Supported by Dr. Osamu Ogasawara and  . . |

|

Last data update: 2014.03.03 |

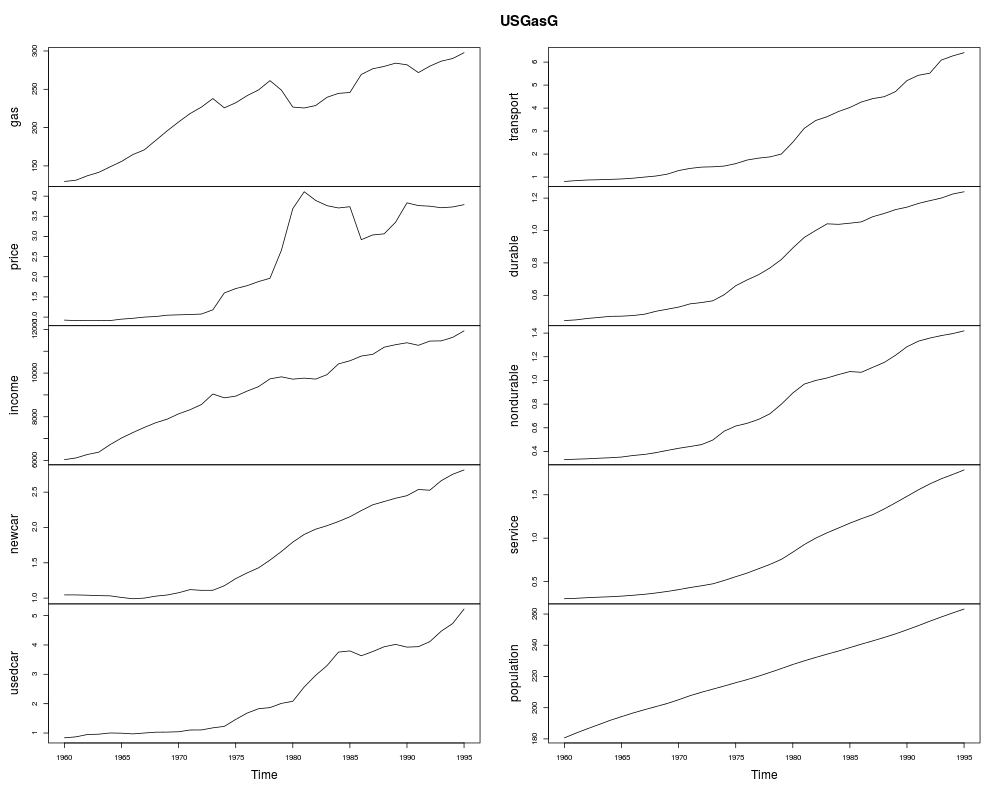

US Gasoline Market Data (1960–1995, Greene)DescriptionTime series data on the US gasoline market. Usagedata("USGasG")

FormatAn annual multiple time series from 1960 to 1995 with 10 variables.

SourceOnline complements to Greene (2003). Table F2.2. http://pages.stern.nyu.edu/~wgreene/Text/tables/tablelist5.htm ReferencesGreene, W.H. (2003). Econometric Analysis, 5th edition. Upper Saddle River, NJ: Prentice Hall. See Also

Examples

data("USGasG", package = "AER")

plot(USGasG)

## Greene (2003)

## Example 2.3

fm <- lm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

data = as.data.frame(USGasG))

summary(fm)

## Example 4.4

## estimates and standard errors (note different offset for intercept)

coef(fm)

sqrt(diag(vcov(fm)))

## confidence interval

confint(fm, parm = "log(income)")

## test linear hypothesis

linearHypothesis(fm, "log(income) = 1")

## Example 7.6

## re-used in Example 8.3

trend <- 1:nrow(USGasG)

shock <- factor(time(USGasG) > 1973, levels = c(FALSE, TRUE),

labels = c("before", "after"))

