Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

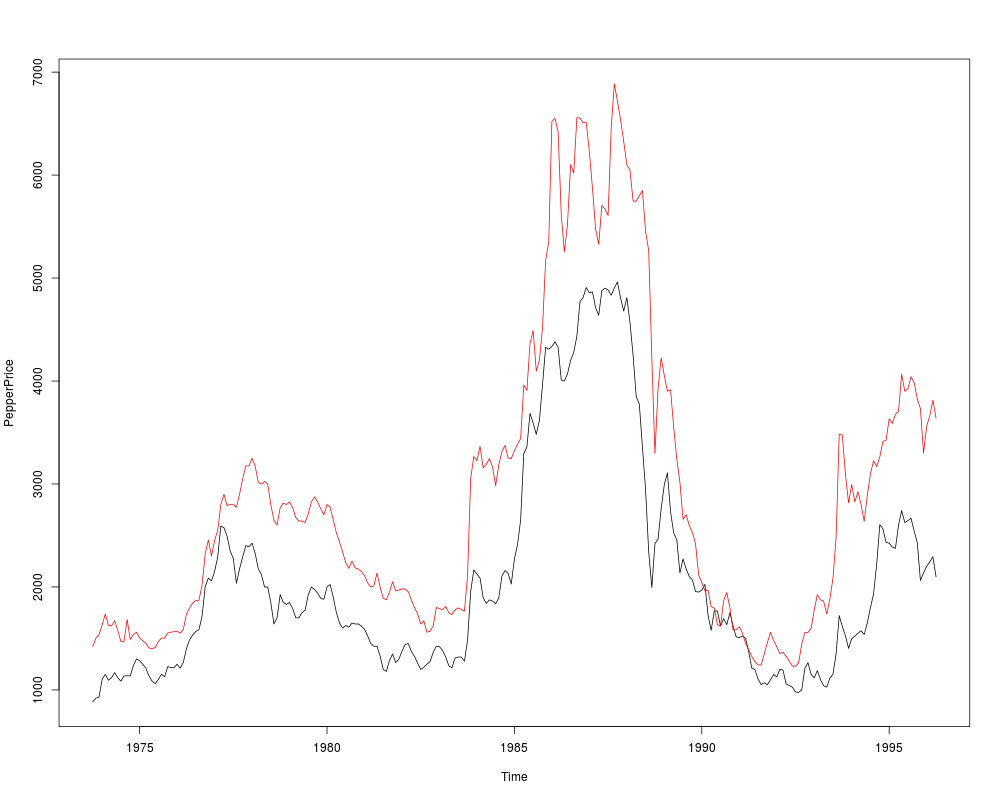

Black and White Pepper PricesDescriptionTime series of average monthly European spot prices for black and white pepper (fair average quality) in US dollars per ton. Usagedata("PepperPrice")

FormatA monthly multiple time series from 1973(10) to 1996(4) with 2 variables.

SourceOnline complements to Franses (1998). http://www.few.eur.nl/few/people/franses/research/book2.htm ReferencesFranses, P.H. (1998). Time Series Models for Business and Economic Forecasting. Cambridge, UK: Cambridge University Press. Examples

## data

data("PepperPrice")

plot(PepperPrice, plot.type = "single", col = 1:2)

## package

library("tseries")

library("urca")

## unit root tests

adf.test(log(PepperPrice[, "white"]))

adf.test(diff(log(PepperPrice[, "white"])))

pp.test(log(PepperPrice[, "white"]), type = "Z(t_alpha)")

pepper_ers <- ur.ers(log(PepperPrice[, "white"]),

type = "DF-GLS", model = "const", lag.max = 4)

summary(pepper_ers)

## stationarity tests

kpss.test(log(PepperPrice[, "white"]))

## cointegration

po.test(log(PepperPrice))

pepper_jo <- ca.jo(log(PepperPrice), ecdet = "const", type = "trace")

summary(pepper_jo)

pepper_jo2 <- ca.jo(log(PepperPrice), ecdet = "const", type = "eigen")

summary(pepper_jo2)

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(AER)

Loading required package: car

Loading required package: lmtest

Loading required package: zoo

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numeric

Loading required package: sandwich

Loading required package: survival

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/AER/PepperPrice.Rd_%03d_medium.png", width=480, height=480)

> ### Name: PepperPrice

> ### Title: Black and White Pepper Prices

> ### Aliases: PepperPrice

> ### Keywords: datasets

>

> ### ** Examples

>

> ## data

> data("PepperPrice")

> plot(PepperPrice, plot.type = "single", col = 1:2)

>

> ## package

> library("tseries")

> library("urca")

>

> ## unit root tests

> adf.test(log(PepperPrice[, "white"]))

Augmented Dickey-Fuller Test

data: log(PepperPrice[, "white"])

