.819122320 0.295999038 -0.949693068 -0.491286273 2.152657224

$y

[1] 0.50667148 -0.96360037 -0.32068759 -1.02845604 0.11419805 0.79195738

[7] 0.80923953 0.84248818 -0.34221365 0.43938815 0.36861426 -0.49791714

[13] -1.58097598 -1.41807390 -0.09193726 1.50024399 -0.91115708 -0.19324185

[19] 1.26212073 -1.12776770 0.26550537 0.75268083 -0.73995138 1.28352488

[25] -0.29790765 0.66369237 -0.08150428 -0.02660853 -1.60906884 0.89637653

[31] 0.20016235 -0.01808949 -0.21559015 0.74908918 -0.59886326 -0.03648556

[37] -0.82987985 1.64760794 1.01975432 0.33085089 -2.30629103 1.13496302

[43] -1.06537708 -0.27594047 -1.07943124 -0.29387762 2.01770803 0.53843675

[49] 0.73067729 0.50170097 -0.20272859 0.74783627 1.22412106 0.88100868

[55] 1.37145009 -0.42355719 -0.74806384 -0.68381214 0.24044379 -0.98884966

[61] -1.27127987 -0.66405976 -0.14360769 0.02681467 0.56160040 1.58960893

[67] -0.30683514 -0.57384290 -0.33813803 -0.04289656 0.16139669 0.04550287

[73] -0.12226641 -0.91142192 -0.71865725 -0.08089410 1.24669966 0.10357728

[79] -0.64647203 0.07614455 -0.72978126 0.12103374 0.32459263 1.57242143

[85] -0.31042552 -1.73227711 0.13327040 -0.29184858 0.87328694 -1.12755055

[91] -1.24015472 0.68576181 -0.21097617 1.09578779 0.22431963 -0.29951479

[97] 0.59530819 -0.79143416 -0.69461776 0.76865006

attr(,"class")

[1] "rsde2d"

> summary(res1)

Monte-Carlo Statistics for X(t) and Y(t) at t = 1

x y

Mean 0.196178 -0.002086

Variance 0.959849 0.724598

Median 0.230743 -0.039691

First quartile -0.498745 -0.650869

Third quartile 0.645076 0.669210

Skewness 0.166416 -0.012700

Kurtosis 2.942410 2.620024

Moment of order 2 0.950251 0.717352

Moment of order 3 0.156495 -0.007833

Moment of order 4 2.710874 1.375625

Moment of order 5 0.800026 -0.258054

Bound conf Inf (95%) -1.514789 -1.595725

Bound conf Sup (95%) 2.247374 1.581445

> X <- cbind(res1$x,res1$y)

> ## library(sm)

> ## sm.density(X,display="persp")

>

> ## Example 2:

> ## dX(t) = 5*(-1-Y(t))*X(t) * dt + 0.5 * dW1(t)

> ## dY(t) = 5*(-1-X(t))*Y(t) * dt + 0.5 * dW2(t)

> ## W1(t) and W2(t) two independent Brownian motion

> set.seed(1234)

>

> fx <- expression(5*(-1-y)*x)

> gx <- expression(0.5)

> fy <- expression(5*(-1-x)*y)

> gy <- expression(0.5)

> res2 <- rsde2d(driftx=fx,diffx=gx,drifty=fy,diffy=gy,tau=0.4876

+ ,x0=2,y0=-2,M=50)

> res2

$SDE

Ito Sde 2D:

| dX(t) = 5 * (-1 - Y(t)) * X(t) * dt + 0.5 * dW1(t)

| dY(t) = 5 * (-1 - X(t)) * Y(t) * dt + 0.5 * dW2(t)

Method:

| Euler scheme of order 0.5

Summary:

| Size of process | N = 1000.

| Number of simulation | M = 50.

| Initial values | (x0,y0) = (2,-2).

| Time of process | t in [0,1].

| Discretization | Dt = 0.001.

$tau

[1] 0.4876

$x

[1] 0.37045552 0.52300479 0.08369982 0.28796583 0.25915916 0.23919130

[7] 0.34059663 0.77575169 0.32267635 0.50306037 0.59706326 0.57773318

[13] 0.54614539 0.59442533 0.18566895 0.40655062 0.41854655 0.24183743

[19] 0.56001159 0.25042614 0.14825070 0.54434343 0.31354847 0.53183272

[25] 0.37875266 0.15298765 0.09969632 0.48721758 0.38654370 0.18791596

[31] -0.07168162 0.22393001 0.42480426 0.33881001 0.16476811 0.19151850

[37] 0.67748695 0.16934174 0.47200220 0.39271166 0.44638779 0.25307664

[43] 0.27497295 0.45441872 0.49790286 0.41883353 0.45537985 -0.13282119

[49] 0.21242166 0.46013589

$y

[1] 0.08576661 -0.07231530 -0.07169320 -0.04497045 0.22615801 -0.06443680

[7] -0.10454925 -0.11699850 0.08153500 -0.12291282 -0.09796212 -0.10531677

[13] 0.03880450 -0.14027926 0.07586430 0.12449890 -0.03415597 -0.15423662

[19] -0.05868709 0.11265533 0.12442072 0.05346850 -0.02095579 0.05879950

[25] -0.17410546 0.15276767 0.03557542 0.04474690 -0.23673402 0.05061763

[31] -0.01266982 0.29053100 0.21046903 -0.01561020 -0.04888774 0.05779271

[37] 0.03093737 0.03127232 0.05133502 0.01186592 -0.18423635 0.17584998

[43] -0.08324319 -0.03013000 -0.07323272 -0.22485228 -0.05276285 0.27190322

[49] 0.15889527 -0.06292103

attr(,"class")

[1] "rsde2d"

> summary(res2)

Monte-Carlo Statistics for X(t) and Y(t) at t = 0.4876

x y

Mean 0.352789 0.002954

Variance 0.033810 0.015042

Median 0.374604 -0.014140

First quartile 0.227745 -0.073003

Third quartile 0.483414 0.071598

Skewness -0.260806 0.301220

Kurtosis 2.935137 2.601741

Moment of order 2 0.033133 0.014741

Moment of order 3 -0.001621 0.000556

Moment of order 4 0.003355 0.000589

Moment of order 5 -0.000479 0.000053

Bound conf Inf (95%) -0.036721 -0.215714

Bound conf Sup (95%) 0.659392 0.261611

> plot(res2,union=TRUE)

> dev.new()

Error in dev.new() : no suitable unused file name for pdf()

Execution halted

|