## 1960-1995

fm1 <- lm(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = as.data.frame(USGasG))

summary(fm1)

## pooled

fm2 <- lm(log(gas/population) ~ shock + log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = as.data.frame(USGasG))

summary(fm2)

## segmented

fm3 <- lm(log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

log(usedcar) + trend), data = as.data.frame(USGasG))

summary(fm3)

## Chow test

anova(fm3, fm1)

library("strucchange")

sctest(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = USGasG, point = c(1973, 1), type = "Chow")

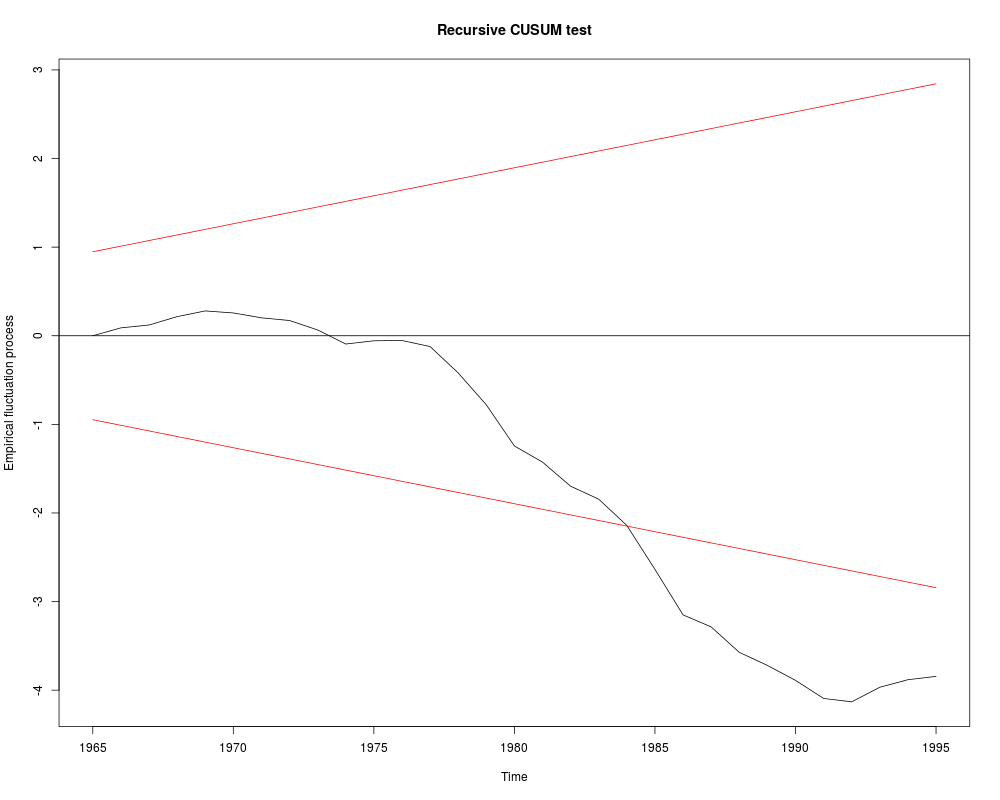

## Recursive CUSUM test

rcus <- efp(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = USGasG, type = "Rec-CUSUM")

plot(rcus)

sctest(rcus)

## Note: Greene's remark that the break is in 1984 (where the process crosses its

## boundary) is wrong. The break appears to be no later than 1976.

## More examples can be found in:

## help("Greene2003")

Results

R version 3.3.1 (2016-06-21) -- "Bug in Your Hair"

Copyright (C) 2016 The R Foundation for Statistical Computing

Platform: x86_64-pc-linux-gnu (64-bit)

R is free software and comes with ABSOLUTELY NO WARRANTY.

You are welcome to redistribute it under certain conditions.

Type 'license()' or 'licence()' for distribution details.

R is a collaborative project with many contributors.