Dickey-Fuller = -1.744, Lag order = 6, p-value = 0.6838

alternative hypothesis: stationary

> adf.test(diff(log(PepperPrice[, "white"])))

Augmented Dickey-Fuller Test

data: diff(log(PepperPrice[, "white"]))

Dickey-Fuller = -5.336, Lag order = 6, p-value = 0.01

alternative hypothesis: stationary

Warning message:

In adf.test(diff(log(PepperPrice[, "white"]))) :

p-value smaller than printed p-value

> pp.test(log(PepperPrice[, "white"]), type = "Z(t_alpha)")

Phillips-Perron Unit Root Test

data: log(PepperPrice[, "white"])

Dickey-Fuller Z(t_alpha) = -1.6439, Truncation lag parameter = 5,

p-value = 0.726

alternative hypothesis: stationary

> pepper_ers <- ur.ers(log(PepperPrice[, "white"]),

+ type = "DF-GLS", model = "const", lag.max = 4)

> summary(pepper_ers)

###############################################

# Elliot, Rothenberg and Stock Unit Root Test #

###############################################

Test of type DF-GLS

detrending of series with intercept

Call:

lm(formula = dfgls.form, data = data.dfgls)

Residuals:

Min 1Q Median 3Q Max

-0.21135 -0.03069 -0.00108 0.03030 0.31018

Coefficients:

Estimate Std. Error t value Pr(>|t|)

yd.lag -0.004022 0.006015 -0.669 0.504

yd.diff.lag1 0.336267 0.061986 5.425 1.32e-07 ***

yd.diff.lag2 -0.105024 0.065414 -1.606 0.110

yd.diff.lag3 0.001263 0.065366 0.019 0.985

yd.diff.lag4 0.011251 0.062085 0.181 0.856

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.06481 on 261 degrees of freedom

Multiple R-squared: 0.1028, Adjusted R-squared: 0.0856

F-statistic: 5.98 on 5 and 261 DF, p-value: 2.947e-05

Value of test-statistic is: -0.6686

Critical values of DF-GLS are:

1pct 5pct 10pct

critical values -2.57 -1.94 -1.62

>

> ## stationarity tests

> kpss.test(log(PepperPrice[, "white"]))

KPSS Test for Level Stationarity

data: log(PepperPrice[, "white"])

KPSS Level = 0.91295, Truncation lag parameter = 3, p-value = 0.01

Warning message:

In kpss.test(log(PepperPrice[, "white"])) :

p-value smaller than printed p-value

>

> ## cointegration

> po.test(log(PepperPrice))

Phillips-Ouliaris Cointegration Test

data: log(PepperPrice)

Phillips-Ouliaris demeaned = -24.099, Truncation lag parameter = 2,

p-value = 0.02404

> pepper_jo <- ca.jo(log(PepperPrice), ecdet = "const", type = "trace")

> summary(pepper_jo)

######################

# Johansen-Procedure #

######################

Test type: trace statistic , without linear trend and constant in cointegration

Eigenvalues (lambda):

[1] 4.931953e-02 1.350807e-02 2.081668e-17

Values of teststatistic and critical values of test:

test 10pct 5pct 1pct

r <= 1 | 3.66 7.52 9.24 12.97

r = 0 | 17.26 17.85 19.96 24.60

Eigenvectors, normalised to first column:

(These are the cointegration relations)

black.l2 white.l2 constant

black.l2 1.0000000 1.00000 1.000000

white.l2 -0.8892307 -5.09942 2.280911

constant -0.5569943 33.02742 -20.032441

Weights W:

(This is the loading matrix)

black.l2 white.l2 constant

black.d -0.07472300 0.002453210 -4.958157e-18

white.d 0.02015611 0.003537005 8.850353e-18

> pepper_jo2 <- ca.jo(log(PepperPrice), ecdet = "const", type = "eigen")

> summary(pepper_jo2)

######################

# Johansen-Procedure #

######################

Test type: maximal eigenvalue statistic (lambda max) , without linear trend and constant in cointegration

Eigenvalues (lambda):

[1] 4.931953e-02 1.350807e-02 2.081668e-17

Values of teststatistic and critical values of test:

test 10pct 5pct 1pct

r <= 1 | 3.66 7.52 9.24 12.97

r = 0 | 13.61 13.75 15.67 20.20

Eigenvectors, normalised to first column:

(These are the cointegration relations)

black.l2 white.l2 constant

black.l2 1.0000000 1.00000 1.000000

white.l2 -0.8892307 -5.09942 2.280911

constant -0.5569943 33.02742 -20.032441

Weights W:

(This is the loading matrix)

black.l2 white.l2 constant

black.d -0.07472300 0.002453210 -4.958157e-18

white.d 0.02015611 0.003537005 8.850353e-18

>

>

>

>

>

> dev.off()

null device

1

>

|

Created & Maintained by Osamu Ogasawara (osamu.ogasawara@gmail.com) and