Type 'contributors()' for more information and

'citation()' on how to cite R or R packages in publications.

Type 'demo()' for some demos, 'help()' for on-line help, or

'help.start()' for an HTML browser interface to help.

Type 'q()' to quit R.

> library(AER)

Loading required package: car

Loading required package: lmtest

Loading required package: zoo

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numeric

Loading required package: sandwich

Loading required package: survival

> png(filename="/home/ddbj/snapshot/RGM3/R_CC/result/AER/USGasG.Rd_%03d_medium.png", width=480, height=480)

> ### Name: USGasG

> ### Title: US Gasoline Market Data (1960-1995, Greene)

> ### Aliases: USGasG

> ### Keywords: datasets

>

> ### ** Examples

>

> data("USGasG", package = "AER")

> plot(USGasG)

>

> ## Greene (2003)

> ## Example 2.3

> fm <- lm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

+ data = as.data.frame(USGasG))

> summary(fm)

Call:

lm(formula = log(gas/population) ~ log(price) + log(income) +

log(newcar) + log(usedcar), data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.065042 -0.018842 0.001528 0.020786 0.058084

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -12.34184 0.67489 -18.287 <2e-16 ***

log(price) -0.05910 0.03248 -1.819 0.0786 .

log(income) 1.37340 0.07563 18.160 <2e-16 ***

log(newcar) -0.12680 0.12699 -0.998 0.3258

log(usedcar) -0.11871 0.08134 -1.459 0.1545

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.03304 on 31 degrees of freedom

Multiple R-squared: 0.958, Adjusted R-squared: 0.9526

F-statistic: 176.7 on 4 and 31 DF, p-value: < 2.2e-16

>

> ## Example 4.4

> ## estimates and standard errors (note different offset for intercept)

> coef(fm)

(Intercept) log(price) log(income) log(newcar) log(usedcar)

-12.34184054 -0.05909513 1.37339912 -0.12679667 -0.11870847

> sqrt(diag(vcov(fm)))

(Intercept) log(price) log(income) log(newcar) log(usedcar)

0.67489471 0.03248496 0.07562767 0.12699351 0.08133710

> ## confidence interval

> confint(fm, parm = "log(income)")

2.5 % 97.5 %

log(income) 1.219155 1.527643

> ## test linear hypothesis

> linearHypothesis(fm, "log(income) = 1")

Linear hypothesis test

Hypothesis:

log(income) = 1

Model 1: restricted model

Model 2: log(gas/population) ~ log(price) + log(income) + log(newcar) +

log(usedcar)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 32 0.060445

2 31 0.033837 1 0.026608 24.377 2.57e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

>

> ## Example 7.6

> ## re-used in Example 8.3

> trend <- 1:nrow(USGasG)

> shock <- factor(time(USGasG) > 1973, levels = c(FALSE, TRUE),

+ labels = c("before", "after"))

>

> ## 1960-1995

> fm1 <- lm(log(gas/population) ~ log(income) + log(price) + log(newcar) +

+ log(usedcar) + trend, data = as.data.frame(USGasG))

> summary(fm1)

Call:

lm(formula = log(gas/population) ~ log(income) + log(price) +

log(newcar) + log(usedcar) + trend, data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.055238 -0.017715 0.003659 0.016481 0.053522

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -17.385790 1.679289 -10.353 2.03e-11 ***

log(income) 1.954626 0.192854 10.135 3.34e-11 ***

log(price) -0.115530 0.033479 -3.451 0.00168 **

log(newcar) 0.205282 0.152019 1.350 0.18700

log(usedcar) -0.129274 0.071412 -1.810 0.08028 .

trend -0.019118 0.005957 -3.210 0.00316 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.02898 on 30 degrees of freedom

Multiple R-squared: 0.9687, Adjusted R-squared: 0.9635

F-statistic: 185.8 on 5 and 30 DF, p-value: < 2.2e-16

> ## pooled

> fm2 <- lm(log(gas/population) ~ shock + log(income) + log(price) + log(newcar) +

+ log(usedcar) + trend, data = as.data.frame(USGasG))

> summary(fm2)

Call:

lm(formula = log(gas/population) ~ shock + log(income) + log(price) +

log(newcar) + log(usedcar) + trend, data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.045360 -0.019697 0.003931 0.015112 0.047550

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -16.374402 1.456263 -11.244 4.33e-12 ***

shockafter 0.077311 0.021872 3.535 0.00139 **

log(income) 1.838167 0.167258 10.990 7.43e-12 ***

log(price) -0.178005 0.033508 -5.312 1.06e-05 ***

log(newcar) 0.209842 0.129267 1.623 0.11534

log(usedcar) -0.128132 0.060721 -2.110 0.04359 *

trend -0.016862 0.005105 -3.303 0.00255 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.02464 on 29 degrees of freedom

Multiple R-squared: 0.9781, Adjusted R-squared: 0.9736

F-statistic: 216.3 on 6 and 29 DF, p-value: < 2.2e-16

> ## segmented

> fm3 <- lm(log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

+ log(usedcar) + trend), data = as.data.frame(USGasG))

> summary(fm3)

Call:

lm(formula = log(gas/population) ~ shock/(log(income) + log(price) +

log(newcar) + log(usedcar) + trend), data = as.data.frame(USGasG))

Residuals:

Min 1Q Median 3Q Max

-0.027349 -0.006332 0.001295 0.007159 0.022016

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -4.13439 5.03963 -0.820 0.420075

shockafter -4.74111 5.51576 -0.860 0.398538

shockbefore:log(income) 0.42400 0.57973 0.731 0.471633

shockafter:log(income) 1.01408 0.24904 4.072 0.000439 ***

shockbefore:log(price) 0.09455 0.24804 0.381 0.706427

shockafter:log(price) -0.24237 0.03490 -6.946 3.5e-07 ***

shockbefore:log(newcar) 0.58390 0.21670 2.695 0.012665 *

shockafter:log(newcar) 0.33017 0.15789 2.091 0.047277 *

shockbefore:log(usedcar) -0.33462 0.15215 -2.199 0.037738 *

shockafter:log(usedcar) -0.05537 0.04426 -1.251 0.222972

shockbefore:trend 0.02637 0.01762 1.497 0.147533

shockafter:trend -0.01262 0.00329 -3.835 0.000798 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.01488 on 24 degrees of freedom

Multiple R-squared: 0.9934, Adjusted R-squared: 0.9904

F-statistic: 328.5 on 11 and 24 DF, p-value: < 2.2e-16

>

> ## Chow test

> anova(fm3, fm1)

Analysis of Variance Table

Model 1: log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

log(usedcar) + trend)

Model 2: log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend

Res.Df RSS Df Sum of Sq F Pr(>F)

1 24 0.0053144

2 30 0.0251878 -6 -0.019873 14.958 4.595e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

> library("strucchange")

> sctest(log(gas/population) ~ log(income) + log(price) + log(newcar) +

+ log(usedcar) + trend, data = USGasG, point = c(1973, 1), type = "Chow")

Chow test

data: log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + trend

F = 14.958, p-value = 4.595e-07

> ## Recursive CUSUM test

> rcus <- efp(log(gas/population) ~ log(income) + log(price) + log(newcar) +

+ log(usedcar) + trend, data = USGasG, type = "Rec-CUSUM")

> plot(rcus)

> sctest(rcus)

Recursive CUSUM test

data: rcus

S = 1.4977, p-value = 0.0002437

> ## Note: Greene's remark that the break is in 1984 (where the process crosses its

> ## boundary) is wrong. The break appears to be no later than 1976.

>

> ## More examples can be found in:

> ## help("Greene2003")

>

>

>

>

>

> dev.off()

null device

1

>

|